Cannabis 280E Deep Dive: Maximizing Cost of Goods Sold

Cannabis businesses in the United States pay some of the highest effective federal tax rates of any industry — sometimes exceeding 70%. That staggering number is largely the result of Internal Revenue Code Section 280E, which bars cannabis companies from deducting ordinary business expenses. However, one powerful and fully legal strategy can soften the blow significantly: learning how to cannabis 280E maximize cost of goods sold (COGS). When you correctly identify and allocate every allowable cost into COGS, you reduce your taxable income without violating federal law.

In this guide, you will learn exactly what Section 280E says,

which costs qualify as COGS under IRS rules, the most common mistakes cannabis operators make, and a step-by-step process to build a COGS strategy that survives an audit. Whether you run a cultivator, a processor, or a retail dispensary anywhere in the USA, this article gives you the framework you need.

What Is IRC Section 280E and Why Does It Crush Cannabis Businesses?

Section 280E of the Internal Revenue Code is a federal tax provision that disallows all ordinary and necessary business expense deductions for any trade or business that “consists of trafficking in controlled substances.” Because marijuana remains a Schedule I controlled substance under the Controlled Substances Act, cannabis businesses cannot deduct rent, salaries, utilities, marketing, or most other operating costs — even when those businesses operate legally under state law.

The Origin of 280E

Congress passed Section 280E in 1982 in direct response to a Tax Court ruling that allowed a drug dealer to deduct business expenses. Lawmakers wanted to punish illegal drug traffickers. Decades later, however, the law now lands squarely on licensed, regulated cannabis companies across the United States.

The IRS has consistently applied 280E to state-legal cannabis businesses, and multiple Tax Court cases — including Harborside Health Center v. Commissioner — have confirmed this position. In short: federal law does not care that your dispensary has a state license.

The Only Lifeline: Cost of Goods Sold

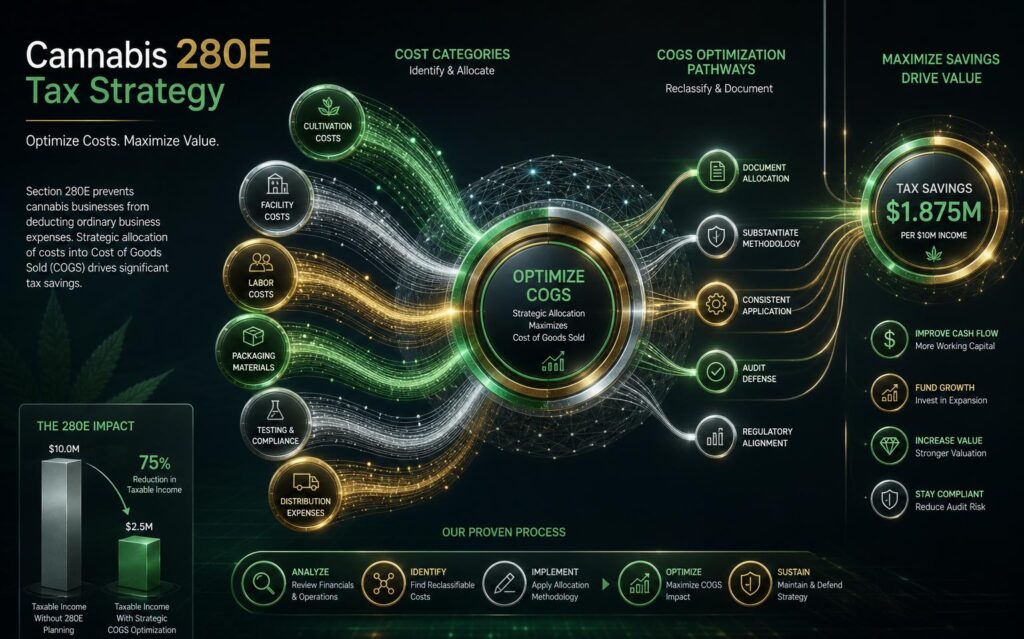

Here is the critical exception. Section 280E blocks expense deductions, but it does not block the reduction of gross receipts by the cost of goods sold. This distinction exists because COGS is not technically a “deduction” — it is an adjustment to gross income under IRC Section 471 and the uniform capitalization rules of Section 263A. Therefore, cannabis operators must build every legally supportable cost into COGS to reduce taxable income. This is why the strategy to cannabis 280E maximize cost of goods sold is the single most important tax planning tool available to the industry.

How Does Cannabis 280E Maximize Cost of Goods Sold Under IRS Rules?

To cannabis 280E maximize cost of goods sold lawfully, you must understand what the IRS allows under IRC Sections 471 and 263A. These sections define how businesses — including cannabis producers and retailers — must value their inventory and which costs get capitalized into COGS.

COGS for Cannabis Producers and Cultivators

Cannabis cultivators and manufacturers are treated similarly to any other producer under the tax code. They must use inventory accounting and can capitalize a wide range of production costs into COGS. Allowable COGS components for producers include:

Direct materials: seeds, clones, growing media, nutrients, pesticides, packaging

Direct labor: wages and payroll taxes for employees directly involved in growing, harvesting, trimming, and processing

Overhead: utilities (electricity, water, HVAC) directly used in the grow facility

Depreciation on production equipment and the productive portion of real property

Testing and compliance costs tied to production

Quality control expenses incurred before the product is ready for sale

Additionally, under Section 263A (the Uniform Capitalization rules, or UNICAP), larger producers must also include indirect production costs — such as a portion of administrative salaries that relate to the production function — into COGS. This rule actually helps cannabis businesses by allowing even more cost capitalization.

COGS for Cannabis Retailers and Dispensaries

Retail dispensaries that purchase finished product — rather than cultivate or manufacture it — have a narrower COGS. However, they can still include the purchase price of inventory, freight and shipping costs to acquire inventory, and direct costs of receiving and preparing products for sale. Dispensaries should work with a qualified accountant to document these costs meticulously so they can withstand IRS scrutiny.

It is important to note that purely selling expenses

such as advertising, budtender wages for customer-facing work, or delivery driver pay for completed sales — generally cannot be included in COGS for retailers. The IRS distinguishes between costs incurred to produce or acquire inventory versus costs incurred to sell it.

External reference: See IRS Publication 334 and the relevant guidance on inventory accounting for the foundational rules on COGS.

Common 280E Mistakes That Cost Cannabis Businesses Thousands

Even well-intentioned cannabis operators leave significant money on the table — or worse, create audit exposure — by misapplying the COGS rules. Therefore, understanding these mistakes is just as important as knowing the correct strategy.

Mistake 1: Treating All Payroll as Non-Deductible

Many cannabis business owners assume that because 280E blocks wage deductions, none of their payroll costs are recoverable. That is simply wrong. Wages paid to employees who perform production activities — growers, trimmers, extraction technicians, packaging staff — are fully capitalized into COGS. Only wages for purely selling, marketing, or administrative roles fall outside of COGS for retailers.

Mistake 2: Ignoring Section 263A for Larger Operations

Producers with average annual gross receipts above $27 million (the 2023 threshold under the Tax Cuts and Jobs Act) are required to apply UNICAP rules, but even smaller businesses can benefit from voluntarily capitalizing additional indirect costs. Ignoring 263A entirely is a missed opportunity that directly raises your federal tax bill.

Mistake 3: Poor Recordkeeping and Job Costing

The IRS will not simply accept your COGS figure — it expects detailed records. Without a proper job costing system that tracks labor hours by activity, utility bills allocated by square footage, and depreciation schedules tied to specific equipment, your COGS claims are vulnerable. Inadequate documentation is the leading cause of disallowed COGS in cannabis audits across the United States.

Mistake 4: Misclassifying Overhead Costs

Overhead costs such as rent and utilities can be included in COGS for the portions of a facility used in production — but not for retail floor space. If 60% of your facility is the grow room and 40% is the sales floor, only 60% of facility overhead belongs in COGS. Applying the wrong allocation percentage is both a compliance error and a missed opportunity if you under-allocate production space.

Mistake 5: Failing to Separate Business Activities

The Californians Helping to Alleviate Medical Problems (CHAMP) case established that a cannabis business with multiple separate and distinct business activities — one subject to 280E and one not — can deduct expenses attributable to the non-cannabis activity. However, the activities must be genuinely separate, with independent revenue and distinct accounting. Artificially lumping together activities to create a tax shelter will fail under IRS scrutiny.

Step-by-Step Guide to Cannabis 280E Maximize Cost of Goods Sold

Follow these seven steps to build a legally defensible, maximized COGS strategy for your cannabis business. Each step builds on the previous one, so work through them in order.

Classify your business type accurately.

Determine whether your business is a cultivator, processor, retailer, or a combination. Your entity type determines which COGS rules apply. Vertically integrated operations have the broadest COGS opportunity but also the most complex accounting requirements.

Map every cost center in your operation.

List all expenses — payroll, rent, utilities, supplies, depreciation, insurance, testing, and professional fees. Do not assume any cost is automatically excluded from COGS without analysis. This exercise often reveals overlooked capitalizable costs.

Identify production versus selling activities.

For each payroll category and each overhead expense, determine what percentage relates to production (capitalizable into COGS) versus selling or administrative activities (blocked by 280E). Use time studies, floor plans, and production logs to support your allocations.

Implement a job costing or inventory costing system.

Use accounting software — ideally one designed for cannabis operations or a robust general ledger with cannabis modules — to track costs at the batch or lot level. Systems like QuickBooks with proper configuration, or cannabis-specific platforms, allow you to capture COGS in real time rather than reconstructing it at year-end.

Apply Section 263A if applicable.

If your cannabis business is a producer, evaluate whether UNICAP rules apply and which indirect costs — including a portion of administrative overhead tied to production — must or can be capitalized. Work with a qualified cannabis tax professional to run the UNICAP calculation correctly.

Document everything with IRS-ready detail.

Keep time records, floor space calculations, utility breakdowns, equipment depreciation schedules, purchase invoices, and any other documentation that supports each line of your COGS. The IRS can audit up to three years back — or longer if fraud is alleged.

How Tranzesta Helps Cannabis Businesses Maximize COGS and Cut Their Tax Bill

Navigating Section 280E requires specialized knowledge that goes far beyond standard business accounting. Tranzesta is a US-based tax consultation firm with deep expertise in cannabis industry accounting and IRS compliance. Our team understands the nuances of COGS optimization, UNICAP calculations, entity structuring, and audit defense — specifically for cannabis operators across the United States.

When you work with Tranzesta, we start with a comprehensive cost analysis to identify every capitalizable expense you may be missing. We then help you implement the right accounting systems and processes so that your COGS is accurate, maximized, and fully documented throughout the year — not just at tax time.

Our cannabis accounting services include COGS strategy and implementation, full-year bookkeeping designed around 280E compliance, federal and state tax preparation, IRS representation and audit support, and entity structure review. We serve cultivators, processors, dispensaries, and vertically integrated cannabis companies across the USA.

Ready to stop overpaying federal taxes? Contact our team at hello@tranzesta.com for a free consultation. Learn more about our cannabis accounting services at Tranzesta.com.

Cannabis 280E Maximize Cost of Goods Sold: Expert Tips for 2026

As the cannabis industry evolves and IRS scrutiny increases, staying ahead of the curve is essential. Tranzesta’s cannabis tax experts share these advanced strategies to help your business minimize its 280E burden in 2026 and beyond.

Consider a vertically integrated structure. Businesses that cultivate, process, and retail their own product have the broadest COGS base. However, ensure your entity structure and accounting properly separates each activity to capture the maximum allowable costs at each stage.

Review your depreciation method.

Under the Modified Accelerated Cost Recovery System (MACRS), cannabis production equipment can be depreciated rapidly. Accelerated depreciation flows directly into COGS for producers and meaningfully reduces taxable income in the early years of equipment ownership.

Track labor with precision.

Use time-tracking software to log employee hours by activity category. A single employee who splits time between trimming (production) and stocking shelves (selling) should have documented time allocations — not estimates — to support your COGS treatment.

Stay current on rescheduling developments.

Federal cannabis rescheduling proposals continue to advance in the United States. If cannabis is moved to Schedule III, Section 280E may no longer apply. However, until rescheduling is finalized and legally effective, operate as though 280E remains fully in force.

Build COGS review into your monthly close.

The most successful cannabis businesses treat COGS optimization as an ongoing process, not an annual scramble. Monthly reconciliation catches issues early and keeps your financial picture accurate.

For personalized guidance on your specific COGS strategy,

visit Tranzesta.com to learn more about our cannabis tax and bookkeeping services.

Conclusion: Your 280E COGS Strategy Starts Today

Section 280E is one of the most punishing provisions in the US tax code for any legitimate industry. However, it is not without a strategy. The key takeaways from this guide are: first, COGS is your most powerful — and legal — tool to reduce taxable income under 280E. Second, both producers and retailers have meaningful COGS opportunities, but they require precise allocation, documentation, and accounting systems to survive IRS scrutiny. Third, mistakes in classification, recordkeeping, or overhead allocation can cost your cannabis business tens of thousands of dollars annually.

The cannabis businesses that thrive financially

are those that treat tax strategy as a year-round priority, not an afterthought. Working with a specialist who understands the interplay between IRC Sections 280E, 471, and 263A can make the difference between a crippling tax bill and a manageable one.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

Yes. Section 280E applies to any business that traffics in a federally controlled substance, regardless of whether that business holds a valid state cannabis license. The IRS and US Tax Court have consistently ruled that state-legal cannabis companies must comply with 280E. Because marijuana remains a Schedule I substance under federal law, businesses in legal states like California, Colorado, Michigan, and others are all subject to the same federal restrictions on expense deductions.

Under Section 280E, ordinary business expense deductions — such as rent, salaries, and marketing — are completely disallowed for cannabis businesses. However, cost of goods sold (COGS) is not a deduction in the traditional sense. Instead, it is an adjustment that reduces gross receipts to arrive at gross income under IRC Section 471. Because 280E only blocks deductions and not this adjustment, cannabis operators can legally reduce their taxable income by maximizing the costs properly classified as COGS.

Generally, no — not for a pure retail dispensary. Budtender wages are typically a selling expense because budtenders serve customers on the retail floor, not in production. However, if a budtender also performs inventory receiving, quality checks, or product preparation activities, a defensible portion of their wages may be allocated to COGS. Time records are essential to support any mixed-activity allocation. For vertically integrated businesses that cultivate or process their own product, the analysis is more nuanced.

Federal rescheduling of cannabis to Schedule III would likely eliminate the application of Section 280E to cannabis businesses, because 280E only applies to Schedule I and II substances. However, as of 2026, rescheduling has not been finalized or legally enacted. Until a final rule takes effect, cannabis businesses in the United States must continue to operate under 280E and should not change their tax strategies based on anticipated — but not yet enacted — law changes.

Section 263A requires certain producers to capitalize indirect costs — such as administrative expenses, storage costs, and purchasing costs — into inventory. For cannabis businesses, this rule is actually beneficial: it allows producers to include a broader range of costs in COGS, thereby reducing taxable income. Larger cannabis producers with gross receipts above the small business threshold must apply UNICAP. Smaller producers may elect to use simplified inventory methods. Either way, understanding 263A is essential for any cannabis cultivator or manufacturer in the USA trying to minimize their 280E tax burden.

One Response