Cannabis dispensaries in the United States carry

some of the heaviest tax burdens of any industry in the country. Yet many owners lose thousands of dollars every year simply because they chose the wrong inventory accounting method. Understanding cannabis inventory accounting FIFO LIFO differences is not optional — it is one of the most consequential financial decisions you will make as a dispensary owner.

In this guide, you will learn exactly how FIFO

(First In, First Out) and LIFO (Last In, First Out) work, which methods the IRS actually allows for cannabis businesses, how each method affects your Cost of Goods Sold (COGS) and taxable income, and which approach gives your dispensary the best tax outcome under Section 280E.

Additionally, you will get a step-by-step framework

for selecting and implementing the right method — plus expert tips from the cannabis accounting team at Tranzesta.com Let’s break it down.

What Is Cannabis Inventory Accounting, and Why Do FIFO and LIFO Matter?

Cannabis inventory accounting refers to the system a dispensary uses to track the cost of cannabis products as they move from purchase to sale. The method you choose directly determines how much of your inventory cost gets recorded as Cost of Goods Sold — which is the only major tax deduction available to cannabis businesses under IRS Section 280E.

FIFO and LIFO are the two most widely discussed

inventory costing methods in the United States. However, they produce dramatically different financial results — especially in a market where cannabis product costs fluctuate frequently. For dispensaries facing both federal 280E restrictions and state tax obligations, the stakes could not be higher.

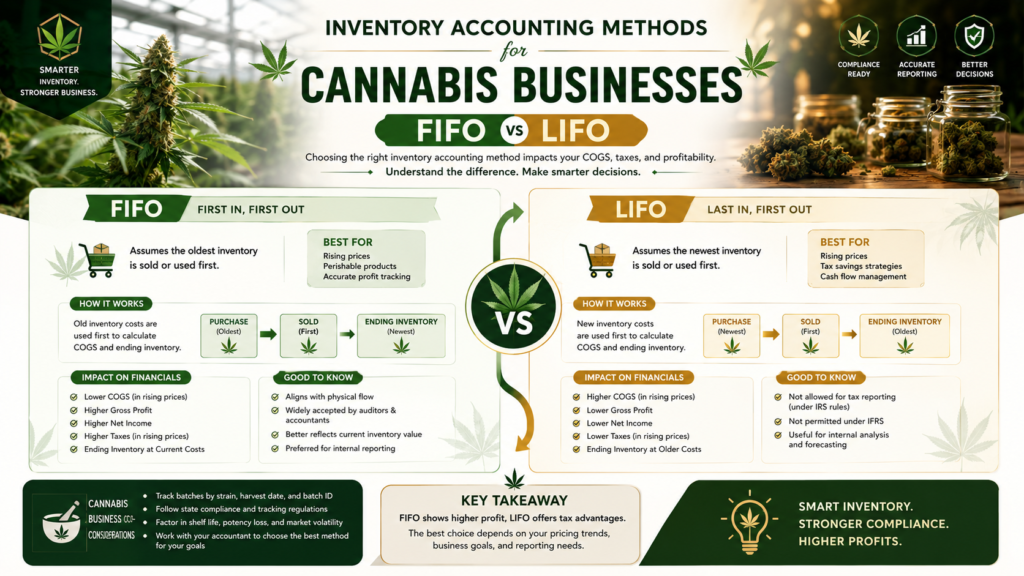

What Is FIFO (First In, First Out)?

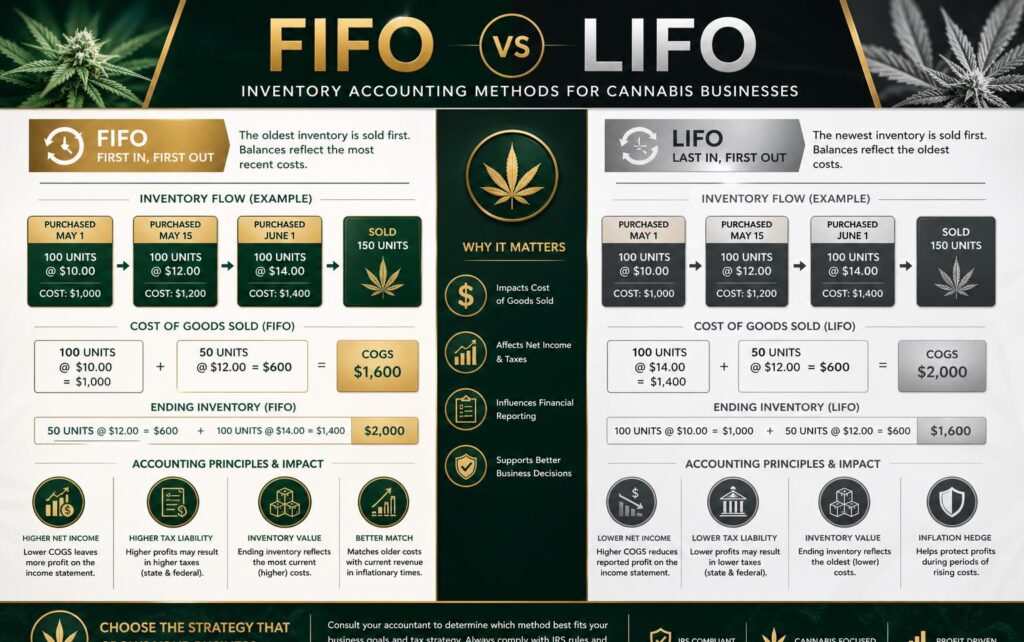

FIFO — First In, First Out — assumes that the oldest inventory you purchased gets sold first. Therefore, the cost assigned to each sale reflects the earliest purchase price in your inventory. In a market where wholesale cannabis prices are declining, FIFO results in higher COGS because older, higher-priced stock gets expensed first. In a rising-cost environment, FIFO produces lower COGS and higher taxable income.

FIFO is the most commonly used and IRS-accepted

inventory method for cannabis businesses in the USA. It also aligns naturally with how dispensaries physically handle perishable cannabis products — older stock should genuinely sell first to maintain quality and compliance with state shelf-life requirements.

What Is LIFO (Last In, First Out)?

LIFO — Last In, First Out — assumes that the most recently purchased inventory sells first. In theory, LIFO can reduce taxable income in a rising-cost environment because newer, more expensive inventory gets expensed as COGS first. However, LIFO is specifically prohibited for cannabis businesses under IRS regulations. The IRS requires that cannabis inventory be valued using methods permitted under IRC Section 471 — and LIFO does not qualify for cannabis retailers operating under a state-regulated market. This distinction is critical for every US dispensary owner to understand.

IRS Rules and Requirements for Cannabis Inventory Accounting

The IRS governs cannabis inventory accounting under Internal Revenue Code Section 471, which requires businesses to use the cost method or another IRS-approved method for valuing inventory. Additionally, IRS Section 280E prohibits cannabis businesses from deducting most ordinary expenses — but COGS under Section 471 remains deductible. This makes your inventory accounting method your most powerful tax tool.

For cannabis dispensaries specifically,

the IRS has clarified through audit guidelines and Tax Court rulings that the following rules apply to inventory valuation in the United States:

FIFO is fully permitted and is the IRS-preferred method for cannabis retail businesses.

Weighted Average Cost (WAC) is also permitted and widely used for dispensaries with high SKU variety.

Specific Identification is permitted when individual items can be uniquely tracked — relevant for high-value cannabis concentrate or extract products.

LIFO is not permitted for cannabis businesses that are classified as retailers under state law.

All inventory records must be contemporaneous — meaning you must track costs at the time of purchase, not reconstructed later.

Physical inventory counts must occur at least annually, and the results must reconcile to your accounting records.

How the Cost Method Works Under IRC Section 471

The cost method requires you to record inventory at its actual acquisition cost — including the purchase price paid to licensed distributors or cultivators, plus any direct costs to bring the product to its retail location (such as freight and testing fees required by state law). Under this method, whichever costing assumption you use — FIFO or WAC — you apply it consistently to every product category.

The IRS expects cannabis businesses to apply their chosen method consistently from year to year. Switching methods requires IRS approval via Form 3115 (Application for Change in Accounting Method). Therefore, choosing the right method from the start matters enormously.

What About the Weighted Average Cost Method?

The Weighted Average Cost (WAC) method calculates COGS using the average cost of all units available for sale during the period. For example, if a California dispensary purchased 100 units at $8 each and 100 units at $10 each, the weighted average cost would be $9 per unit. WAC smooths out price fluctuations over time and is particularly useful for dispensaries that carry large quantities of similar products at varying purchase prices. Many US dispensaries favor WAC for its simplicity and consistency.

Common Cannabis Inventory Accounting Mistakes That Cost Dispensaries Money

Even experienced dispensary operators make critical inventory accounting errors that inflate their tax bills or expose them to IRS audit risk. Therefore, understanding these mistakes before they happen can save your dispensary a significant amount of money.

Mistake 1: Attempting to Use LIFO for Cannabis Inventory

Some dispensary owners or general-purpose accountants mistakenly try to apply LIFO because it appears to reduce taxable income in certain market conditions. However, the IRS explicitly disallows LIFO for cannabis businesses operating as retailers. If an IRS examination discovers LIFO usage, the agent will restate your inventory values using an approved method — typically resulting in a higher tax liability, plus penalties and interest. This is an avoidable and costly error.

Mistake 2: Inconsistently Applying the Chosen Method

Switching between FIFO and WAC from quarter to quarter — or applying different methods to different product categories without documentation — violates IRS consistency requirements. The IRS requires that once you adopt an accounting method, you must use it consistently. Any change requires filing Form 3115. Inconsistent application not only creates audit exposure but also produces unreliable financial statements that make business planning nearly impossible.

Mistake 3: Excluding Allowable Costs from COGS

Many cannabis businesses undercount their COGS by failing to include all allowable acquisition costs. In addition to the purchase price of cannabis products, COGS can include state-mandated testing fees paid before the product enters retail inventory, freight and shipping costs from licensed distributors, and direct packaging materials used in the sale. Excluding these costs means you are overpaying your federal tax liability unnecessarily.

Mistake 4: Failing to Conduct Regular Physical Inventory Counts

The IRS requires that physical inventory counts reconcile to book inventory records. Dispensaries that rely solely on point-of-sale system reports without periodic physical counts risk significant discrepancies — especially given cannabis product shrinkage, breakage, and the high volume of cash transactions. Monthly mini-counts and a comprehensive annual physical count are minimum best practices for US dispensaries.

Mistake 5: Not Documenting Inventory Valuation Decisions

Your choice of inventory method, your cost allocation decisions, and any adjustments you make to inventory values must be documented in writing. If audited, the IRS will request your inventory accounting policies and procedures. Dispensaries that cannot produce clear documentation of how they valued inventory risk having their COGS disallowed — which dramatically increases their effective tax rate under 280E.

How to Choose and Implement the Right Cannabis Inventory Accounting Method

Selecting the right inventory accounting method for your dispensary is a decision that affects your taxes, your financial statements, and your audit risk every single year. Follow these seven steps to make the right choice and implement it correctly.

Step 1: Understand Your Product Mix and Price Volatility

First, analyze how your wholesale cannabis costs move over time. If your cannabis purchase prices are relatively stable, WAC is simple and effective. If you carry a wide variety of products at very different price points — premium flower versus value edibles, for example — FIFO may give you cleaner tracking by product category. Understanding your price volatility guides your method selection.

Step 2: Confirm Your State-Level Inventory Tracking Requirements

Next, check your state cannabis control board’s requirements. States like Colorado, California, Illinois, and Michigan require dispensaries to track inventory through state-mandated seed-to-sale systems such as METRC. Your accounting method must be compatible with your state tracking system. In most cases, FIFO aligns most naturally with state-regulated inventory tracking because products are logged in order of receipt.

Step 3: Choose Between FIFO and Weighted Average Cost

For most US cannabis dispensaries, the choice comes down to FIFO versus WAC. Choose FIFO if you want simplicity, natural alignment with physical product flow, and clear traceability per batch. Choose WAC if you purchase large volumes of similar products at varying prices and prefer smoothed cost averaging. Either method is IRS-approved under IRC Section 471. Document your decision in writing before your first tax period.

Step 4: Configure Your Accounting Software

Configure your accounting platform — typically QuickBooks — to apply your chosen method consistently across all cannabis product categories. Set up inventory items with accurate opening costs. If you use a cannabis-specific POS system like Dutchie, Flowhub, or Treez, ensure that cost data flows correctly into your accounting software. Mismatches between POS cost records and accounting records are a leading cause of inventory reconciliation failures.

Step 5: Establish a Consistent Receiving and Costing Process

Every time you receive cannabis products from a licensed distributor or cultivator, record the exact unit cost — including any allowable additional costs like state-required testing fees or freight. Create a receiving checklist that your inventory manager completes for every delivery. This contemporaneous documentation is what protects your COGS deductions during an IRS audit.

Step 6: Perform Monthly Reconciliations and an Annual Physical Count

Monthly, reconcile your accounting software inventory values to your POS system’s reported on-hand quantities and costs. Investigate and resolve every discrepancy. Annually, perform a full physical count and adjust your book inventory to match physical reality. Document the count process, the counters’ names, and the date. Store these records for at least seven years — the IRS statute of limitations for civil tax fraud is six years.

Step 7: Review Your Method Annually with a Cannabis CPA

Finally, review your inventory accounting method every year with a CPA who specializes in cannabis. Market conditions change, state laws evolve, and new IRS guidance may affect your approach. If a method change makes sense, file Form 3115 with the IRS before implementing it. Learn more about comprehensive cannabis tax planning at Tranzesta.com, where our team stays current on every federal and state development affecting US dispensaries.

How Tranzesta Helps Cannabis Businesses Master Inventory Accounting

Tranzesta is a US-based tax consultation firm that specializes exclusively in complex tax situations — including cannabis industry accounting. Our team works directly with dispensary owners, multi-state operators, and cannabis cultivators across the United States to set up, maintain, and optimize their inventory accounting systems.

When it comes to cannabis inventory accounting FIFO LIFO decisions, Tranzesta provides a full suite of services: initial method selection analysis, QuickBooks configuration for cannabis inventory, monthly bookkeeping and reconciliation, COGS optimization reviews, and year-end tax preparation under Section 280E. We also represent clients during IRS examinations, ensuring your inventory documentation is thorough and defensible.

Additionally, Tranzesta handles state excise tax reconciliations, ancillary revenue separation for 280E analysis, and ongoing advisory services as your dispensary grows. Our clients across states like California, Colorado, Illinois, Arizona, and Michigan trust us to keep their books clean and their tax positions optimized.

Contact our team at hello@tranzesta.com for a free consultation. Visit Tranzesta.com to learn more about our cannabis accounting and bookkeeping services and see how we help dispensary owners across the USA reduce their effective tax rate while staying fully compliant.

Cannabis Inventory Accounting FIFO LIFO: Expert Tips for 2026

Beyond choosing between FIFO and WAC, there are advanced strategies that the most tax-efficient dispensaries in the United States use to maximize their COGS deductions and minimize audit risk. Here are the top tips from Tranzesta’s cannabis accounting team:

Track costs by product category, not just by total inventory:

Separating flower, edibles, concentrates, vapes, and pre-rolls into distinct inventory sub-accounts gives you granular COGS data and makes audits far easier to navigate.

Include all IRS-allowable COGS components:

Beyond the product purchase price, include state-required lab testing fees, inbound freight from licensed distributors, and direct packaging materials. Each dollar added to COGS legally is a dollar removed from your 280E-restricted taxable income.

Use class tracking in QuickBooks to separate cannabis and ancillary inventory:

This separation allows you to potentially deduct expenses associated with ancillary sales — such as accessories and branded merchandise — that fall outside 280E’s reach.

Document your inventory method in a written accounting policy:

A one-to-two-page accounting policy document that describes your inventory costing method, your receiving process, and your reconciliation schedule is one of the most powerful audit shields a dispensary can have.

Stay current on IRS cannabis audit guidelines:

The IRS has published specific examination techniques for cannabis businesses. Tranzesta monitors these guidelines continuously to ensure our clients’ books meet the exact standard the IRS expects.

Consider Specific Identification for high-value SKUs:

If your dispensary carries premium concentrates, solventless extracts, or rare cultivars priced above $50 per unit, Specific Identification accounting may allow more precise COGS tracking — and potentially higher deductions — than FIFO or WAC.

Most importantly, never try to navigate cannabis inventory accounting alone. The combination of federal 280E restrictions, IRS Section 471 requirements, and state-level compliance obligations creates a complexity level that demands specialized expertise.

Conclusion

Cannabis inventory accounting decisions have a direct and significant impact on how much your dispensary pays in taxes every year. Three takeaways define everything covered in this guide. First, FIFO and Weighted Average Cost are the only IRS-approved inventory methods for cannabis retailers in the United States — LIFO is explicitly prohibited and using it creates serious audit risk. Second, your inventory method determines your COGS, and COGS is your most powerful tax deduction under Section 280E — making method selection a critical financial strategy decision. Third, consistency, documentation, and regular reconciliation are what protect your deductions when the IRS comes knocking.

For cannabis business owners across the USA,

getting your inventory accounting right is not just about compliance — it is about protecting every dollar your dispensary earns. Furthermore, with cannabis tax law continuing to evolve in 2026, staying current with expert guidance is more important than ever.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

Cannabis dispensaries in the United States should use either FIFO (First In, First Out) or the Weighted Average Cost method for inventory accounting.

Cannabis businesses operating as retailers in the United States cannot use LIFO (Last In, First Out) for inventory accounting. The IRS does not permit cannabis dispensaries to use LIFO under IRC Section 471 regulations. Attempting to use LIFO exposes a dispensary to IRS audit adjustments, back taxes, penalties, and interest. .

Inventory accounting directly affects cannabis taxes under Section 280E because the Cost of Goods Sold is Higher COGS means lower taxable income under 280E. Therefore, accurate, IRS-compliant inventory accounting is the single most important tax strategy for US cannabis dispensaries.

Cannabis dispensaries in the United States can include several cost components in their Cost of Goods Sold under IRC Section 471. These include the purchase price paid to licensed distributors or cultivators, state-required lab testing fees incurred before products enter retail inventory, inbound freight and shipping costs from the supplier to the dispensary, and the cost of direct packaging materials used in the sale of cannabis products.

A cannabis dispensary should perform a full physical inventory count at least once per year, with the results reconciled to accounting records. Additionally, most compliance-focused dispensaries in the United States perform monthly mini-counts on high-velocity or high-value product categories to catch discrepancies early. State seed-to-sale tracking systems such as METRC require ongoing inventory reporting, which makes regular reconciliation between the state system, the POS system, and the accounting system essential for both compliance and accurate COGS calculation.

3 Responses