Over 65 countries have signed tax treaties with the United States

yet the vast majority of foreign nationals working in the USA never claim the benefits they are legally entitled to. If you are a foreign individual earning income inside the United States, understanding tax treaty benefits for foreign individuals in the USA could save you thousands of dollars in unnecessary withholding taxes every single year.

In this complete 2026 guide,

you will learn exactly what US tax treaties are, which countries have them, how they reduce or eliminate US withholding taxes, which specific income types they cover, and how to claim them on your US tax return. We will also cover the most common mistakes foreign nationals make — and explain how Tranzesta helps foreign individuals navigate these rules with confidence.

Whether you are working in the United States on a visa,

earning US-source income as a non-resident, or simply trying to understand your obligations to the IRS, this guide is your definitive resource. Let us start with the basics.

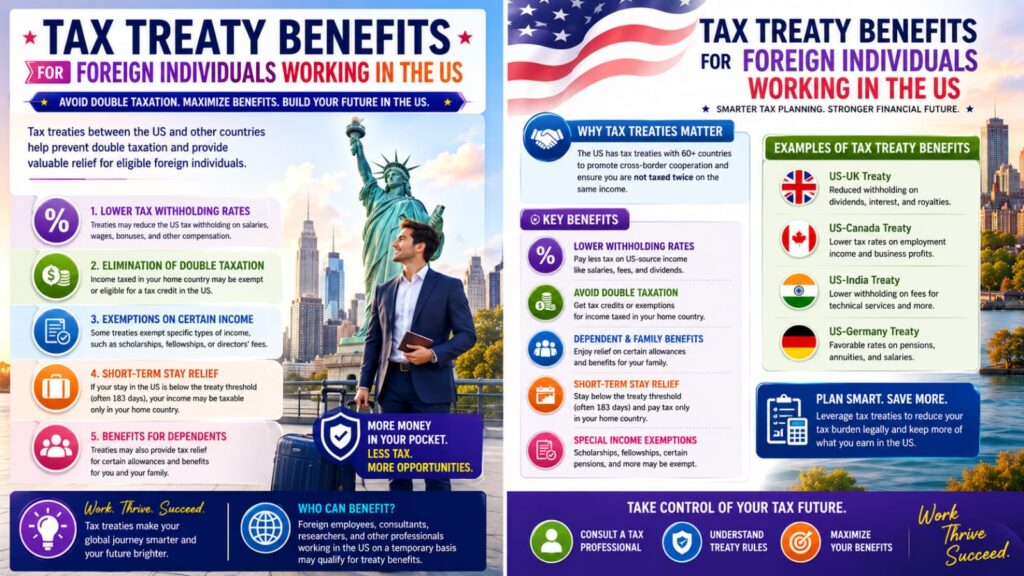

What Are Tax Treaty Benefits for Foreign Individuals in the USA?

Tax treaty benefits for foreign individuals in the USA are provisions in bilateral tax agreements that reduce or eliminate the US tax — particularly withholding tax — that would otherwise apply to income earned by foreign nationals inside the United States. These treaties are negotiated between the US government and individual foreign governments to prevent double taxation and encourage cross-border economic activity.

Without a treaty, the IRS imposes a flat 30% withholding tax on most US-source income paid to non-resident aliens (NRAs) — including wages, dividends, interest, royalties, and certain other income types. Tax treaties reduce this rate significantly, often to 15%, 10%, or even 0% on specific income categories. For many foreign individuals, the difference between the 30% statutory rate and the treaty rate represents a life-changing amount of money.

Who Qualifies as a Non-Resident Alien (NRA)?

A non-resident alien (NRA) is a foreign national who does not pass either the Green Card Test or the Substantial Presence Test for US tax purposes. The Substantial Presence Test requires physical presence in the United States for at least 31 days in the current year and 183 days over the prior three-year period using a weighted formula. If you do not meet either test, the IRS treats you as a non-resident alien — and tax treaty rules become critically important to your situation.

NRAs are only taxed by the US on their US-source income, unlike US citizens and resident aliens who owe tax on worldwide income. However, the 30% withholding rate on that US-source income can be punishing without treaty relief. Therefore, claiming your treaty benefits correctly is not optional — it is essential.

Which Countries Have Tax Treaties With the United States?

As of 2026, the United States has income tax treaties with over 65 countries. Major treaty partners include the United Kingdom, Canada, Germany, France, Japan, India, China, Australia, the Netherlands, and Mexico. Each treaty is unique — the rates and exemptions vary significantly by country and income type. The IRS maintains a full list of US tax treaties and their applicable rates at IRS.gov.

Notably, many popular countries do NOT have a tax treaty with the United States. For example, Brazil, Saudi Arabia, the UAE, and most of Africa and Latin America lack US tax treaties. Foreign individuals from non-treaty countries generally face the full 30% withholding rate on US-source passive income.

How Do US Tax Treaty Benefits Work? Key Rules and Requirements

US tax treaty benefits work by overriding the standard 30% IRS withholding rate with a lower treaty rate — or a full exemption — for specific income types paid to qualifying residents of treaty countries. The treaty itself defines the rules; IRS Publication 901 and the individual treaty text govern the specifics.

Income Types Commonly Covered by US Tax Treaties

US tax treaties typically cover the following income categories, with reduced withholding rates for treaty country residents:

Dividends: Standard 30% withholding reduced to 5%–15% for most treaty countries. Some treaties allow 0% for certain qualified dividends.

Interest: Often reduced to 0% under treaties with major partners like the UK, Germany, and Canada, compared to the standard 30%.

Royalties: Standard 30% typically reduced to 0%–10% for intellectual property royalties under most major treaties.

Wages and personal service income: Treaties often exempt wages from US tax when the foreign individual is present in the US for fewer than 183 days and their employer is not a US entity.

Student and trainee income: Many treaties include specific exemptions for students, trainees, and teachers from treaty countries studying or training in the United States.

Pensions and social security: Reduced or zero withholding on pension distributions for residents of many treaty countries.

The Residency and Limitation on Benefits Requirements

To claim treaty benefits, you must be a bona fide resident of the treaty country — not simply a passport holder. Most modern US tax treaties include a Limitation on Benefits (LOB) clause, which prevents residents of third countries from using treaty networks for tax avoidance. For example, a citizen of a non-treaty country who holds a passport from a treaty country cannot generally claim that treaty’s benefits.

Additionally, you must provide the correct documentation

to the US withholding agent (typically your employer or financial institution) before treaty benefits are applied. The primary form for this purpose is Form W-8BEN — Certificate of Foreign Status of Beneficial Owner. Individuals complete Form W-8BEN, while foreign entities complete Form W-8BEN-E. These forms must be updated every three years and whenever your circumstances change.

Importantly, even if your treaty rate reduces withholding

to zero, you may still be required to file a US tax return — specifically Form 1040-NR — to report your US-source income and formally claim the treaty position. Tranzesta.com Filing a return protects your treaty claim and creates a clear record with the IRS.

For a complete list of US tax treaty rates by country and income type, visit the IRS Tax Treaties page at IRS.gov (opens in new tab).

Common Mistakes Foreign Individuals Make When Claiming Treaty Benefits

Claiming tax treaty benefits incorrectly — or failing to claim them at all — creates serious financial and legal consequences. Here are the five most damaging mistakes foreign individuals make in the United States.

Mistake 1: Failing to Submit Form W-8BEN to the Withholding Agent

The most common and most expensive mistake is simply never providing Form W-8BEN to the US payer. Without this form, the withholding agent is legally required to withhold at the full 30% statutory rate — regardless of whether a lower treaty rate applies. Many foreign individuals working in the United States are unaware of this requirement and unknowingly overpay by tens of thousands of dollars annually. The remedy is straightforward: submit Form W-8BEN before your first payment and update it every three years.

Mistake 2: Using the Wrong Treaty Article

Every tax treaty is organized into articles, and each article covers a different income type. For example, Article 10 of many treaties covers dividends, Article 11 covers interest, Article 12 covers royalties, and Article 15 covers employment income. Claiming the wrong article on Form W-8BEN or Form 8833 — or citing the correct article incorrectly — can result in a rejected treaty claim, an IRS audit, or penalties. Always verify the exact article number and reduction rate from the official treaty text or an IRS-approved summary.

Mistake 3: Assuming Visa Status Determines Treaty Eligibility

Your visa type does not determine your tax treaty eligibility — your tax residency status does. A foreign national on an F-1 student visa is typically a non-resident alien for US tax purposes during the first five years in the United States, making them potentially eligible for student treaty exemptions. However, an H-1B visa holder who has passed the Substantial Presence Test is treated as a US resident for tax purposes and generally cannot claim treaty benefits as a non-resident alien. Conflating visa status with tax residency is a frequent and costly error.

Mistake 4: Not Filing Form 8833 for Treaty-Based Return Positions

When a taxpayer takes a return position that is inconsistent with the standard US tax rules — for example, claiming a treaty exemption from US tax on certain income — Form 8833 (Treaty-Based Return Position Disclosure) must be attached to the US tax return. Failure to file Form 8833 when required can result in penalties of $1,000 per failure for individuals. Many foreign individuals are unaware that this form exists, and their treaty claims remain technically incomplete until it is filed.

Mistake 5: Ignoring State Tax Obligations

Federal tax treaties do not automatically apply to US state taxes. Most US states do not recognize federal income tax treaties and will tax your US-source income at full state rates, regardless of your treaty position at the federal level. For example, California — one of the most common destinations for foreign workers in the USA — does not honor any federal income tax treaties. This means a foreign individual working in California may successfully claim a 0% federal withholding rate under a treaty while still owing California state income tax at rates up to 13.3%.

How to Claim Tax Treaty Benefits in the USA: Step-by-Step

Claiming your treaty benefits correctly requires following a clear, documented process. Here are the seven steps every foreign individual should take to claim US tax treaty benefits in 2026.

Confirm Your Non-Resident Alien Status.

Before claiming any treaty benefit, verify that you are classified as a non-resident alien for US tax purposes. Apply the Green Card Test and the Substantial Presence Test. If you have already become a US tax resident, treaty benefits as an NRA generally no longer apply to you.

Verify Your Country Has a Treaty With the USA.

Check the IRS’s official list of US income tax treaties at IRS.gov to confirm your home country has an active treaty with the United States. Note the specific articles and rates that apply to your type of income, because each income category may have a different treaty rate.

Review the Specific Treaty Article for Your Income Type.

Obtain the full text of your country’s treaty with the United States from IRS.gov or the US Department of the Treasury. Identify the article that applies to your income — for example, dividends, interest, royalties, or employment income. Note the reduced withholding rate and any conditions (such as the 183-day rule for employment income).

Complete and Submit Form W-8BEN to Your US Payer.

Fill out IRS Form W-8BEN — Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding. In Part II (Claim of Tax Treaty Benefits), enter your country of residence, the treaty article number, and the reduced withholding rate you are claiming. Submit this form to your employer, financial institution, or other US withholding agent before the first payment is made.

File Form 8833 With Your US Tax Return If Required.

If your treaty position results in a reduced or zero US tax rate on income that would otherwise be taxable, attach Form 8833 (Treaty-Based Return Position Disclosure) to your US tax return. Describe the treaty, the applicable article, and the tax benefit you are claiming. Penalties of $1,000 per occurrence apply for non-disclosure.

File Form 1040-NR to Report US-Source Income.

Even if your treaty rate reduces your US tax to zero, you may still need to file Form 1040-NR to report your US-source income and formally assert your treaty position. The deadline is generally June 15 for non-resident aliens without US wages subject to withholding, or April 15 for those with such wages. Extensions are available.

Address State Tax Separately.

Research the tax treaty policy of the specific US state where you are working or earning income. Most states do not honor federal tax treaties. File the required state tax return and pay any state taxes owed, even if your federal treaty exemption eliminates federal liability.

How Tranzesta Helps Foreign Individuals Claim Tax Treaty Benefits in the USA

Navigating US tax treaty rules as a foreign individual is genuinely complex. One wrong form, one missed article, or one incorrect residency determination can cost you thousands of dollars in overpaid taxes — or trigger an IRS penalty notice. That is exactly why foreign nationals across the United States trust Tranzesta to handle their US tax obligations correctly.

Tranzesta is a US-based tax consultation firm with specialized expertise in non-resident alien tax compliance, international income sourcing, treaty benefit claims, and cross-border tax planning. Tranzesta.com Our team works with foreign workers, international students, content creators, and business owners earning US-source income from countries around the world.

Here is how Tranzesta can help you:

Determine your correct US tax residency status and confirm your eligibility for treaty benefits under your home country’s treaty with the USA

Identify the exact treaty article and reduced withholding rate that applies to each of your income streams

Prepare and file Form W-8BEN correctly so your US payer applies the right withholding rate from day one

Complete Form 8833 (Treaty-Based Return Position Disclosure) accurately and attach it to your US tax return

File Form 1040-NR to report your US-source income and formally claim your treaty position with the IRS

Advise you on state tax obligations in California, New York, Texas, Florida, and other US states where treaty recognition varies

Contact our team at hello@tranzesta.com for a free consultation. Visit Tranzesta.com to learn more about our international and non-resident alien tax services.

Tax Treaty Benefits for Foreign Individuals USA: Expert Tips for 2026

Beyond the basics, there are several advanced strategies that experienced international tax professionals use to maximize treaty benefits and minimize US tax exposure for foreign individuals. Here is what the Tranzesta team recommends for 2026.

Act before your first US payment.

Treaty benefits are not retroactive in most cases. If you wait until tax season to claim treaty benefits, your payer will have already withheld at 30%. You can recover overpaid taxes by filing Form 1040-NR and claiming a refund — but this takes months. Submit Form W-8BEN before your first payment to ensure the correct rate is applied immediately.

Monitor the 183-day rule carefully.

Many treaty articles covering employment income include a 183-day threshold. If you exceed 183 days of physical presence in the United States during a calendar year, your employment income may become fully taxable at US rates — even under a treaty. Track your US travel days precisely throughout the year.

Be aware of the Saving Clause.

Most US tax treaties include a Saving Clause that preserves the US’s right to tax its own citizens and residents as if the treaty did not exist. If you become a US resident for tax purposes while holding a treaty-country passport, the Saving Clause generally eliminates most of your treaty benefits. The major exception is for certain items specifically carved out in the treaty itself.

Consider the impact of treaty benefits on Social Security.

Some tax treaties affect the taxability of US Social Security benefits paid to foreign individuals. For example, residents of Canada, Germany, and the UK benefit from specific provisions that reduce or eliminate US withholding on US Social Security payments. This is a frequently overlooked benefit with significant long-term value.

Review your treaty position annually.

Tax treaties are renegotiated, amended, and occasionally terminated by either country. The US Treasury publishes updates at Treasury.gov. Review your treaty position each year to ensure the benefits you are claiming are still available and have not been modified.

The tax experts at Tranzesta stay current with every US tax treaty update, IRS Revenue Procedure, and regulatory change that affects foreign individuals working in the United States. We provide clear, actionable guidance — in plain English — so you can focus on your work rather than tax compliance.

Conclusion

Tax treaty benefits for foreign individuals in the USA represent one of the most powerful — and most underutilized — tools available to non-resident aliens earning income inside the United States. Here are the three most important takeaways from this guide:

The US imposes a 30% withholding tax on US-source

income paid to non-resident aliens by default. Tax treaties with over 65 countries reduce this rate significantly — often to 0% on interest and certain royalties — but you must proactively claim the benefit using Form W-8BEN.

Treaty benefits depend on your tax residency status,

not your visa or passport. Getting this classification right is the foundation of every treaty claim — and getting it wrong can result in overpaid taxes, penalties, or an IRS audit.

Federal treaty benefits do not automatically extend to US

state taxes. Most states — including California — tax foreign individuals at full state rates regardless of any federal treaty position.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

To claim tax treaty benefits in the USA as a foreign worker, you must first confirm that your home country has an active income tax treaty with the United States. Next, determine that you qualify as a non-resident alien for US tax purposes.

The tax treaty withholding rate for dividends in the USA varies by treaty country. Without a treaty, the standard IRS withholding rate on dividends paid to non-resident aliens is 30%.

Yes, in many cases you still need to file a US tax return even if your income is fully covered by a tax treaty and your US tax liability is zero. Non-resident aliens with US-source income generally must file Form 1040-NR. Additionally, if you are taking a treaty-based tax position that overrides standard US tax rules.

Many countries do not have an income tax treaty with the United States, meaning their residents face the full 30% US withholding tax on most US-source passive income. As of 2026, notable countries without a US tax treaty include Brazil, Argentina, Saudi Arabia, the United Arab Emirates, most African nations, and many Latin American countries.

Yes, many US tax treaties include specific exemptions for foreign students, researchers, and trainees studying in the United States. For example, the US-India tax treaty provides a limited exemption for Indian students on certain scholarships and stipends.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation