If you operate a cannabis business in the United States,

you already know the rules feel like they were written in two different languages. State regulators want every plant logged, every transfer scanned, and every sale tied back to a unique tag. The IRS, on the other hand, refuses to acknowledge that you are even allowed to deduct the same expenses any other small business takes for granted. Sitting in the middle of that contradiction is seed to sale tracking tax compliance — the discipline of making your inventory, your accounting, and your federal tax return tell exactly the same story.

This guide is written for owners, CFOs, and bookkeepers

who want to stop guessing. We’ll walk through how seed-to-sale tracking actually works, why it matters for IRS Section 280E exposure, the most common compliance mistakes sees in audits, and a step-by-step framework you can apply this quarter. By the end, you’ll know exactly what your books, your METRC ledger, and your tax filings need to look like to survive a Department of Revenue review or an IRS field audit.

What Is Seed-to-Sale Tracking and Why Does It Matter for Tax Compliance?

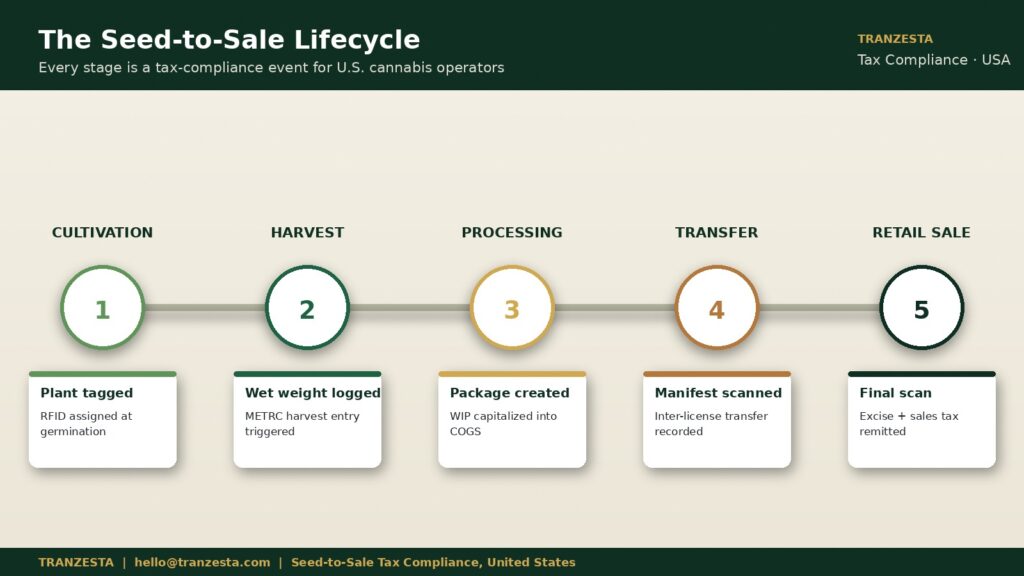

Diagram showing the seed to sale tracking lifecycle from cultivation to dispensary sale

Seed-to-sale tracking is the regulatory requirement that every legal cannabis plant be assigned a unique identifier from the moment it germinates until it leaves a licensed retailer in a sealed package. In the United States, that tracking lives inside platforms like METRC (opens in new tab), BioTrack, or state-built equivalents in Washington, Oregon, and a handful of others. Every plant is tagged, every harvest is weighed, every transfer between licensees is scanned, and every retail sale is reconciled at the end of each business day.

The “tax compliance” half of seed to sale tracking tax compliance is what most operators underestimate. Because cannabis is still a Schedule I controlled substance under federal law, the Internal Revenue Service applies Section 280E (opens in new tab), which disallows ordinary business deductions for any operation “trafficking” in a controlled substance. The single legal escape valve is Cost of Goods Sold (COGS) — and your ability to claim COGS depends entirely on the accuracy of your seed-to-sale data. If your METRC ledger says you produced 500 pounds of trim but your books only show 420 pounds capitalized into inventory, the IRS has a clean line of attack during examination.

Put another way: your state tracking system

is the source of truth your tax position rests on. Tranzesta builds the bridge between the two so the numbers match before a regulator ever asks.

The 2026 Regulatory Landscape: What’s Actually Required in the United States

The United States does not have a single federal cannabis program, so requirements vary by license type and state. Across the 38 states with some form of legal cannabis, four pillars of compliance now apply universally:

1. State-mandated track-and-trace.

Every licensed plant must carry a unique RFID or barcode tag from cultivation through retail sale (opens in new tab). California, Colorado, Michigan, and most other adult-use states use METRC. Washington uses Leaf Data Systems. Oregon uses METRC as of 2024. Whatever the platform, daily reconciliation between physical inventory and the digital ledger is non-negotiable.

2. Federal tax filing under Section 280E.

Cannabis businesses must still file federal returns — Form 1120 for C-corps, 1065 for partnerships, 1040 Schedule C for sole proprietors. The catch: only COGS is deductible. Selling, general, and administrative expenses (SG&A) like marketing, executive salaries, and rent for retail floor space cannot reduce taxable income.

3. State excise and sales tax. Most adult-use states

layer a cannabis excise tax (often 10–37%) on top of standard sales tax, and those liabilities are reported monthly. Mismatches between point-of-sale data, METRC sales records, and tax remittance are the #1 trigger for state Department of Revenue audits.

4. Banking and cash-handling documentation.

Because most banks still refuse cannabis deposits, the majority of U.S. operators handle large amounts of cash. The IRS expects a Form 8300 filing for every cash receipt over $10,000 from a single payer, and the Bank Secrecy Act requires meticulous logs.

The Tranzesta cannabis tax compliance team monitors all four pillars across every U.S. jurisdiction we serve so our clients don’t have to track regulatory updates themselves.

Why Section 280E Makes Seed-to-Sale Data So Valuable

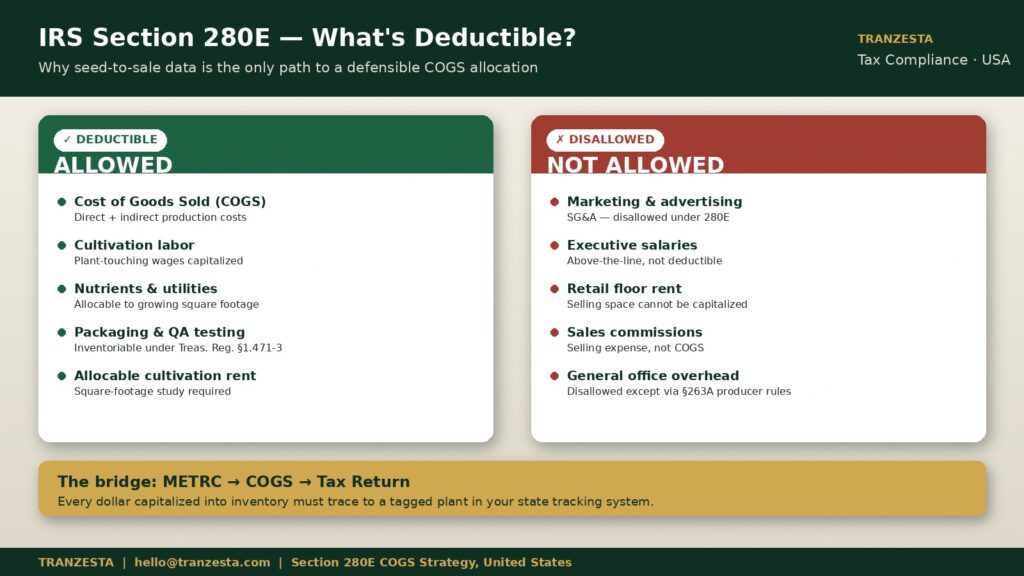

Visual breakdown of IRS Section 280E and how COGS allocations protect cannabis operators

Section 280E is the single biggest reason seed to sale tracking tax compliance matters more in cannabis than in any other industry. A typical small business pays federal tax on net income — revenue minus all reasonable expenses. A cannabis business pays federal tax on gross profit, because almost no expense below the COGS line is allowed.

That means the line between “cost of producing the product” and “cost

of running the business” is the most expensive line on your P&L. Get it right and your effective federal tax rate sits in a workable range. Get it wrong and you can end up paying 70%+ of net income to the IRS. The Tax Court case Patients Mutual Assistance Collective Corp. (Harborside) v. Commissioner (opens in new tab) made this painfully clear: vertically integrated retailers cannot use IRC §263A to push more SG&A into inventory the way producers can.

where seed-to-sale data becomes your most valuable asset.

Every harvest event in METRC is a journal entry waiting to happen. Every package transfer is a movement from one inventory account to another. Every retail sale is a deduction of inventory at standard cost. When your accounting system mirrors your METRC ledger plant-by-plant, your COGS calculation is automatically defensible — every dollar of deduction maps back to a tagged unit of physical inventory the state can verify.

Step-by-Step: How to Build an Audit-Ready Seed-to-Sale Tax Workflow

The framework below is the same one Tranzesta deploys with new cultivation and dispensary clients across the United States. Work through each step in order — most operators can implement the full workflow in 60–90 days.

Step 1 — Map your license type to the correct COGS method.

Cultivators, manufacturers, and retailers each have different “absorption” rules. Cultivators get the broadest COGS treatment under Treas. Reg. §1.471-3 (opens in new tab) because they grow the product; retailers get the narrowest. Mixing methods or copying a friend’s chart of accounts is the single fastest way to lose a Section 280E argument.

Step 2 — Set up a chart of accounts that mirrors METRC categories.

Build inventory sub-accounts for Immature Plants, Vegetative Plants, Flowering Plants, Harvest Batches, Processing WIP, Finished Goods, and Sold Inventory. Each of these maps to a stage in your state tracking system. When METRC moves a plant, your accounting moves a dollar.

Step 3 — Reconcile daily, not monthly.

Pull your METRC sales report at end-of-day and tie it to your point-of-sale Z-tape and your bank deposit (or cash count). A single day of mismatch is easy to fix. A 90-day mismatch is a forensic accounting project.

Step 4 — Capitalize the right costs into inventory.

Direct labor, cultivation utilities, nutrients, packaging, and quality testing all belong in COGS. So do allocable overhead items like the rent for cultivation square footage. Tranzesta runs a square-footage and time-allocation study for every client so the percentages we capitalize would survive challenge.

Step 5 — File Form 8300 the day you breach $10,000 in cash.

Not the week of, the day of. The penalties for late filing are punitive and the IRS has been actively prosecuting cannabis operators on this exact issue.

Step 6 — Run a quarterly mock audit.

Pretend the IRS just sent you an Information Document Request. Can you produce a complete METRC-to-GL-to-tax-return chain for any randomly selected month? If not, that’s the gap to close before quarter-end.

Step 7 — Document your tax positions in writing.

Every COGS allocation method, every overhead percentage, every state apportionment formula needs a written memo signed by an officer. The memo is what protects you years later when a different examiner shows up.

The Top 6 Seed-to-Sale Tax Mistakes (and How to Fix Them)

Top seed to sale tracking tax compliance mistakes ranked for U.S.

In Tranzesta’s audit-defense engagements across the United States, six errors come up over and over again:

1. Treating METRC as a regulatory chore instead of an accounting source.

Operators give bookkeepers read-only access to METRC and never reconcile. Result: state tracking and GL drift apart and the inventory number on the tax return is indefensible.

2. Capitalizing too little (or too much) into COGS.

Under-capitalize and you lose deductions. Over-capitalize and the IRS will reverse you under the Uniform Capitalization rules (opens in new tab). Both errors are common; both are expensive.

3. Forgetting to amend after a METRC adjustment.

A plant destruction, a sample correction, or a shrinkage entry in METRC needs a corresponding journal entry the same day. We’ve seen $200,000 inventory adjustments sit unrecorded for an entire fiscal year.

4. Mixing 280E and non-280E activities without a clean cost study.

Many vertically integrated operators run an ancillary, non-plant-touching activity (apparel, accessories, education) that is fully deductible. The IRS will only honor that separation if you have documented allocation drivers.

5. Ignoring state apportionment rules.

Operators with multiple state licenses often forget that California sourcing, Colorado throwback, and Massachusetts single-sales-factor formulas all apply differently to cannabis revenue.

6. Treating Form 8300 as optional.

It is not optional, and the IRS Cannabis Industry compliance program has made this a top enforcement priority for 2026.

Tranzesta’s compliance team has built playbooks for each of these. If any of the six sound familiar, that’s the conversation to have with us this quarter.

METRC vs. BioTrack vs. State Systems: A Quick Comparison

The choice is rarely up to you — your state mandates one system. What matters is how cleanly you integrate it with your accounting stack. Tranzesta has integration patterns for all three.

How Tranzesta Helps U.S. Cannabis Operators Stay Compliant

Tranzesta is a United States–based tax consulting firm that has worked with cultivators, manufacturers, and licensed retailers in every major adult-use state since the legal market matured. We focus exclusively on regulated industries where the tax rules are non-standard, and cannabis is one of our largest practice areas.

For seed-to-sale tax compliance work, our clients get a single team that handles the METRC reconciliation, the COGS capitalization study, the Section 280E memo, the state excise and sales tax filings, and the Form 8300 cash-reporting workflow. We also provide audit defense if the IRS or your state Department of Revenue knocks on the door — and because our team built the books in the first place, we can produce the documents the examiner asks for the same day.

If you want to see what a clean seed to sale tracking tax compliance workflow looks like in your business, contact the Tranzesta team or email hello@tranzesta.com. The first conversation is free and we’ll give you a written punch list of what’s working, what’s missing, and what to fix first.

Conclusion

Cannabis operators don’t get to choose whether the rules are fair — they only get to choose whether they’re prepared. Seed to sale tracking tax compliance is the discipline that makes preparation possible: every plant tagged, every gram accounted for, every dollar capitalized into the right account, every tax position documented in writing. Done well, it turns Section 280E from an existential threat into a manageable line item. Done poorly, it ends licenses and businesses.

The Tranzesta team is built for this. If you’re ready to align your inventory, your books, and your federal return into a single defensible system, get in touch at hello@tranzesta.com.

FAQs

It means your state tracking ledger (usually METRC), your point-of-sale system, your accounting books, and your federal and state tax returns all reflect the same physical inventory at the same moment in time. Every gram on a shelf must trace back to a tagged plant in METRC and forward to a recognized sale in your books and tax filings.

Generally, no — IRS Section 280E disallows ordinary deductions for businesses trafficking in Schedule I controlled substances. The legal exception is Cost of Goods Sold, which lets cultivators and manufacturers capitalize a meaningful portion of labor and overhead. Retailers face the strictest treatment. Tranzesta runs a license-specific COGS study for every client to maximize what is legally deductible.

Daily. Weekly is acceptable in low-volume cultivations during off-season, but daily reconciliation is the standard for retail and any operation with significant transfer activity. Monthly reconciliation is how operators end up unable to defend an audit.

The most common triggers are inconsistent gross-margin reporting year over year, large cash deposits without matching Form 8300 filings, COGS allocations that look unusually high for the license type, and tip-offs from state Department of Revenue audits. The IRS Cannabis Industry program is actively targeting these patterns through 2026.

Yes. Tranzesta works with multi-state operators across the United States and handles the apportionment, intercompany transfer pricing, and state-by-state filing calendar that come with operating in more than one license jurisdiction.

2 Responses