Cannabis business owners in the United States

face one of the most complex tax environments in any industry. The conflict between federal and state laws creates confusion, risk, and often higher tax bills. In fact, many operators overpay or underpay simply because they don’t fully understand cannabis business taxes federal state rules.

If you run a dispensary, cultivation facility, or cannabis brand, this guide will break everything down in plain English. You’ll learn how federal tax law differs from state rules, how IRS Section 280E impacts your profits, and how to stay compliant in 2026.

Let’s start with the foundation so you can see exactly where the challenges begin.

What Is Cannabis Business Taxes Federal State?

Cannabis business taxes federal state refers to the difference between how cannabis businesses are taxed at the federal level versus the state level in the United States.

At the federal level, cannabis is still classified as a Schedule I controlled substance. As a result, businesses cannot deduct normal expenses under IRS rules. However, many US states have legalized cannabis and allow standard deductions.

This mismatch creates a major financial and compliance gap.

Federal vs State Tax Treatment

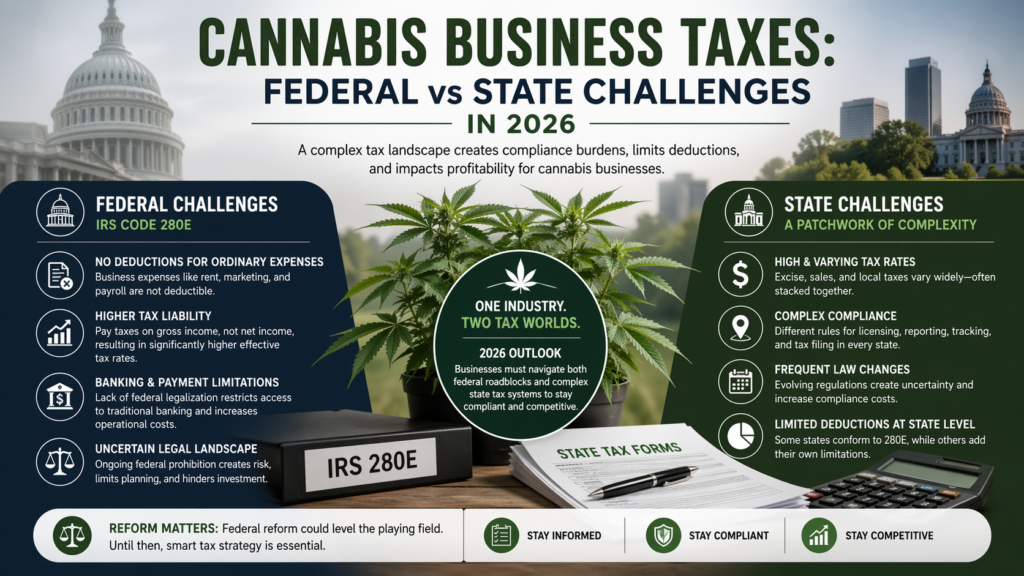

At the federal level, the IRS enforces Section 280E of the Internal Revenue Code. This rule prohibits cannabis businesses from deducting ordinary business expenses like rent, payroll, or marketing.

However, at the state level, many jurisdictions—such as California, Colorado, and Illinois—have decoupled from 280E. That means they allow standard deductions for state tax purposes.

Therefore, cannabis businesses often calculate two different taxable incomes: one for federal taxes and another for state taxes.

Why This Matters for Cannabis Businesses

This dual system significantly increases your effective tax rate. In many cases, cannabis operators in the USA pay 60%–80% in combined taxes if not properly structured.

Additionally, the compliance burden increases. You must maintain detailed records and separate accounting systems to satisfy both federal and state requirements.

As a result, understanding cannabis business taxes federal state is not optional—it’s critical for survival and profitability.

How Do Cannabis Business Taxes Federal State Rules Work?

Cannabis business taxes federal state rules work by applying conflicting legal frameworks to the same business income.

At the federal level, strict IRS rules apply. At the state level, more flexible tax policies may exist depending on where you operate.

Federal Tax Rules (IRS Section 280E)

Under IRS Section 280E, businesses trafficking in controlled substances cannot deduct ordinary and necessary expenses. This includes:

Rent and utilities

Employee wages

Marketing and advertising

Office supplies

However, businesses can deduct Cost of Goods Sold (COGS). COGS includes direct costs such as inventory, raw materials, and production expenses.

According to the IRS, proper inventory accounting is essential. You can review official guidance here:

Learn more from the IRS (opens in new tab): https://www.irs.gov/businesses/small-businesses-self-employed/cost-of-goods-sold

State-Level Tax Flexibility

Many US states have passed legislation allowing cannabis businesses to deduct normal expenses at the state level.

For example:

California allows deductions disallowed by 280E

Colorado permits state-level expense deductions

New York aligns with standard business deduction rules

Therefore, your taxable income for state taxes is often lower than your federal taxable income.

This creates a major planning opportunity—but also adds complexity.

Common Challenges in Cannabis Business Taxes Federal State

Cannabis businesses face several unique challenges due to the federal and state tax divide.

Misunderstanding Section 280E

Many operators underestimate the impact of 280E. As a result, they fail to plan for higher federal taxes and face cash flow issues.

Poor Record-Keeping

Accurate accounting is essential. However, many businesses fail to separate COGS from operating expenses properly. This leads to IRS audits and penalties.

Mixing Personal and Business Expenses

Some owners blur the line between personal and business spending. This increases audit risk and reduces allowable deductions.

Ignoring State-Specific Rules

Each state has different cannabis tax laws. Therefore, applying a one-size-fits-all strategy can lead to compliance issues.

Lack of Professional Guidance

Many cannabis entrepreneurs try to handle taxes alone. However, this industry requires specialized expertise in US tax law.

Step-by-Step Guide to Managing Cannabis Business Taxes Federal State

Managing cannabis business taxes federal state requires a structured and proactive approach.

Step 1: Understand Your Federal Tax Obligations

Start by reviewing IRS Section 280E. Know what you can and cannot deduct.

Focus on maximizing COGS legally to reduce taxable income.

Step 2: Identify Your State Tax Position

Next, determine whether your state allows deductions disallowed by 280E.

Each US state has unique rules, so review your state tax code carefully.

Step 3: Set Up Proper Accounting Systems

Use accounting software designed for cannabis businesses. Track:

Inventory costs

Direct production expenses

Operating expenses separately

This separation is critical for compliance.

Step 4: Maintain Detailed Documentation

Keep records of every transaction. This includes invoices, receipts, and payroll data.

Good documentation protects you during IRS audits.

Step 5: Work With a Cannabis Tax Specialist

Cannabis taxation is highly specialized. Therefore, working with experts ensures compliance and optimization.

Step 6: Plan for Estimated Taxes

Federal and state tax liabilities can differ significantly. Set aside funds for both to avoid surprises.

Step 7: Review and Adjust Quarterly

Tax laws change frequently in the USA cannabis industry. Regular reviews help you stay compliant and reduce risk.

How Tranzesta Can Help With Cannabis Business Taxes Federal State

Tranzesta is a US-based tax consultation firm specializing in complex tax scenarios like cannabis business taxes federal state. We help cannabis operators stay compliant while reducing unnecessary tax burdens.

Our services include:

Cannabis-specific bookkeeping and accounting

IRS Section 280E compliance strategies

State tax optimization planning

Financial structuring for dispensaries and growers

Additionally, Tranzesta supports multi-state operators navigating different compliance requirements across the USA.

Contact our team at hello@tranzesta.com for a free consultation.

Visit Tranzesta.com to learn more about our cannabis accounting services.

You can also learn more about tax compliance strategies at Tranzesta.com and explore advanced bookkeeping solutions for cannabis businesses at Tranzesta.com.

Cannabis Business Taxes Federal State: Expert Tips for 2026

Cannabis business taxes federal state will continue evolving in 2026. Therefore, staying ahead of changes is essential.

Here are expert strategies from Tranzesta:

Maximize COGS allocation legally to reduce federal taxable income

Separate business entities where appropriate to improve tax efficiency

Stay updated on federal reform proposals, such as potential 280E repeal

Use accrual accounting for better financial visibility

Conduct quarterly tax planning instead of waiting until year-end

Additionally, consider long-term structuring strategies. For example, some businesses restructure operations to optimize tax treatment under current laws.

The US cannabis industry generated over $30 billion in legal sales in recent years. As the market grows, IRS scrutiny is also increasing.

Therefore, proactive tax planning is no longer optional—it’s essential.

Conclusion

Cannabis business taxes federal state rules create a complex but manageable system when you understand the fundamentals.

First, federal law under Section 280E limits deductions. Second, many US states allow those deductions, creating dual tax systems. Third, proper planning and accounting can significantly reduce your tax burden.

If you want to stay compliant and maximize profits, expert guidance is critical.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

Cannabis business taxes federal state rules stem from IRS Section 280E, which prevents businesses dealing in controlled substances from deducting ordinary expenses. Because cannabis is still illegal at the federal level in the United States, businesses cannot claim typical deductions like rent or payroll. However, they can deduct Cost of Goods Sold, which helps reduce taxable income.

Cannabis business taxes federal state rules allow deductions only for Cost of Goods Sold under Section 280E. This includes inventory costs, raw materials, and production expenses. Operating costs such as marketing, rent, and administrative salaries are not deductible federally. Proper accounting is essential to maximize allowable deductions legally.

Cannabis business taxes federal state differences exist because many US states do not follow federal rules. States like California and Colorado allow businesses to deduct ordinary expenses for state taxes. Therefore, cannabis operators often calculate separate taxable income for federal and state filings.

Cannabis business taxes federal state planning strategies include maximizing Cost of Goods Sold, maintaining detailed records, and structuring operations efficiently. Working with a specialized tax firm like Tranzesta ensures compliance while identifying legal ways to reduce tax liability in the United States.

Cannabis business taxes federal state laws may change if federal legalization occurs in the USA. Proposed reforms could eliminate Section 280E, allowing standard deductions. However, until laws change, businesses must comply with current IRS regulations and plan accordingly.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation