Every year, thousands of US taxpayers are blindsided

by a 24% tax hit they never saw coming. If you have ever received a payment for freelance work, content creation, or a business service and found that a chunk was withheld before it ever reached your bank account, you may have already encountered backup withholding. Understanding backup withholding IRS requirements is not just helpful — it is essential if you want to keep your full earnings and stay compliant with federal tax law.

In this guide, you will learn exactly what backup

withholding is, when the IRS requires it, who it affects, and how to avoid it. Whether you are an OnlyFans creator, a cannabis business owner, a freelancer, or a self-employed professional in the United States, this article gives you everything you need to know — in plain English.

What Is Backup Withholding and Why Does It Matter?

Backup withholding is a mandatory federal tax withholding that payers — such as banks, businesses, or payment platforms — must apply to certain payments when the IRS requires it. The current backup withholding rate is 24%, and it applies to payments like interest, dividends, self-employment income, and freelance payments reported on a 1099 form.

The Basic Definition

When you receive certain types of income in the United States, the payer is normally not required to withhold taxes upfront. However, backup withholding kicks in when the IRS identifies a problem with your tax account — such as a missing taxpayer identification number (TIN) or a history of underreporting income. In those cases, the payer must withhold 24% of the gross payment and send it directly to the IRS on your behalf.

Think of it as the IRS ensuring it gets paid before the money ever reaches you. For many self-employed individuals and content creators, this can come as a serious financial shock, especially if you depend on that income for monthly expenses.

Why Should You Care About Backup Withholding?

Backup withholding affects a wider audience than most people realize. It applies to freelancers, gig workers, small business owners, content creators, and even investors receiving dividends. For OnlyFans creators, for example, platforms may be required to apply backup withholding if you have not submitted a valid W-9 form with your correct TIN. For cannabis businesses — already navigating complex tax restrictions under Section 280E of the IRS tax code — an additional 24% withholding on top of other tax burdens can severely strain cash flow.

Therefore, knowing when backup withholding applies, and how to prevent it, is a critical part of managing your finances as a self-employed individual in the USA.

What Are the IRS Backup Withholding Requirements?

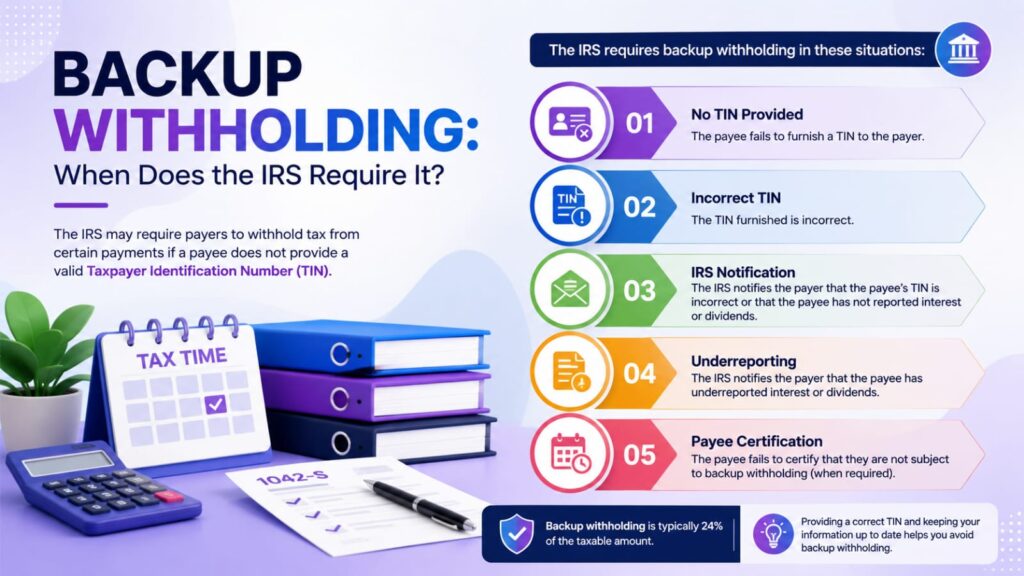

The IRS requires backup withholding in specific, well-defined situations. Understanding these triggers helps you take proactive steps to avoid them. The legal authority for backup withholding comes from Internal Revenue Code (IRC) Section 3406.

When Does Backup Withholding Apply?

The IRS mandates backup withholding in the following situations:

You failed to provide your TIN (Social Security Number or Employer Identification Number) to the payer.

You provided an incorrect TIN that does not match IRS records.

The IRS has notified the payer that you are subject to backup withholding due to underreporting interest or dividend income.

You failed to certify that you are not subject to backup withholding on your W-9 form.

The IRS notifies the payer to begin backup withholding because you have not reported all your interest and dividends on your tax return.

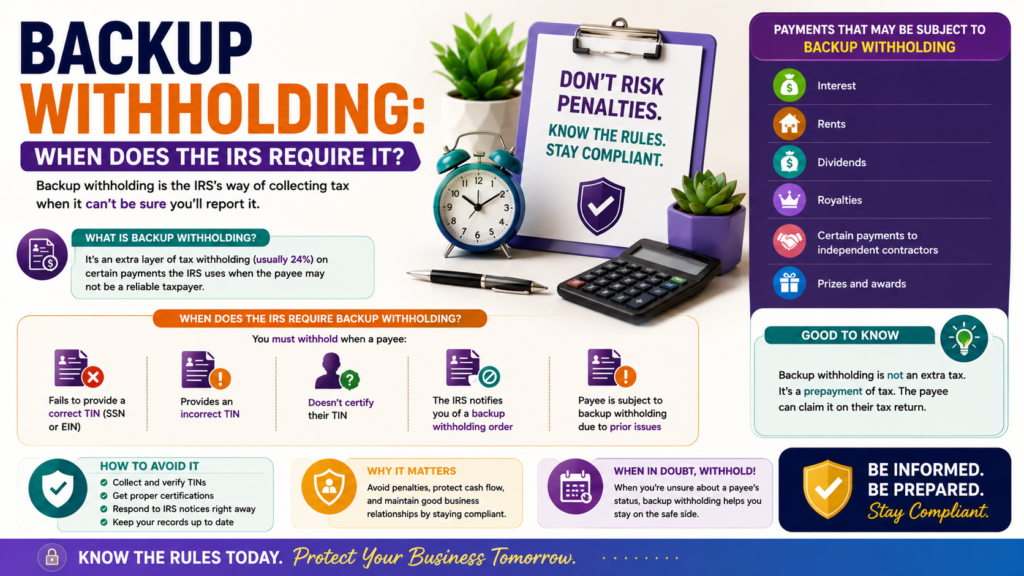

Which Types of Payments Are Subject to Backup Withholding?

Not every type of income is subject to this rule. However, the following payments are covered under backup withholding IRS requirements:

Additionally, real estate transactions reported on Form 1099-S and certain other payments can also trigger backup withholding. If your income falls into any of these categories, you need to make sure your tax information is accurate and on file with every payer.

The W-9 Form: Your First Line of Defense

The most important step in avoiding backup withholding is completing a W-9 form — the Request for Taxpayer Identification Number and Certification. When you provide a payer with a completed and accurate W-9, you certify your TIN and confirm that you are not subject to backup withholding. Payers are required to request this form before making payments, and you are responsible for submitting it promptly and accurately.

For US taxpayers working with multiple clients or platforms, you will likely need to submit a separate W-9 to each one. Keeping a completed, current W-9 ready to send is a simple but powerful way to protect your income.

Common Mistakes That Trigger Backup Withholding

Many US taxpayers end up subject to backup withholding not because they are dishonest, but because they made avoidable administrative errors. Here are the most common mistakes and how they lead to that 24% withholding.

Mistake 1: Not Submitting a W-9 to Your Payer

This is the single most common trigger for backup withholding among freelancers and content creators. If you begin earning income from a client, platform, or business and do not submit a W-9, the payer is legally required to withhold 24% of all future payments. Many new OnlyFans creators or first-time contractors skip this step because they are not aware it is required. As a result, they receive significantly less than expected.

Mistake 2: Using an Incorrect or Outdated TIN

Even if you submit a W-9, providing the wrong Social Security Number or EIN can cause a TIN mismatch. The IRS cross-references the information you provide against its own records. If there is a discrepancy, the IRS will send the payer a “B Notice,” which requires them to begin backup withholding within 30 days. This is why it is critical to double-check your TIN every time you submit a W-9.

Mistake 3: Failing to Report All Interest and Dividends

The IRS monitors income reporting closely. If you underreport interest or dividend income on your tax return — even accidentally — the IRS may determine that you are subject to backup withholding. They notify the payer directly, and the withholding begins. This situation is especially common among investors or passive income earners who overlook small interest payments from multiple accounts.

Mistake 4: Not Responding to IRS Notices Promptly

When the IRS sends a backup withholding notice, ignoring it or delaying your response makes the situation worse. For example, if the IRS sends a “CP2100” or “CP2100A” notice to your payer indicating a TIN mismatch, the payer has strict timelines to follow. If you do not address the issue quickly — by submitting a corrected W-9 or contacting the IRS — the withholding continues indefinitely until the issue is resolved.

Mistake 5: Assuming Backup Withholding Does Not Apply to You

Many self-employed individuals and small business owners assume this only happens to other people. In reality, backup withholding can affect anyone who receives 1099-reportable income. Cannabis business owners, for instance, often focus on the complexities of Section 280E and overlook backup withholding risks that may arise from business transactions. Being proactive is always better than reacting after the withholding has already started.

How to Stop or Prevent Backup Withholding: A Step-by-Step Guide

Whether you are trying to prevent backup withholding before it starts or stop it once it has already been triggered, the steps below will help you get back on track with the IRS.

Submit a completed W-9 form to every payer immediately.

Make sure your legal name, address, and TIN match exactly what is on file with the IRS and Social Security Administration. Do not leave any fields blank.

Verify your TIN is correct.

If you are using a Social Security Number, confirm it matches your SSA records. If you are using an EIN, log in to the IRS Business Tax Account portal to verify your information is current and accurate.

File all overdue tax returns.

If backup withholding was triggered because you underreported income in a prior year, filing amended or past-due returns is an essential step. The IRS cannot remove the withholding requirement until your account is in compliance.

Respond immediately to any IRS notices.

If you receive a CP2100 or similar notice, treat it as urgent. Contact the payer to submit a corrected W-9, and if needed, reach out directly to the IRS to resolve the discrepancy. Acting fast reduces the amount of income withheld.

Request a backup withholding release from the IRS.

Once you have corrected the underlying issue — whether it was a missing TIN, underreported income, or a prior mismatch — you can request that the IRS stop the backup withholding. This typically involves filing the correct paperwork and ensuring your tax account is current and accurate.

Claim withheld amounts on your tax return.

Any backup withholding applied during the tax year is reported on Line 25c of Form 1040. You can claim these withheld amounts as a tax payment, which may reduce your overall tax liability or generate a refund. Keep all 1099 forms that show withholding amounts for your records.

Work with a qualified tax professional.

Resolving backup withholding issues with the IRS can be complex, especially if multiple payers are involved or if the issue stems from a prior audit or underreporting flag. A professional who understands IRS procedures can save you time, reduce penalties, and ensure the issue is resolved correctly the first time.

How Tranzesta Can Help With Backup Withholding IRS Requirements

Dealing with backup withholding issues on your own can be frustrating and time-consuming. Tranzesta is a US-based tax consultation firm that specializes in helping self-employed individuals, content creators, cannabis business owners, and US expats navigate complex IRS rules — including backup withholding.

Our team understands that backup withholding is not just a paperwork problem. For many of our clients — OnlyFans creators who depend on consistent platform payouts, or cannabis businesses already burdened by federal tax restrictions — a 24% withholding can have a very real impact on cash flow and financial stability. That is why we approach each situation with precision and urgency.

At Tranzesta, we help clients with:

Reviewing and correcting W-9 submissions to prevent TIN mismatches.

Responding to IRS CP2100 and B Notice situations on your behalf.

Filing amended or delinquent tax returns to bring your IRS account into good standing.

Reclaiming backup withholding amounts through your annual tax return.

Ongoing bookkeeping and compliance support to prevent future withholding triggers.

We also offer Streamlined Filing Services for US expats who may face international variations of withholding compliance issues. No matter where you are in the USA — or abroad — our team is ready to help.

Contact our team at hello@tranzesta.com for a free consultation. Visit Tranzesta.com to learn more about our business tax and compliance services.

Backup Withholding IRS Requirements: Expert Tips for 2026

Staying ahead of backup withholding means being proactive, not reactive. Here are the top strategies our tax professionals at Tranzesta recommend for US taxpayers heading into 2026.

Keep one master W-9 on file and update it any time your legal name, address, TIN, or business structure changes. Send the updated form to all active payers immediately.

Set a calendar reminder to verify your TIN with the IRS once per year, especially if you recently formed a new LLC, S-Corp, or sole proprietorship in the United States.

Review all 1099 forms received each year before filing your return. If any show backup withholding in Box 4, make sure you report that amount correctly on Form 1040, Line 25c.

If you are an OnlyFans creator or other digital content producer, check the payment settings of every platform you use. Many platforms — including Fansly, Patreon, and subscription services — have their own W-9 submission processes.

For cannabis business owners, work with a tax professional who understands the intersection of Section 280E restrictions and general withholding rules. The financial stakes are higher in this industry, and errors are more costly.

Do not assume that small payments are exempt. Backup withholding applies regardless of the payment amount, as long as the payment type is covered under IRS rules.

Additionally, if you receive a notice from any payer stating that your TIN could not be verified, treat it as a top-priority issue. Most backup withholding problems can be resolved quickly when addressed early — but they escalate rapidly when ignored.

Conclusion: Take Control of Your Tax Compliance

Backup withholding is one of the most misunderstood — and most preventable — tax issues facing self-employed individuals and small business owners in the United States. The three most important takeaways from this guide are: first, always submit a complete and accurate W-9 to every payer; second, respond immediately to any IRS or payer notices about a TIN mismatch or withholding requirement; and third, claim any backup withholding already applied to your income on your annual tax return.

The IRS has clear rules around backup withholding, and the good news is that following them is not complicated — as long as you stay organized and act quickly when issues arise. Whether you are an OnlyFans creator, a cannabis operator, a freelancer, or a US expat, the key is to be proactive before backup withholding ever begins.

Tranzesta is here to make that process easier. Our team of US tax professionals handles everything from W-9 reviews to IRS notice responses, so you can focus on running your business instead of fighting with tax paperwork.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

Backup withholding is triggered when a taxpayer fails to provide a correct Taxpayer Identification Number (TIN) to a payer, provides an incorrect TIN that does not match IRS records, or has been notified by the IRS that they underreported interest or dividend income on a prior tax return. It is also triggered when a taxpayer fails to certify their exempt status on a W-9 form. The payer is then legally required to withhold 24% of all covered payments and send that amount directly to the IRS.

You will know you are subject to backup withholding if the IRS sends a notice to your payer — typically a CP2100 or CP2100A notice — indicating a TIN mismatch or underreported income. Your payer may also notify you directly and request a corrected W-9. Additionally, if you receive a 1099 form at tax time and notice an amount in Box 4 (Federal income tax withheld), that indicates backup withholding was applied to your payments during the year.

The backup withholding rate for 2026 is 24% of the gross payment. This rate is set by the IRS and applies to all payments subject to backup withholding, including freelance income, interest, dividends, and other 1099-reported income. The 24% rate has been in effect since the Tax Cuts and Jobs Act of 2017. It applies to the full payment amount before any deductions, which means it can represent a significant portion of your earnings if triggered.

Yes, you can recover backup withholding amounts when you file your annual federal tax return. Any backup withholding applied during the tax year is reported on Form 1040, Line 25c, as a federal tax payment. This reduces your overall tax liability for the year. If the withheld amount exceeds what you owe in taxes, you may receive a refund. To claim it correctly, make sure you have all 1099 forms showing the withholding amount in Box 4.

Backup withholding can apply to payments made through third-party payment platforms like PayPal, Venmo for Business, Stripe, and Cash App for Business. These platforms are required to report business transactions on Form 1099-K and may also be subject to backup withholding rules if you have not provided a valid W-9. If you use any payment platform to receive business income in the United States, you should submit a W-9 to each platform to ensure your TIN is on file and to avoid backup withholding.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation