Running a cannabis dispensary in the United States

is one of the most financially complex business ventures in modern commerce. You face federal restrictions under Section 280E of the Internal Revenue Code, strict state-level compliance requirements, and daily cash-heavy transactions — all at once. Without a proper cannabis dispensary chart of accounts setup, your books become a liability instead of an asset.

In this guide, you will learn exactly

how to structure your dispensary’s chart of accounts, which account categories matter most, and how to stay compliant despite the unique tax burdens cannabis businesses carry. You will also discover the most common mistakes dispensary owners make — and how to avoid them.

Whether you are launching a new dispensary or cleaning up messy books, this step-by-step resource will give you a rock-solid financial foundation. Let’s get started.

What Is a Cannabis Dispensary Chart of Accounts?

A chart of accounts (COA) is the master list of every financial account your business uses to record transactions. For cannabis dispensaries, the COA serves as the backbone of your entire accounting system — and it must be built specifically to handle the unique legal and tax environment cannabis businesses operate in across the USA.

Every dollar that flows through your dispensary

— from product sales to payroll to rent — gets assigned to a specific account in your COA. When set up correctly, these accounts feed your income statement, balance sheet, and cash flow statement. When set up incorrectly, they can trigger IRS scrutiny, cost you thousands in denied deductions, and make tax season a nightmare.

Standard business accounting software like QuickBooks

was not designed with cannabis compliance in mind. That is why a customized cannabis dispensary chart of accounts setup is essential — not optional — for every dispensary in the United States.

Why Cannabis Businesses Need a Specialized COA

Section 280E of the US tax code prohibits cannabis businesses from deducting most ordinary business expenses because marijuana remains a Schedule I controlled substance at the federal level. However, dispensaries can still deduct the Cost of Goods Sold (COGS). A properly structured COA helps you maximize COGS deductions legally while keeping all other expenses correctly categorized.

Without this structure, you risk losing deductions

you are legally entitled to. You also risk claiming deductions you are not entitled to — which can lead to IRS audits, penalties, and back taxes. The stakes for US cannabis businesses are simply too high to use a generic accounting setup.

Who Needs a Cannabis-Specific Chart of Accounts?

Any cannabis dispensary, marijuana retail store, or multi-state operator (MSO) in the United States needs a dispensary-specific COA. This includes recreational dispensaries, medical marijuana facilities, delivery-only operations, and cannabis consumption lounges. If you sell cannabis products and file US tax returns, this guide applies to you.

Key Rules and IRS Requirements for Cannabis Accounting

The most critical rule governing cannabis dispensary accounting in the USA is Internal Revenue Code Section 280E. This code section states that no deduction or credit is allowed for any amount paid in carrying on a trade or business that consists of trafficking in controlled substances. For dispensaries, this means most business expenses — rent, utilities, marketing, salaries for non-COGS staff — are not federally deductible.

However, the IRS does allow cannabis businesses

to deduct the Cost of Goods Sold (COGS) under IRC Section 471. This is the primary tax planning opportunity for every US dispensary. Your chart of accounts must be designed to clearly separate COGS from non-deductible operating expenses.

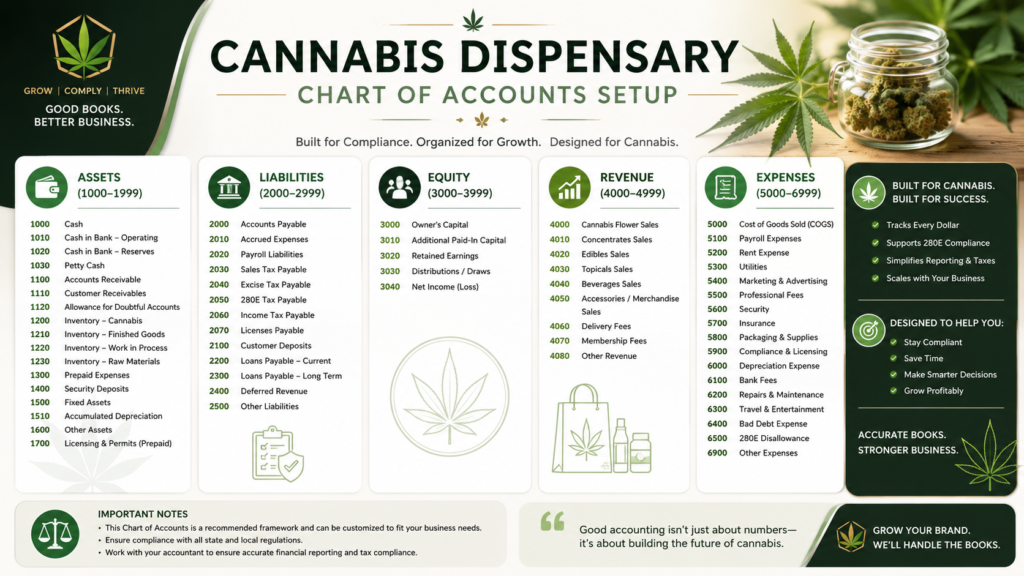

The Five Core Account Categories Every Dispensary Needs

A well-structured cannabis dispensary COA is built around five main account categories. Each plays a distinct role in your financial reporting and tax compliance:

Assets — Everything your dispensary owns: cash, inventory, equipment, and accounts receivable.

Liabilities — Everything your dispensary owes: loans, sales tax payable, credit lines.

Equity — Owner’s equity, retained earnings, and capital contributions.

Revenue — All income from cannabis sales, accessories, delivery fees, and other sources.

Expenses — Operating costs, split carefully between COGS (deductible) and non-COGS (280E-restricted).

IRS References and Compliance Anchors

According to IRS guidance, cannabis businesses must use generally accepted accounting principles (GAAP) and maintain contemporaneous records of all transactions. The IRS has published field audit guidelines specifically for cannabis businesses. Dispensaries in states like California, Colorado, Illinois, and Michigan face both federal 280E exposure and state-level tax obligations. Your COA must be compatible with both layers of reporting.

The IRS requires that inventory be valued using the cost

method or another IRS-approved method under Section 471. Proper inventory accounting is therefore not just a best practice — it is a legal requirement for every US cannabis dispensary.

Common Cannabis Dispensary Chart of Accounts Mistakes to Avoid

Even well-intentioned dispensary owners make critical accounting errors that cost them dearly at tax time. Therefore, understanding these pitfalls before you set up your books can save your business thousands of dollars — or even protect it from IRS enforcement action.

Mistake 1: Mixing COGS and Non-COGS Expenses

This is the most expensive mistake a cannabis business can make. When operating costs like rent, marketing, and utilities get recorded under COGS, the dispensary incorrectly inflates its deductible expenses. If audited, the IRS will disallow these deductions and assess back taxes plus penalties. Your COA must use separate account numbers for every COGS item and every non-COGS item — with no overlap.

Mistake 2: Using a Generic Accounting Template

Off-the-shelf QuickBooks templates or restaurant-industry COAs do not account for 280E limitations, cannabis inventory regulations, or state-specific excise tax accounts. Additionally, these generic setups often lack the granularity needed to separate ancillary business income (which may not be subject to 280E) from cannabis-specific revenue. Starting with the wrong template creates cascading problems throughout your entire financial system.

Mistake 3: Failing to Track Cash Transactions Properly

Cannabis dispensaries in the USA are largely cash businesses due to federal banking restrictions. However, every cash transaction must be recorded accurately and matched to your daily POS reports. A COA that lacks dedicated cash accounts — or that combines petty cash with operational cash — creates reconciliation gaps that can look fraudulent to auditors. Separate cash drawer accounts are essential.

Mistake 4: Ignoring State Excise Tax Accounts

States like California impose a cannabis excise tax (currently 15%) that must be collected from customers and remitted to the state. Similarly, other states impose cultivation taxes, weight-based taxes, or potency-based taxes. These must each have their own liability accounts in your COA. Combining them with general sales tax creates reconciliation errors and potentially exposes you to state tax penalties.

Mistake 5: Not Separating Ancillary Revenue

Many dispensaries sell non-cannabis items — pipes, grinders, branded clothing, or CBD products. Because Section 280E applies only to cannabis trafficking, income from truly ancillary sales may be deductible. However, this only works if your COA cleanly separates ancillary revenue and its associated expenses from cannabis revenue and expenses. Without this separation, you cannot substantiate the deduction if questioned by the IRS.

How to Set Up a Cannabis Dispensary Chart of Accounts: Step-by-Step

Setting up your cannabis dispensary chart of accounts setup correctly from day one is far easier than fixing a broken system later. Follow these seven steps to build a compliant, audit-ready COA for your US dispensary.

Step 1: Choose the Right Accounting Software

QuickBooks Online or QuickBooks Desktop are the most widely used platforms for cannabis accounting in the USA. Select the version that supports class tracking — this feature allows you to separate cannabis and ancillary business segments within the same company file. Some dispensaries use specialized platforms like Dutchie, Flowhub, or Treez for point-of-sale, which must then sync with your accounting software.

Step 2: Set Up Your Asset Accounts

Create individual asset accounts for: primary operating bank account, cash drawers by register, accounts receivable (if applicable), cannabis inventory at cost, non-cannabis merchandise inventory, prepaid expenses, security deposits, and fixed assets like furniture, fixtures, and equipment. Each account should carry a unique account number — typically in the 1000–1999 range for assets.

Step 3: Build Your Liability Accounts

Liability accounts (typically numbered 2000–2999) should include: accounts payable, cannabis excise tax payable, state sales tax payable, city/local tax payable, payroll taxes payable, short-term loans, and long-term debt. Each state excise tax type should have its own account. For example, a California dispensary needs separate accounts for the 15% excise tax and any applicable cultivation tax passed through from licensed distributors.

Step 4: Create Your Revenue Accounts

Revenue accounts (4000–4999) must separate cannabis product sales by category — flower, concentrates, edibles, topicals, vapes, and pre-rolls — from ancillary revenue like accessories, delivery fees, and branded merchandise. This separation is critical for both financial reporting and 280E analysis. Also create a separate account for discounts and returns to net against gross sales accurately.

Step 5: Structure Your COGS Accounts

Cost of Goods Sold (5000–5999) is your most important account group. Under IRC Section 471, allowable COGS for a cannabis retailer typically includes the cost to purchase cannabis products from licensed distributors or cultivators, plus the direct cost of packaging materials used in the sale. Additionally, if your state allows producer-retailer vertical integration, costs associated with growing and processing can also be included in COGS. These accounts must be meticulously documented.

Step 6: Set Up Operating Expense Accounts

Operating expenses (6000–6999) are the costs that Section 280E restricts from federal deduction. Despite being non-deductible at the federal level, these must still be tracked accurately for state tax purposes and financial management. Create accounts for: rent and occupancy, utilities, marketing and advertising, insurance, legal and professional fees, office supplies, banking fees, and non-COGS payroll (managers, budtenders, security). Granularity here protects you during audits.

Step 7: Apply Account Numbers and Enable Class Tracking

Assign a consistent numbering scheme and activate class tracking in your accounting software to segment cannabis versus ancillary operations. Run a test transaction through every major account to confirm proper flow. Then schedule a monthly reconciliation review — ideally with a cannabis-specialized CPA — to catch discrepancies before they compound. For more on compliant bookkeeping practices, visit the IRS Small Business Tax Center at IRS.gov.

How Tranzesta Can Help With Your Cannabis Dispensary Chart of Accounts Setup

Tranzesta is a US-based tax consultation firm with deep expertise in cannabis industry accounting. We understand that running a dispensary means navigating Section 280E, managing complex inventory regulations, staying current with state excise tax changes, and keeping your books audit-ready at all times — all while actually running your business.

Our cannabis accounting services include building

a fully customized cannabis dispensary chart of accounts setup from scratch, migrating your existing books to a compliant structure, ongoing monthly bookkeeping, and strategic tax planning to maximize your allowable COGS deductions under Section 471. We serve dispensary owners across the United States, from single-location operations to multi-state operators.

Tranzesta also provides quarterly financial reviews,

state compliance reconciliations, and year-end tax preparation specifically designed for cannabis businesses. We know the IRS audit red flags — and we make sure your records are clean, documented, and defensible.

Ready to get your dispensary books compliant? Contact our team at hello@tranzesta.com for a free consultation. You can also explore our full cannabis accounting services at Tranzesta.com to learn more about how we support cannabis business owners across the USA.

Cannabis Dispensary Chart of Accounts Setup: Expert Tips for 2026

Beyond the fundamentals, there are advanced strategies that separate compliant, financially optimized dispensaries from those that struggle every tax season. Here are the most important pro tips for 2026:

Use sub-accounts liberally:

Break down each major account into sub-accounts for granular tracking. For example, under cannabis inventory, create sub-accounts for flower, edibles, concentrates, and vapes separately.

Align your COA with your POS system:

Your point-of-sale system should map directly to your revenue accounts. Misalignment between POS categories and COA revenue accounts is a common source of reconciliation headaches.

Document every COGS allocation decision:

If you allocate any shared costs — such as a portion of manager time or shared facility costs — to COGS, you must document the allocation methodology. The IRS requires that COGS allocations be reasonable and consistently applied.

Review your COA annually:

State cannabis tax laws change frequently. For example, several US states have adjusted cannabis excise tax rates or reporting requirements in recent years. Review your COA structure at the start of each year to ensure it still captures all required data.

Never commingle personal and business funds:

This is especially critical for cannabis businesses, where the IRS scrutinizes financials more closely. A separate business bank account for every entity is non-negotiable.

Consider cannabis-specific software add-ons:

Tools like Leaf Logix, BioTrack, or METRC-integrated systems can automate inventory tracking and sync directly with accounting platforms, reducing manual entry errors.

Most importantly, work with a CPA or accounting firm that specializes in cannabis — not a generalist who occasionally takes dispensary clients. The regulatory complexity is simply too high for a one-size-fits-all approach. Tranzesta’s team stays current on all federal and state cannabis tax developments so you never have to worry about being caught off guard.

Conclusion

Setting up a proper cannabis dispensary chart of accounts is not just an accounting task — it is a compliance and tax strategy imperative. Three takeaways stand above all others. First, your COA must clearly separate COGS from non-COGS expenses to navigate Section 280E correctly and legally maximize your deductions. Second, cannabis-specific account categories — including state excise tax liabilities, ancillary revenue, and inventory sub-accounts — are non-negotiable for accurate reporting. Third, your financial system must be built for audit-readiness from day one, not retrofitted under pressure.

For cannabis business owners across the United States,

getting this right early saves money, reduces stress, and builds a business that is positioned to grow. Furthermore, as state and federal cannabis policy continues to evolve in 2026, a well-structured COA gives you the flexibility to adapt quickly.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

A chart of accounts for a cannabis dispensary is a structured list of every financial account the business uses to record transactions. It is customized for cannabis to separate Cost of Goods Sold (deductible under IRC Section 471) from non-deductible operating expenses restricted by IRS Section 280E. A properly built cannabis COA covers assets, liabilities, equity, revenue, COGS, and operating expenses — each with unique account numbers and sub-accounts tailored to dispensary operations in the United States.

Section 280E of the Internal Revenue Code prohibits cannabis businesses from deducting most ordinary business expenses at the federal level because marijuana is still classified as a Schedule I controlled substance. However, dispensaries can deduct Cost of Goods Sold under IRC Section 471. This means your chart of accounts must carefully separate COGS from all other expenses. Properly structured dispensary books allow you to maximize allowable deductions and reduce the overall effective tax rate on your cannabis business income.

QuickBooks Online and QuickBooks Desktop are the most widely used accounting platforms for cannabis dispensaries in the USA because they support class tracking, custom chart of accounts, and integration with cannabis point-of-sale systems. Some dispensaries also use cannabis-specific ERP platforms. However, the software itself is less important than how it is configured. A cannabis-specialized accountant should set up and maintain your chart of accounts to ensure it reflects your specific state compliance requirements and 280E limitations.

Cannabis dispensaries in the United States cannot deduct most ordinary business expenses at the federal level due to IRS Section 280E. This includes rent, marketing, most payroll, and utilities. However, dispensaries can deduct Cost of Goods Sold under IRC Section 471, which covers the purchase cost of cannabis inventory and direct packaging costs. Some states allow additional deductions that the federal government does not. Proper COA setup ensures you capture every allowable deduction while staying fully compliant.

A cannabis dispensary should reconcile its accounts monthly at a minimum — and ideally perform a weekly cash reconciliation given the cash-intensive nature of the business. Monthly reconciliation involves matching your bank statements, POS reports, and accounting records to catch discrepancies early. Quarterly reviews with a cannabis CPA help ensure your chart of accounts continues to reflect current state tax requirements and that your COGS allocations remain properly documented for IRS compliance.

One Response