Cannabis business structure tax minimize 2026 in US

Most US cannabis operators pay an effective federal tax rate above 50%. The reason is simple. IRS Section 280E disallows nearly every ordinary business deduction. Therefore, is no longer optional — it is survival. Choosing the wrong entity, mixing taxable activities, or skipping a multi-entity plan can cost your business hundreds of thousands of dollars each year.

In this guide, you will learn exactly how to structure a US cannabis business to legally reduce tax burden. We cover entity selection, multi-entity strategies, COGS optimization, common structural mistakes, and a step-by-step framework you can apply this quarter. Tranzesta has built this playbook through years of audit-defense work across the United States. Let’s begin.

What Does “Cannabis Business Structure Tax Minimize” Actually Mean?

A cannabis business structure tax minimize plan is the legal framework you use to reduce federal and state taxes inside the constraints of IRS Section 280E. In short, it is the combination of entity type, ownership structure, and intercompany agreements that keeps as much money in the business as legally possible.

For US cannabis operators, structure matters more than for almost any other industry. Because Section 280E disallows ordinary deductions for businesses “trafficking” in a Schedule I controlled substance, only Cost of Goods Sold (COGS) is deductible. As a result, every dollar must be channeled through an entity that captures it as COGS — not as overhead.

Tranzesta works with cultivators, processors, and dispensaries

across the United States. Our team designs structures that hold up under IRS audit and state Department of Revenue review. Most importantly, we build them to scale.

Why Structure Beats Every Other Tax Strategy

Most tax savings in cannabis come from how the business is organized. For example, a single-entity dispensary cannot deduct rent on retail floor space. However, a properly designed two-entity structure can shift expenses into a deductible management company. Therefore, structure decisions made on day one drive returns for the next decade.

Who Needs This Plan?

Every licensed US cannabis operator needs one. Whether you run a small Oregon craft farm or a multi-state operator (MSO), the rules apply. Furthermore, both LLCs and corporations face Section 280E exposure equally — so the entity decision is only the starting point.

Cannabis Business Structure Tax Minimize: Key Rules and Requirements

The rules for a defensible cannabis business structure tax minimize plan come from three places: the Internal Revenue Code, US Tax Court precedent, and your state’s cannabis regulations. Understanding all three is the foundation for any structure that survives an audit.

First, IRC Section 280E disallows deductions for any business trafficking in Schedule I or II controlled substances. Cannabis remains Schedule I as of April 2026. Therefore, the only legal escape valve is the COGS exclusion under IRC Section 471 (opens in new tab). Second, the IRS Marijuana Industry guidance (opens in new tab) confirms that operators must still file federal returns and pay tax on gross profit, not net income. Third, every US state with legal cannabis layers its own excise tax, sales tax, and licensing rules.

Here are the six most important compliance requirements every structure must meet:

Separate plant-touching from non-plant-touching activities with documented intercompany agreements.

Capitalize qualifying costs into inventory under Treas. Reg. §1.471-3.

File Form 8300 for every cash receipt over $10,000.

Maintain audit-ready books that match METRC or your state tracking system daily.

Document all related-party transactions at arm’s-length prices.

File state-specific returns in every jurisdiction where you operate.

How Section 280E Drives Every Decision

Section 280E is the single biggest reason structure matters. For instance, a vertically integrated dispensary that earns $5 million in revenue and has $3 million in operating expenses might owe federal tax on $4 million instead of $2 million. As a result, the right structure can cut tax liability nearly in half.

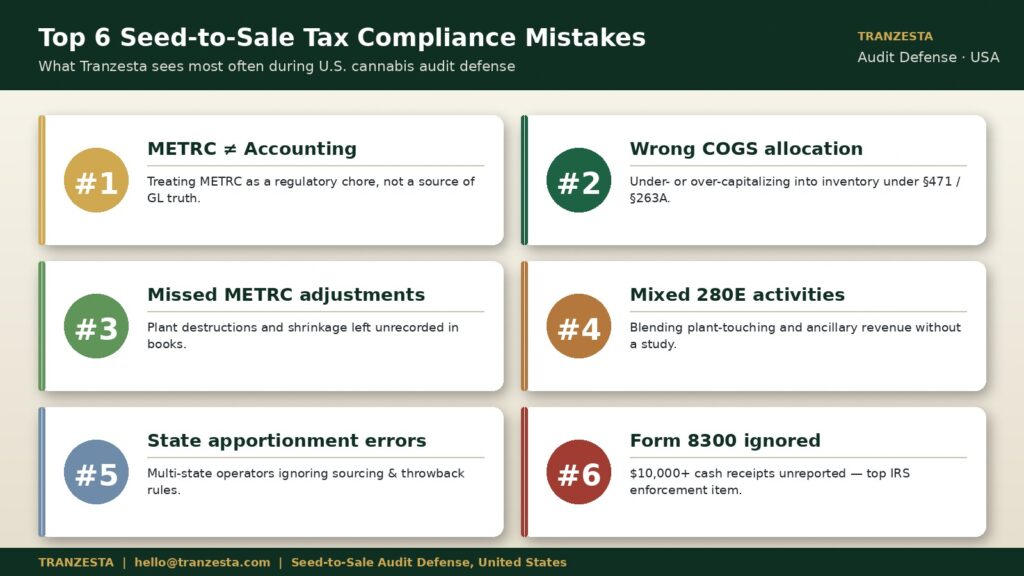

Common Mistakes That Increase Cannabis Tax Burden

Most cannabis operators in the United States make at least one of these structural mistakes. Each one is preventable. However, fixing them after the fact costs ten times more than building the structure correctly the first time.

Mistake 1: Running Everything Through One Entity

Single-entity cannabis businesses lose every dollar of SG&A as a non-deductible expense. For example, a single-LLC dispensary cannot deduct executive salaries, retail floor rent, or marketing. By contrast, splitting the business into a plant-touching OpCo and a non-plant-touching management company can move some expenses outside Section 280E. This single change has saved Tranzesta clients between $80,000 and $400,000 per year.

Mistake 2: Choosing C-Corp Without a Strategy

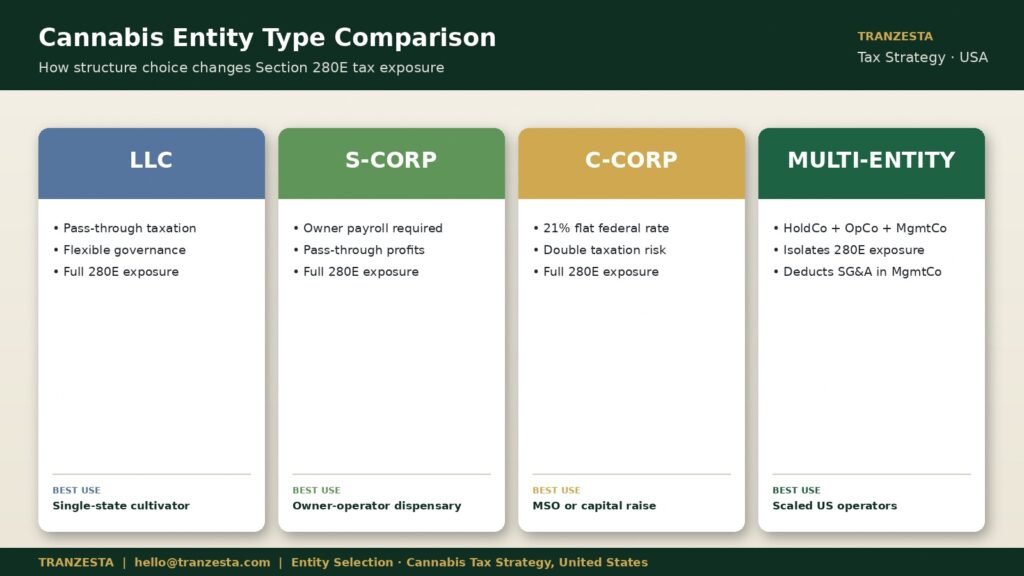

Many operators default to a C-Corp because the 21% federal rate sounds attractive. However, C-Corps still face Section 280E. Worse, they create double taxation when profits are distributed. As a result, a C-Corp only makes sense if you are raising institutional capital or planning a public listing. Otherwise, an LLC structure is usually more flexible.

Mistake 3: Ignoring Related-Party Documentation

When you operate two related entities, every transaction between them must be priced at arm’s length. The IRS will reverse intercompany charges that look artificial. Furthermore, weak documentation invites both federal and state audit adjustments. Therefore, written management agreements, lease agreements, and transfer pricing memos are non-negotiable.

Step-by-Step: How to Structure Your US Cannabis Business to Minimize Tax

Follow this seven-step framework to build a defensible cannabis business structure tax minimize plan. Most operators can implement the full structure in 60 to 120 days. Tranzesta uses this exact framework with new US clients.

Step 1 — Map your business activities.

List every revenue stream, cost center, and asset. For example, separate cultivation, manufacturing, distribution, and retail. Then identify which activities touch the plant and which do not. This map drives every entity decision that follows.

Step 2 — Choose the right base entity for each activity.

For most US operators, an LLC taxed as a partnership is the strongest starting point. However, single-owner dispensaries often benefit from an S-Corp election. C-Corps make sense only for capital-raising plans or MSOs.

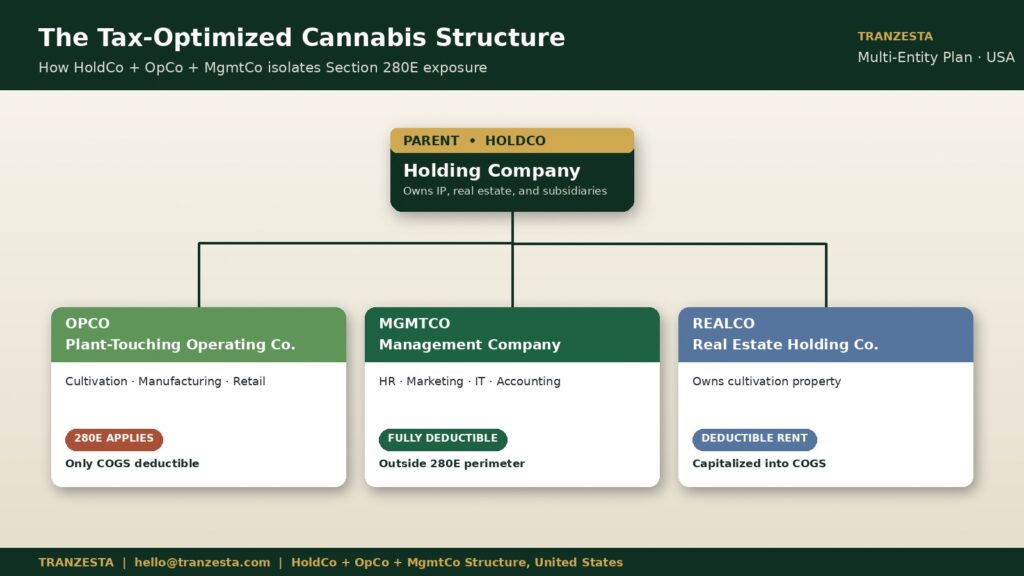

Step 3 — Set up a holding company (HoldCo).

A HoldCo owns the operating entities and any cannabis intellectual property. This isolates risk and creates a clean structure for future investors. Additionally, the HoldCo can hold real estate or trademarks outside the 280E perimeter.

Step 4 — Create a non-plant-touching management company (MgmtCo).

This entity provides services like HR, marketing, accounting, and IT to the OpCo. As a result, those expenses become deductible to MgmtCo. The OpCo pays MgmtCo a documented arm’s-length management fee.

Step 5 — Capitalize the right costs into COGS.

Direct labor, nutrients, packaging, and allocable cultivation utilities all belong in COGS. Tranzesta runs a square-footage and time-allocation study for every client so capitalized percentages survive IRS challenge.

Step 6 — Lock in state apportionment and licensing alignment.

If you operate in multiple US states, ensure your structure matches each state’s residency, ownership, and apportionment rules. For instance, California, Colorado, and Massachusetts each apply different sourcing formulas.

Step 7 — Document everything in writing.

Every entity, every intercompany agreement, every COGS allocation method needs a signed memo. This is what protects you years later when an IRS examiner appears.

How Tranzesta Helps US Operators Minimize Cannabis Tax Burden

Tranzesta is a United States–based tax consultation firm built for industries with non-standard tax rules. Cannabis is one of our largest practice areas. Our team has helped operators in California, Colorado, Michigan, New Jersey, and a dozen other US states design structures that legally cut tax exposure.

For cannabis business structure tax minimize engagements, Tranzesta delivers a single-team solution. We review your current entity setup, identify Section 280E leakage, and design a HoldCo-OpCo-MgmtCo structure that fits your license type and growth plan. Additionally, we draft the intercompany agreements, build the chart of accounts, and run the COGS capitalization study.

Tranzesta also handles ongoing bookkeeping, federal and state filings, Form 8300 compliance, and full audit defense. Because our team designs the structure and maintains the books, we can produce any document an examiner asks for the same day.

Visit Tranzesta.com to learn more about our cannabis tax services or contact our team at hello@tranzesta.com for a free consultation. We will give you a written punch list of what is working, what is missing, and what to fix first.

Cannabis Business Structure Tax Minimize: Expert Tips for 2026

Pro-level structures share a handful of advanced moves. Most US operators miss them. However, applied together they can lower your effective tax rate by another 5 to 12 percentage points.

Use real-estate segregation. Hold cultivation property in a separate LLC and lease it to the OpCo. Rent paid by the OpCo is partially capitalized into COGS.

Run a quarterly 280E exposure model.

Update gross profit, COGS allocations, and management fees every quarter so surprises never appear at year-end.

Adopt accrual accounting from day one. Cash-basis books rarely survive an IRS cannabis audit at scale.

File Form 8300 the same day any cash receipt crosses $10,000. The IRS Cannabis Industry program is actively prosecuting late filings in 2026.

Document a written transfer-pricing policy.

Even small operators benefit from a one-page memo explaining how intercompany fees are calculated.

Layer in a 401(k) or defined-benefit plan inside MgmtCo. Retirement contributions become deductible outside the 280E perimeter.

Learn more about audit-defense planning at Tranzesta.com. Tranzesta has built each of these tactics into a repeatable playbook.

Conclusion

A smart cannabis business structure tax minimize plan is the single highest-leverage decision a US operator can make. The three biggest takeaways are: choose the right base entity for each activity, separate plant-touching from non-plant-touching work in a HoldCo-OpCo-MgmtCo structure, and document every intercompany agreement at arm’s length. As a result, your effective tax rate drops, your audit risk shrinks, and your business scales cleanly.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

The best cannabis business structure tax minimize plan for most US operators is a multi-entity setup with a holding company, a plant-touching operating LLC, and a separate non-plant-touching management company. This structure isolates Section 280E exposure to only the plant-touching entity. Therefore, expenses inside the management company remain fully deductible. Tranzesta typically recommends this design for any US cannabis business with annual revenue above $1 million, although smaller operators can also benefit from a simplified two-entity version.

For most cannabis operators in the United States, an LLC is the strongest starting point. LLCs offer pass-through taxation, simpler administration, and more flexibility for related-party planning. However, a C-Corp can make sense if you plan to raise institutional capital or pursue a public listing. Both entities face Section 280E exposure equally, so the choice is driven by capital strategy rather than tax savings. Tranzesta helps US operators model both options before filing entity paperwork.

cannabis business can deduct only the portion of rent allocable to cultivation, manufacturing, or other plant-touching production activities under Treas. Reg. §1.471-3. Retail floor rent, executive office rent, and marketing-space rent are disallowed under Section 280E. As a result, US operators often hold real estate in a separate LLC and structure leases so cultivation rent is captured as COGS. Tranzesta runs a square-footage allocation study to maximize the deductible portion.

Multi-state cannabis operators in the United States minimize tax burden by combining entity segregation with state-by-state apportionment planning. Each state has different sourcing rules, throwback provisions, and excise taxes. Therefore, a holding company with state-specific operating subsidiaries usually performs best. Additionally, intercompany management fees must be priced at arm’s length and documented in writing. Tranzesta handles multi-state structures across California, Colorado, Michigan, New Jersey, Massachusetts, and other US adult-use markets.

Tranzesta is a US-based tax consultation firm that designs cannabis business structures, capitalizes the right costs into COGS under Section 280E, files federal and state returns, manages Form 8300 cash-reporting workflows, and provides full audit defense. Tranzesta works with cultivators, manufacturers, distributors, and dispensaries across the United States. For a free consultation, contact hello@tranzesta.com or visit Tranzesta.com to schedule a tax strategy session with our cannabis tax team.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation