Did you know that the IRS taxes US citizens

on their worldwide income — no matter where in the world they earned it? That single rule creates enormous confusion for expats, online content creators, cannabis operators, and self-employed Americans doing business internationally. Understanding the difference in US source income vs non-US source tax treatment is not optional — it is the foundation of every compliant US tax return filed by someone with cross-border income.

In this guide, you will learn exactly how the IRS defines

US source income and foreign source income, which rules apply to your specific situation, the most expensive mistakes taxpayers make, and a step-by-step process to handle your filing correctly. Whether you are an OnlyFans creator receiving payments from overseas subscribers, a cannabis business owner with out-of-state revenue, a US expat working abroad, or a foreign national earning money inside the United States, this guide covers every angle.

What Is US Source Income vs Non-US Source Tax Treatment?

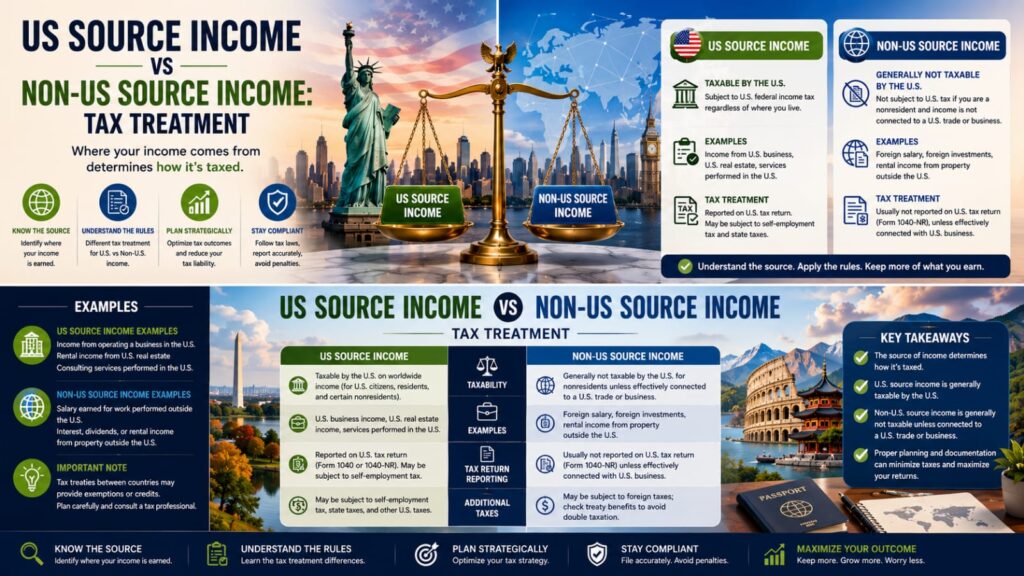

US source income is any income that the IRS considers to originate inside the United States. Non-US source income — also called foreign source income — is income that originates outside American borders. The distinction determines who owes US tax, how much they owe, and which credits or treaties may reduce that liability.

This distinction matters enormously because the United States is one of only two countries in the world (alongside Eritrea) that taxes its citizens on their worldwide income. Under Internal Revenue Code (IRC) Sections 861 through 865, the IRS has created a detailed framework to classify income as domestic or foreign. Every taxpayer with international ties needs to understand these rules.

How the IRS Defines US Source Income

The IRS determines income sourcing based on the type of income — not simply where you, the taxpayer, happen to live. Under IRC Section 861, the following types of income are generally treated as US source income:

Wages and salaries earned for services performed inside the United States

Business income from a US trade or business

Rental income from US real property

Dividends from US corporations

Interest paid by US residents, corporations, or the US government

Royalties for the use of intellectual property inside the United States

Therefore, even a foreign national living abroad may owe US taxes if they earn income from a US source. Conversely, a US citizen living overseas may still owe US taxes on foreign income — but may qualify for exclusions or credits to reduce or eliminate double taxation.

How the IRS Defines Non-US Source Income

Non-US source income — governed by IRC Section 862 — includes income derived from sources outside the United States. Examples include foreign wages, foreign business profits, foreign rental income, and foreign dividends. For US citizens and green card holders, this income is still taxable by the IRS. However, mechanisms like the Foreign Tax Credit (Form 1116) and the Foreign Earned Income Exclusion (Form 2555) can significantly reduce or eliminate double taxation.

For non-resident aliens, only US source income is generally subject to US tax. This is a critical distinction that affects thousands of international taxpayers every year.

Key IRS Rules Governing US Source Income Tax Treatment

The IRS applies specific sourcing rules depending on the type of income involved. Knowing these rules in detail helps you avoid overpaying — or underpaying — your US tax obligations.

The Source Rules for Different Income Types

Below is a breakdown of how the IRS sources each major income category under IRC Sections 861-865:

Personal services income: Sourced where the services are physically performed. For example, a US citizen working in Germany sources that income as foreign, even if the employer is a US company.

Interest income: Generally sourced based on the residence of the payer. Interest paid by a US person or entity is US source income.

Dividend income: Sourced based on the country of incorporation of the paying corporation. Dividends from a US corporation are US source income.

Rental and royalty income: Sourced based on where the property is located or where the intangible property is used.

Sales of inventory: Sourced based on the location where title to the property passes from seller to buyer.

Sales of depreciable property: More complex — a portion may be US source and a portion may be foreign source, depending on depreciation previously claimed.

What About Withholding Taxes on US Source Income?

When a non-resident alien earns US source income, the US generally imposes a flat 30% withholding tax under IRC Section 1441. This rate may be reduced by a tax treaty between the US and the non-resident’s home country. The US has tax treaties with over 65 countries, and treaty benefits can reduce withholding rates to as low as 0% on certain income types.

US citizens and resident aliens earning foreign

source income are taxed at their ordinary tax rates. However, they can use Form 1116 (Foreign Tax Credit) to claim a credit for foreign taxes already paid on that income. Tranzesta.com Alternatively, qualifying US citizens and resident aliens living abroad may exclude up to $126,500 of foreign earned income for tax year 2024 using Form 2555.

Additionally, the Net Investment Income Tax

(NIIT) of 3.8% under IRC Section 1411 may apply to certain US source and foreign source investment income for higher-income taxpayers with modified adjusted gross income above $200,000 (single) or $250,000 (married filing jointly).

For official IRS guidance on income sourcing rules,

review IRS Publication 519 (US Tax Guide for Aliens), which covers these rules in detail.

Common Mistakes in Handling US Source Income vs Non-US Source Tax Treatment

Many US taxpayers — including online creators, expats, and business owners — make costly errors when classifying income and filing correctly. Here are the five most damaging mistakes and how to avoid them.

Mistake 1: Assuming Foreign Income Is Not Taxable in the US

This is the most common and most expensive mistake US citizens make. Many Americans living abroad believe that because they pay taxes in another country, they owe nothing to the IRS. That is incorrect. The US taxes its citizens and permanent residents on worldwide income, regardless of where it is earned or whether it has already been taxed abroad. Failing to report foreign income can result in substantial penalties — including civil fines of up to $10,000 per violation and, in willful cases, criminal prosecution.

Mistake 2: Ignoring FBAR and FATCA Reporting Requirements

Two separate reporting regimes apply to US taxpayers with foreign financial accounts. The Foreign Bank Account Report (FBAR) — FinCEN Form 114 — must be filed if your foreign accounts exceed $10,000 at any point during the year. The Foreign Account Tax Compliance Act (FATCA) requires additional reporting on Form 8938 for foreign financial assets exceeding $50,000 (single filers) or $100,000 (married filing jointly). Missing either filing triggers automatic penalties, even if you owe zero additional tax.

Mistake 3: Misclassifying Self-Employment Income

OnlyFans creators, freelancers, and other self-employed individuals often receive payments from international platforms or foreign subscribers. Many incorrectly assume that because the payer is located outside the US, the income is foreign source income. In most cases, however, if the creator performed the services inside the United States, the income is still classified as US source income — and is subject to self-employment tax of 15.3% on top of ordinary income tax rates. This misclassification is a frequent audit trigger.

Mistake 4: Forgetting to Claim the Foreign Tax Credit or FEIE

US taxpayers with non-US source income who have already paid foreign taxes on that income are entitled to reduce their US tax liability using the Foreign Tax Credit (Form 1116). Similarly, US expats who qualify as bona fide residents or physical presence test filers can exclude up to $126,500 of foreign earned income using the Foreign Earned Income Exclusion (Form 2555) for 2024. Many taxpayers miss these powerful deductions entirely — resulting in double taxation that was never legally required.

Mistake 5: Not Filing at All After Years Abroad

A significant number of US expats — and even some US-based entrepreneurs with foreign income — simply stop filing US tax returns after moving abroad or starting to earn foreign income. The IRS has aggressive offshore enforcement programs, including information-sharing agreements with over 100 countries under FATCA. The good news is that the IRS offers the Streamlined Filing Procedures, which allow eligible non-willful delinquent filers to come back into compliance with significantly reduced or waived penalties.

How to Handle US Source Income vs Non-US Source Tax Treatment: Step-by-Step

Handling the US source income vs non-US source tax treatment correctly requires a systematic approach. Follow these seven steps to file accurately and avoid costly penalties.

Determine Your US Tax Residency Status.

Your obligations depend on whether you are a US citizen, US permanent resident (green card holder), resident alien, or non-resident alien. US citizens and green card holders owe tax on worldwide income. Non-resident aliens owe tax only on US source income. Tranzesta.com Resident aliens generally follow the same rules as US citizens. Use IRS Form 1040-NR if you are a non-resident alien with US source income.

Identify and Classify Each Income Stream.

List every source of income you received during the tax year. For each item, apply the relevant IRC sourcing rule (861-865) to determine whether it is US source or non-US source. Remember: the classification is based on where the income originates, not where you live.

Check for Tax Treaty Benefits.

If you are a non-resident alien or a US person earning income in a treaty country, check the applicable tax treaty at IRS.gov. Treaties can reduce withholding rates, exempt certain income types, or affect sourcing rules for specific income categories.

Calculate Foreign Tax Credits or FEIE Eligibility.

If you have non-US source income on which you paid foreign taxes, complete Form 1116 to claim the Foreign Tax Credit. If you are a qualifying US expat, consider whether Form 2555 (Foreign Earned Income Exclusion) reduces your US tax liability further.

Complete FBAR and FATCA Filings If Required.

If you have foreign financial accounts that exceeded $10,000 at any point during the year, file FinCEN Form 114 (FBAR) electronically by April 15 (with automatic extension to October 15). Tranzesta.com If foreign financial assets exceed the FATCA thresholds, attach Form 8938 to your federal return.

File the Correct Tax Return. US citizens and residents file Form 1040.

Non-resident aliens file Form 1040-NR. Cannabis business owners in the United States face additional complexity under IRC Section 280E, which disallows most business deductions. If you are self-employed — including as an OnlyFans creator — report all income on Schedule C and calculate self-employment tax on Schedule SE.

Address Delinquent Returns Through the Streamlined Program If Needed.

If you have unfiled returns involving foreign income, the IRS Streamlined Filing Compliance Procedures allow eligible taxpayers to file three years of delinquent returns and six years of FBARs. The Streamlined Domestic Offshore program imposes a 5% miscellaneous offshore penalty. The Streamlined Foreign Offshore program waives penalties entirely for qualifying non-resident filers.

Learn more about IRS Streamlined Filing Procedures directly from the IRS website (opens in new tab).

How Tranzesta Can Help With US Source Income vs Non-US Source Tax Treatment

Navigating the IRS rules for US source income vs non-US source income is genuinely complex — and the cost of getting it wrong can be devastating. That is why thousands of taxpayers across the United States turn to Tranzesta for expert, plain-English tax guidance.

Tranzesta is a US-based tax consultation firm with deep

expertise in cross-border tax issues, Streamlined Filing compliance, OnlyFans and content creator tax services, cannabis industry accounting, and day-to-day business bookkeeping. Our team understands that your income does not fit into a simple box — and neither should your tax strategy.

Here is what Tranzesta can do for you:

Analyze your income streams and correctly classify each as US source or non-US source income under the applicable IRS rules

Prepare Form 1116 (Foreign Tax Credit) and Form 2555 (FEIE) to minimize double taxation on your foreign income

Complete and file FBAR (FinCEN Form 114) and Form 8938 (FATCA) to keep you fully compliant with offshore reporting requirements

Manage your Streamlined Filing if you have delinquent returns and want to come back into compliance with reduced or waived penalties

Handle the unique tax challenges faced by OnlyFans creators, cannabis business owners, and self-employed Americans with international income

Contact our team at hello@tranzesta.com for a free consultation. Visit Tranzesta.com to learn more about our Streamlined Filing and expat tax services.

US Source Income vs Non-US Source Tax Treatment: Expert Tips for 2026

Tax law in this area continues to evolve. Here are the most important insider strategies to optimize your position in 2026 and beyond.

Track your physical location daily.

If you spend significant time in both the US and abroad, keep a contemporaneous travel log. This documentation is essential for proving foreign source income claims and qualifying for the Physical Presence Test (330 full days outside the US) for the Foreign Earned Income Exclusion.

Do not confuse payment location with income source.

An American content creator who receives payments from a UK-based platform but creates all content inside the United States earns US source income. The platform’s location is irrelevant to the sourcing analysis.

Use the foreign tax credit strategically.

In high-tax countries, the Foreign Tax Credit (Form 1116) often eliminates US tax on foreign source income entirely. In low-tax countries, the Foreign Earned Income Exclusion via Form 2555 is often more beneficial.

Cannabis operators: note that the favorable tax treatment available to other businesses under IRC Section 199A (20% QBI deduction) may be limited by Section 280E for cannabis businesses. However, correctly sourcing your income across state lines can still reduce your effective federal tax rate.

Consider your state tax obligations.

Several US states — including California — tax worldwide income and do not conform to federal FEIE rules. Moving abroad does not automatically cut California’s tax nexus. Always consult a qualified tax professional about your specific state situation.

Act quickly on delinquent returns.

The IRS Streamlined program is available now — but there is no guarantee it will remain open indefinitely. Taxpayers who proactively come forward receive far better treatment than those who are discovered through IRS enforcement action.

The tax experts at Tranzesta stay current with every IRS update, Revenue Ruling, and treaty change that affects US source income taxation. We translate these developments into clear, actionable strategies for every client we serve across the United States and globally.

Conclusion

Understanding US source income vs non-US source tax treatment is not just an academic exercise — it is a critical compliance requirement that affects your bottom line. Here are the three most important takeaways from this guide:

The IRS taxes US citizens and green card holders on their worldwide income.

Foreign source income is not automatically exempt — it must be reported, with available credits or exclusions applied strategically.

Income sourcing is determined by the nature

of the income, not simply where the taxpayer lives. Tranzesta.com Applying the correct IRC Section 861-865 sourcing rule is essential to accurate reporting.

Relief is available. Whether you need the Foreign Tax Credit,

the Foreign Earned Income Exclusion, or the IRS Streamlined Filing Procedures, there are legitimate tools to reduce or eliminate double taxation and come back into full compliance.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

US source income is income that originates inside the United States, such as wages earned for work performed in the US, dividends from US corporations.

Yes. US citizens and permanent residents must report and pay US tax on their worldwide income, including income earned in other countries. However, you are not necessarily double-taxed. The Foreign Tax Credit (Form 1116) allows you to offset US taxes with foreign taxes already paid on the same income. Additionally,

The IRS determines income sourcing based on the type of income under IRC Sections 861 through 865. For . For dividends, it depends on the country of incorporation. For rents and royalties, it is based on property location or where intangibles are used.

The Foreign Tax Credit is a US tax provision under IRC Section 901 that allows US taxpayers to reduce their US tax liability by the amount of income taxes paid to foreign governments on non-US source income. You claim it using Form 1116.

The Streamlined Foreign Offshore program is available to US expats who have lived outside the United States for at least one of the past three years and whose failure to file was non-willful. It requires filing three years of delinquent tax returns and six years of FBARs, with penalties completely waived. Tranzesta specializes in Streamlined Filing and can guide you through the process confidentially and efficiently.