Cannabis intellectual property is worth millions

— but most dispensary owners and cannabis brand operators in the United States are leaving significant tax savings on the table because they do not structure royalties and licensing agreements correctly. Getting the cannabis royalties licensing tax structure right from the start can dramatically reduce your federal tax burden, protect your intellectual property assets, and create a defensible business model that survives IRS scrutiny. However, doing it wrong exposes you to back taxes, penalties, and the unforgiving reach of IRC Section 280E.

In this guide, you will learn exactly what cannabis royalties and licensing agreements are, how the and a step-by-step plan to set up a tax-efficient licensing arrangement. You will also discover how Tranzesta’s cannabis accounting specialists help operators across the USA build compliant, tax-optimized IP structures.

What Are Cannabis Royalties and Licensing Agreements?

Cannabis royalties and licensing agreements are legal contracts in which the owner of intellectual property — such as a brand name, cultivation technique, proprietary strain genetics, processing formula, or operating system — grants another party the right to use that IP in exchange for royalty payments. These structures are common in franchising, brand licensing, and management service arrangements across the cannabis industry in the United States.

For cannabis businesses, IP licensing has become especially important because federal prohibition creates unusual structural pressures. Multi-state operators (MSOs) frequently use licensing entities to separate their brand and IP assets from their licensed cannabis operations. This separation can, when structured properly, allow certain income streams to escape the reach of Section 280E — the IRS provision that denies standard business deductions for cannabis trafficking businesses.

Why Does the Tax Structure of Cannabis Royalties Matter?

Under IRC Section 280E, a cannabis dispensary or cultivator cannot deduct ordinary business expenses such as rent, salaries, marketing, or management fees. However, a properly structured IP holding company that licenses intangible assets — and does not itself touch cannabis — may not be subject to 280E. As a result, royalty income received by the IP entity could potentially be taxed as ordinary business income with full deductions available. This creates a powerful tax planning opportunity, but only when the structure is properly established and documented.

The IRS has increasingly scrutinized these arrangements. Therefore, understanding the precise legal and tax requirements for a defensible cannabis royalties licensing tax structure is essential for any multi-entity cannabis operation in the USA.

What Types of Cannabis IP Can Be Licensed?

Cannabis businesses in the United States can license a wide range of intellectual property assets. These include: trade names and trademarks, proprietary strain genetics and cultivar names, processing and extraction methods, standard operating procedures (SOPs) and training systems, software and point-of-sale systems, and customer loyalty program frameworks. Each of these IP categories can generate royalty income for the holding entity while providing legitimate business value to the licensed operator.

How Does the IRS Tax Cannabis Royalty and Licensing Income?

The IRS taxes cannabis royalty and licensing income according to its source and the nature of the entity receiving it. Understanding this distinction is the foundation of any effective cannabis royalties licensing tax structure.

Royalty Income Taxed as Ordinary Income

Royalty income is generally classified as ordinary income under the Internal Revenue Code. For an individual or pass-through entity (such as an LLC or S-corporation) receiving royalties, this income flows to the owner’s personal tax return and is taxed at ordinary income rates — up to 37% at the federal level for 2026. Additionally, if the royalty income arises from an active trade or business, it may also be subject to self-employment tax of 15.3% on the first $168,600 of net earnings (2024 threshold, adjusted annually by the IRS).

The 280E Boundary: What Is and Is Not Subject to It

IRC Section 280E (Internal Revenue Code Section 280E) applies to businesses engaged in trafficking Schedule I or II controlled substances. A critical question in cannabis IP structuring is whether the IP holding entity itself qualifies as a trafficking business. If the holding company licenses trademarks and SOPs but never handles, grows, processes, or sells cannabis, the IRS may determine it is not subject to 280E. However, the IRS has challenged these structures when it determines the IP entity lacks independent economic substance — meaning it exists solely for tax avoidance rather than genuine business purposes.

Passive Versus Active Royalty Income

Royalty income can be classified as either passive or active depending on the taxpayer’s involvement. Passive royalty income — earned from intellectual property the owner is not actively managing — may be subject to the 3.8% Net Investment Income Tax (NIIT) under IRC Section 1411 for individuals with modified adjusted gross income above $200,000 (single) or $250,000 (married filing jointly). Active royalty income, where the licensor materially participates in the business, avoids the NIIT but may be subject to self-employment tax. Your cannabis royalties licensing tax structure should account for this distinction from day one.

Ordinary income tax rates apply (up to 37% federal)

Self-employment tax may apply if income is from active business (15.3% up to threshold)

3.8% NIIT may apply on passive royalty income above income thresholds

280E may not apply to a non-plant-touching IP entity — but only with proper structure and substance

State tax treatment varies significantly across US jurisdictions

Common Mistakes in Cannabis Royalty and Licensing Tax Structures

Most structuring failures in cannabis licensing arrangements come down to a handful of predictable errors. Avoiding these mistakes is essential to a durable cannabis royalties licensing tax structure.

Mistake 1: Creating a Sham IP Entity Without Economic Substance

The most dangerous mistake is forming an IP holding company purely to shift income away from the 280E-burdened cannabis entity without giving the IP company genuine economic purpose. The IRS applies the economic substance doctrine to evaluate whether a transaction or structure has a meaningful non-tax business purpose. If the IP entity has no employees, no management activity, no actual IP development cost, and exists only on paper, the IRS will disregard it entirely — collapsing it back into the cannabis operation and applying 280E to all income. The result is large back-tax assessments plus penalties.

Mistake 2: Setting Non-Arm’s-Length Royalty Rates

When related parties transact with each other — for example, when the cannabis operator pays royalties to a commonly owned IP holding company — the IRS requires the royalty rate to reflect what unrelated parties would negotiate in an arm’s-length transaction. Charging an above-market royalty rate artificially shifts income to the low-tax entity and reduces the cannabis operator’s taxable income, which the IRS views as an impermissible tax shelter. Royalty rates must be supported by a qualified transfer pricing analysis, particularly for multi-state operators with significant IP values.

Mistake 3: Failing to Document IP Ownership and Transfer

Before a royalty structure can function legally, the intellectual property must be formally owned by the licensing entity. This requires written IP assignment agreements, trademark registrations (where applicable), and documentation of when and how the IP was developed or acquired. Many cannabis operators form a holding company and begin charging royalties without ever formally transferring the IP to that entity. Without clean legal title, the licensing arrangement has no valid foundation.

Mistake 4: Ignoring State Tax Consequences

While a non-plant-touching IP entity may escape federal 280E, state tax treatment varies dramatically across US jurisdictions. Some states impose their own version of 280E or require combined reporting, which consolidates related entities for state tax purposes. California, for example, uses combined reporting for corporate groups, which may effectively eliminate the state tax benefit of separating your IP entity. A complete cannabis royalties licensing tax structure analysis must include state-by-state review.

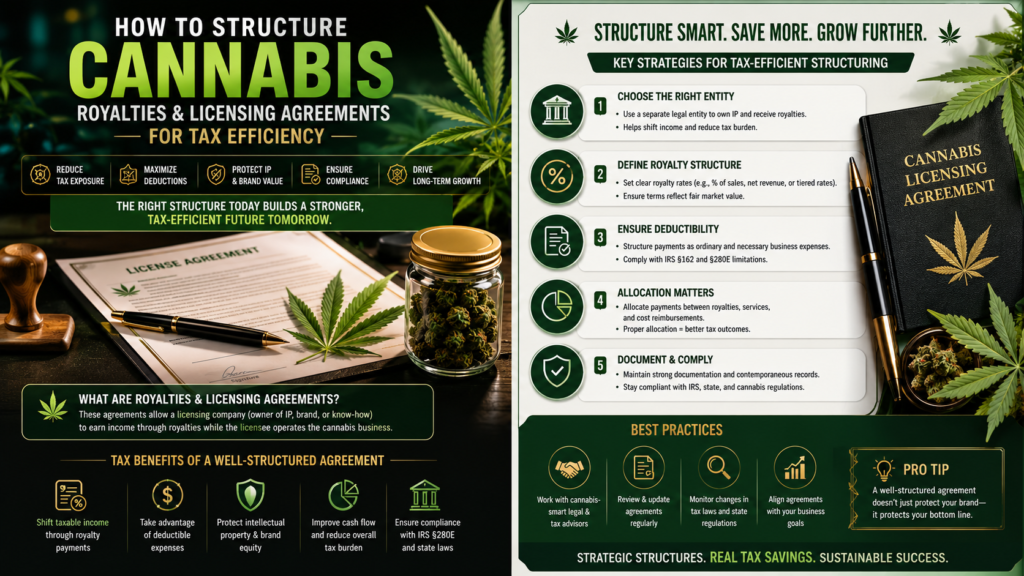

How to Set Up a Cannabis Royalties Licensing Tax Structure: Step-by-Step

Building a defensible cannabis royalties licensing tax structure requires careful legal and accounting coordination. Follow these six steps to establish a compliant arrangement.

Step 1: Identify and Inventory Your Cannabis IP Assets.

Begin by cataloging all intellectual property your business owns — trademarks, trade names, proprietary cultivation methods, SOPs, recipes, and software systems. Assign a fair market value to each asset, supported by a qualified IP valuation professional if the amounts are material. This inventory is the foundation of your licensing structure.

Step 2: Form a Separate IP Holding Entity.

Create a distinct legal entity — typically an LLC or C-corporation — to hold your cannabis IP assets. This entity should be domiciled in a state with favorable tax treatment. The entity must have independent economic substance: real management activity, documented decision-making, and compensation arrangements that reflect genuine services rendered.

Step 3: Execute Formal IP Transfer and Assignment Agreements.

Transfer each identified IP asset to the holding entity through a written assignment agreement. For trademarks, file the assignment with the USPTO. Document the consideration paid for the transfer and record it on both entities’ books. This formal transfer is legally required before any royalty arrangement can be valid.

Step 4: Establish Arm’s-Length Royalty Rates.

Work with a transfer pricing specialist or cannabis tax advisor to determine market royalty rates for each IP category. Royalty rates for cannabis trademarks and brands typically range from 3% to 8% of gross revenue, though rates vary based on brand strength and market conditions. Document the analysis in writing and review it annually.

Step 5: Execute a Written License Agreement.

Draft a formal licensing agreement between the IP holding entity and each cannabis operator. The agreement must specify the licensed IP, the royalty rate and payment schedule, the licensor’s quality control obligations, and the term and termination provisions. Quality control language is especially important for trademark licenses — without it, the trademark may be invalidated.

Step 6: Maintain Ongoing Documentation and Compliance.

Pay royalties on schedule according to the agreement, issue proper invoices, and record all transactions in both entities’ accounting systems. The IP entity should file its own tax returns, hold board meetings, maintain bank accounts, and function as a genuine independent business. Annual review by a cannabis tax specialist like Tranzesta helps ensure the structure remains defensible.

How Tranzesta Helps Cannabis Operators Build Tax-Efficient Licensing Structures

Tranzesta is a US-based tax consultation firm specializing in cannabis industry accounting, including multi-entity structuring, 280E compliance, and royalty agreement tax planning. Our cannabis tax specialists work with dispensary operators, cultivators, multi-state operators, and cannabis brands across the United States to build IP licensing structures that reduce tax exposure while surviving IRS scrutiny.

When you work with Tranzesta.com we begin with a complete review of your existing entity structure and IP assets. We then design a licensing arrangement that reflects arm’s-length economics, documents genuine business substance, and accounts for both federal and state tax consequences. We also provide ongoing bookkeeping and compliance services to ensure the structure remains defensible year after year.

Tranzesta’s cannabis accounting services include:

IP entity formation and structuring advice, transfer pricing analysis and royalty rate benchmarking, 280E compliance reviews, multi-state tax planning, and full-service bookkeeping for cannabis operators in the USA. Learn more about cannabis accounting and tax strategy services at Tranzesta.com.

Ready to structure your cannabis royalties and licensing agreements correctly?

Contact our cannabis tax specialists at hello@tranzesta.com for a free consultation.

Visit Tranzesta.com to learn more about our cannabis accounting services.

Cannabis Royalties Licensing Tax Structure: Expert Tips for 2026

Beyond the foundational steps, experienced cannabis tax professionals apply advanced strategies to maximize the value of a licensing structure. Here are key insights from Tranzesta’s cannabis accounting team.

Consider a C-Corporation for the IP Entity in Certain Situations.

A C-corporation pays a flat 21% federal corporate tax rate. If your IP entity generates substantial royalty income that would otherwise be taxed at your personal rate of up to 37%, electing corporate taxation for the IP entity may produce significant savings — particularly for high-volume multi-state operators.

Use Cost Segregation and R&D Credits at the IP Entity Level.

If your IP entity funds cannabis-related research and development, it may qualify for the federal R&D Tax Credit under IRC Section 41. Because the IP entity is not subject to 280E (assuming proper structure), it can claim this credit against its tax liability — something the cannabis operator could never do.

Leverage State Decoupling Strategically.

Several US states do not conform to 280E at the state level. In those states, the cannabis operator can deduct royalty payments as an ordinary business expense on its state return. This creates a state-level deduction that further reduces the overall tax burden of the two-entity structure.

Review Royalty Rates Annually.

Brand value, revenue, and market conditions change. An arm’s-length royalty rate from 2023 may no longer reflect current market conditions in 2026. Annual rate reviews — documented in writing — demonstrate that your licensing arrangement reflects genuine economic terms rather than a static tax shelter.

Avoid Commingling Funds Between Entities.

One of the fastest ways to destroy the legal integrity of a two-entity structure is to allow money to flow informally between the IP entity and the cannabis operator. All royalty payments must follow the schedule in the license agreement, be invoiced properly, and be recorded in both sets of books.

Conclusion: Build Your Cannabis Licensing Tax Strategy Before the IRS Looks

A well-designed cannabis royalties licensing tax structure is one of the most powerful tools available to cannabis operators in the United States. The three most important takeaways from this guide are: first, a non-plant-touching IP holding entity can potentially escape 280E — but only with genuine economic substance and arm’s-length pricing; second, documentation is everything — from formal IP assignments to written royalty rate analyses; and third, state-level tax consequences require separate analysis because federal planning does not automatically translate to state tax savings.

Cannabis licensing structures are complex, and the IRS has become increasingly aggressive in challenging arrangements that lack substance. Additionally, tax law continues to evolve as more US states legalize cannabis and federal rescheduling discussions continue. Proactive planning with a cannabis tax specialist is far more cost-effective than reacting to an IRS challenge after the fact.

Ready to get expert help structuring your cannabis licensing agreements?

Email us at hello@tranzesta.com or visit Tranzesta.com

to schedule your free tax strategy session today.

FAQs

the IRS evaluates the economic substance of the arrangement. If the IP entity lacks genuine independent business purpose — real management, documented IP ownership, and arm’s-length royalty rates — the IRS may disregard the structure and apply 280E to all related income. Always work with a cannabis tax specialist to verify compliance.

the IRS evaluates the economic substance of the arrangement. If the IP entity lacks genuine independent business purpose — real management, documented IP ownership, and arm’s-length royalty rates — the IRS may disregard the structure and apply 280E to all related income. Always work with a cannabis tax specialist to verify compliance.

A cannabis company subject to 280E cannot deduct most ordinary business expenses, but royalty payments may qualify as a Cost of Goods Sold component in limited circumstances, or they may be treated as a non-deductible operating expense at the federal level. However, in US states that have decoupled from 280E — including California and Colorado — the cannabis operator can deduct royalty payments on its state tax return. The deductibility of royalty payments is one of the most nuanced issues in cannabis tax planning and requires entity-specific analysis.

An arm’s-length royalty rate for a cannabis brand is the rate that two unrelated parties would negotiate in an strength. However, rates for proprietary cultivation methods, extraction formulas, or operating systems may differ significantly. The IRS requires royalty rates between related parties to reflect arm’s-length terms, supported by a documented transfer pricing analysis.

rates and payment terms, a transfer pricing analysis documenting that royalty rates are arm’s-length, invoices and payment records for all royalty transactions, financial statements for both entities showing royalties as income and expense respectively, and evidence of the IP entity’s genuine business activity, including board minutes, bank accounts, and management records.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation