Every US business that pays wages is required

to collect and remit FICA taxes — no exceptions. FICA tax, Social Security, and Medicare obligations for businesses generate more than $1.2 trillion in federal revenue each year, yet they remain one of the most misunderstood areas of American tax law. A single payroll miscalculation can trigger IRS penalties of up to 15% of the unpaid amount.

In this complete 2026 guide, you will learn

exactly what FICA tax covers, how Social Security and Medicare rates work, who owes what, the most expensive mistakes to avoid, and a step-by-step process for getting compliant. Whether you are a self-employed content creator, a cannabis business owner, a traditional employer, or a US expat with stateside income, this resource was built for you.

Let’s start with the fundamentals — what FICA actually is and why it matters to your bottom line.

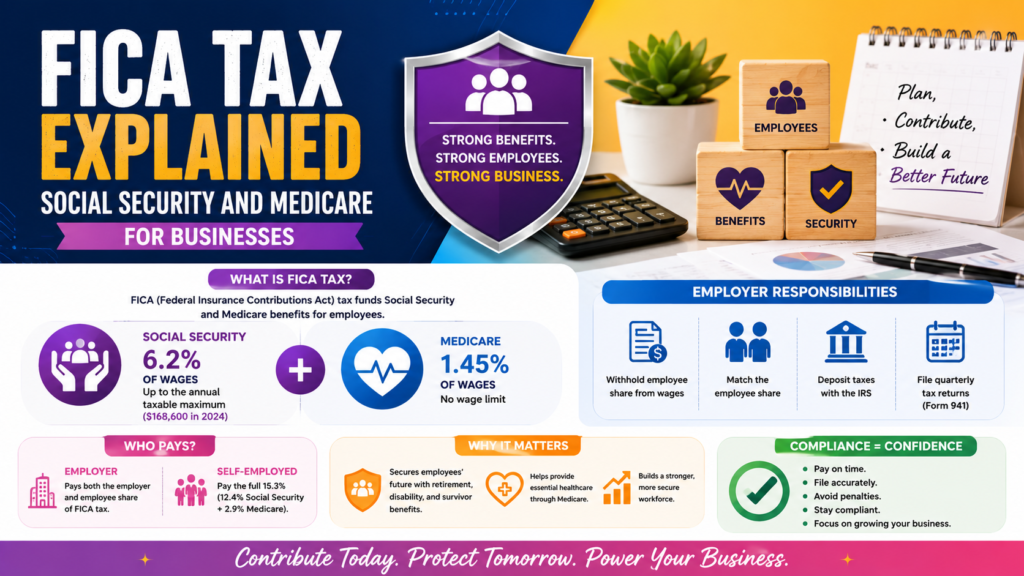

What Is FICA Tax? Social Security and Medicare for Businesses Defined

FICA tax is a mandatory federal payroll tax that funds two programs: Social Security and Medicare. The Federal Insurance Contributions Act (FICA), first enacted in 1935, requires employers and employees to each contribute a fixed percentage of wages to these programs. Self-employed individuals pay both shares themselves through the Self-Employment (SE) Tax.

For US businesses, FICA is not optional

and it is not a one-time obligation. Every pay period, employers must withhold FICA from employee wages and match those contributions dollar for dollar. Failure to do so results in the Trust Fund Recovery Penalty (TFRP), which the IRS can assess personally against business owners and responsible parties.

Understanding the structure of FICA is the first step toward building accurate, penalty-free payroll.

How FICA Splits Into Social Security and Medicare

FICA tax has two distinct components, each funding a separate federal program:

Social Security Tax: Funds retirement, disability, and survivor benefits. Rate: 6.2% employee + 6.2% employer = 12.4% combined. Applies only up to the annual Social Security wage base.

Medicare Tax: Funds hospital insurance (Medicare Part A). Rate: 1.45% employee + 1.45% employer = 2.9% combined. Applies to all wages with no dollar cap.

Therefore, the combined FICA rate per employee is 7.65% (employee share) + 7.65% (employer match) = 15.3% of gross wages up to the wage base, then 2.9% above it.

Who Must Pay FICA Tax in the United States?

FICA applies across a wide range of income earners in the USA. The following groups carry FICA obligations:

W-2 employees and their employers

Self-employed individuals (freelancers, sole proprietors, content creators)

OnlyFans creators and social media influencers with net earnings above $400

Cannabis industry operators and their employees

S-Corp shareholder-employees on their reasonable salary

US expats with stateside self-employment income

FICA Tax Rates, Wage Bases, and Key IRS Rules for 2026

The IRS updates FICA wage thresholds annually, so knowing the 2026 figures is essential for accurate payroll processing and quarterly deposits.

2026 FICA Tax Rates: The Numbers You Need

Social Security — Employee: 6.2% on wages up to the wage base

Social Security — Employer: 6.2% (mirrors the employee rate)

Medicare — Employee: 1.45% on all wages, no cap

Medicare — Employer: 1.45% (mirrors the employee rate)

Additional Medicare Tax: 0.9% on employee wages exceeding $200,000 (employer does not match this)

Self-Employment (SE) Tax: 15.3% on net SE income up to the wage base, then 2.9% above it

The Social Security Wage Base Limit

Social Security tax only applies to wages up to the annual wage base limit. The IRS set this figure at $176,100 for 2025 and adjusts it upward each year based on national average wage growth. Once an employee’s cumulative wages from your business exceed this threshold for the calendar year, you stop withholding and matching Social Security tax for that employee — until January 1 restarts the clock.

Medicare tax, however, carries no wage cap. It applies to every dollar an employee earns, all year long. For complete 2026 wage base figures, refer to IRS Publication 15 (Employer’s Tax Guide) at IRS.gov

IRS Reference: See IRS Publication 15 and Schedule SE for current rates and calculation worksheets. Always verify thresholds annually — they change every January.

The Additional Medicare Tax: What High-Earning Employees Trigger

The Affordable Care Act introduced a 0.9% Additional Medicare Tax on wages and self-employment income above set thresholds: $200,000 for single filers, $250,000 for married filing jointly, and $125,000 for married filing separately.

Employers must begin withholding this surtax the moment a single employee’s wages from that business exceed $200,000 in the calendar year — regardless of the employee’s total household income. The employer does not contribute a matching 0.9%. This creates a common error when businesses fail to track individual wage milestones.

Self-Employment Tax: Paying Both Sides Yourself

Self-employed individuals — including freelancers, creators, and sole proprietors — owe the full 15.3% SE Tax on net self-employment income because no employer exists to share the load. However, the IRS provides relief: self-employed taxpayers may deduct 50% of SE Tax as an above-the-line deduction on Form 1040. This deduction reduces Adjusted Gross Income (AGI) and lowers overall tax liability. Net self-employment income above $400 triggers the filing requirement for Schedule SE.

Common FICA Tax Mistakes That Cost US Businesses Money

FICA errors rank among the costliest payroll mistakes a US business can make. The IRS assesses civil penalties for late deposits, incorrect withholding, and misclassified workers — and interest accrues daily. Knowing these mistakes in advance helps you avoid them entirely.

Mistake 1: Misclassifying Employees as Independent Contractors

This is the single most common FICA-related error in the United States. When a business classifies a worker as an independent contractor, the employer owes no FICA. However, the IRS applies a three-part test — behavioral control, financial control, and type of relationship — to determine actual worker status.

If the IRS reclassifies a contractor as an employee after the fact, the business owes back FICA taxes, matching employer contributions, penalties, and accumulated interest. In some cases, the Trust Fund Recovery Penalty applies to individual owners personally.

Mistake 2: Ignoring Self-Employment Tax as a Creator or Freelancer

Many OnlyFans creators, influencers, and gig workers treat their income as “extra cash” and underestimate their FICA obligations. Any net self-employment income above $400 per year requires filing Schedule SE and paying SE Tax. Additionally, missing quarterly estimated tax payments — due April 15, June 15, September 15, and January 15 — compounds the underpayment with IRS penalties.

Mistake 3: Depositing FICA Taxes Late

Employers must deposit FICA taxes electronically through the Electronic Federal Tax Payment System (EFTPS) on a monthly or semi-weekly schedule determined by the IRS. Many business owners confuse the deposit deadline with the quarterly Form 941 filing deadline — these are different obligations. Late deposits trigger penalties ranging from 2% (1–5 days late) up to 15% (more than 10 days after IRS notice).

Mistake 4: Missing the Additional Medicare Tax Withholding Trigger

Employers must start withholding the additional 0.9% Medicare surtax once a single employee’s wages from your business cross $200,000 in the calendar year. Missing this trigger — especially in businesses with highly compensated employees or owner-employees of S-Corps — creates a year-end discrepancy that generates IRS notices and potential penalties.

Mistake 5: Assuming Cannabis Businesses Are Exempt from FICA

Some cannabis operators assume that federal restrictions under IRC Section 280E — which limits allowable deductions for cannabis businesses — also reduce payroll tax obligations. This is incorrect. FICA taxes are fully owed on all employee wages in cannabis businesses, regardless of federal cannabis scheduling. Additionally, FICA errors in the cannabis industry can attract heightened IRS scrutiny given the sector’s complex compliance profile.

How to Calculate and Pay FICA Tax: A Step-by-Step Guide for Business Owners

Following a clear, sequential process for FICA compliance protects your business from penalties and keeps your payroll records audit-ready. Here are seven actionable steps every US employer and self-employed individual should follow.

1. Determine Gross Wages Per Pay Period.

Calculate total gross compensation for each employee: regular wages, overtime, bonuses, commissions, and taxable fringe benefits. Certain items — like qualified expense reimbursements — may be excludable. Consult IRS Publication 15-B for a full exclusion list.

2. Apply the Social Security Rate.

Withhold 6.2% from each employee’s gross wages up to the annual wage base limit. Calculate your matching 6.2% employer share. Stop collecting Social Security tax once wages exceed the wage base for the year.

3. Apply the Medicare Rate.

Withhold 1.45% from all employee wages without any cap. Match with another 1.45% as the employer. Check whether any employee has crossed the $200,000 threshold this calendar year to trigger the 0.9% Additional Medicare Tax withholding.

4. Deposit FICA Taxes via EFTPS on Schedule.

Use the Electronic Federal Tax Payment System (EFTPS) at eftps.gov to make timely deposits. The IRS assigns you either a monthly or semi-weekly deposit schedule based on your lookback-period payroll liability. Never wait until Form 941 to pay — the deposit and the filing are separate requirements.

5. File Form 941 Each Quarter.

Submit IRS Form 941 (Employer’s Quarterly Federal Tax Return) to report wages paid, employee FICA withheld, and employer FICA matched. Quarterly deadlines: April 30, July 31, October 31, and January 31.

6. Reconcile Payroll at Year-End.

At December 31, reconcile all FICA amounts reported quarterly on Form 941 against each employee’s Form W-2. Discrepancies between these two sets of figures trigger automated IRS notices. File W-2s with the Social Security Administration (SSA) by January 31.

7. Calculate Self-Employment Tax on Schedule SE (If Self-Employed).

Take net profit from Schedule C. Multiply by 92.35% to arrive at net earnings from self-employment. Apply 15.3% SE Tax up to the wage base, then 2.9% above it. Deduct 50% of SE Tax on Form 1040 Line 15 to reduce your AGI and overall tax bill.

How Tranzesta Helps Businesses Handle FICA Tax

Tranzesta is a US-based tax consultation firm that specializes in payroll tax compliance, self-employment taxes, and complex business tax situations. Our team works with business owners across the United States to ensure FICA obligations are calculated correctly, deposits are made on time, and quarterly and annual filings are accurate.

We serve several client groups that face unique FICA challenges:

Content Creators & OnlyFans Professionals: SE Tax calculation, quarterly estimated payment planning, multi-platform income reconciliation, and state filing support.

Cannabis Business Operators: Full payroll tax compliance alongside IRC 280E planning — because FICA taxes do not take a day off regardless of federal scheduling.

Small and Mid-Size Businesses: Payroll tax setup, deposit scheduling, Form 941 filing, year-end W-2 reconciliation, and worker classification reviews.

Self-Employed Individuals and Freelancers: SE Tax optimization, estimated tax payment calendars, and deduction strategies to minimize AGI.

US Expats with US-Source Income: FICA compliance coordination alongside Streamlined Filing services for Americans coming back into IRS compliance.

Do not let a FICA miscalculation cost your business thousands in penalties. Contact our team at hello@tranzesta.com for a free consultation and get complete clarity on your payroll tax obligations today.

Visit Tranzesta.com to learn more about our business tax and bookkeeping services, or explore our content creator tax services for platform-specific guidance.

FICA Tax Social Security Medicare Business: Expert Tips for 2026

Beyond the compliance basics, experienced tax professionals use proactive strategies to manage FICA more efficiently. Tranzesta shares these insider tips to help US business owners and self-employed individuals reduce liability and avoid surprises.

Consider S-Corp Election. Self-employed individuals paying full 15.3% SE Tax may reduce their FICA exposure significantly through S-Corp status. As a shareholder-employee, you pay SE Tax only on your reasonable salary — distributions are not subject to SE Tax. However, the IRS scrutinizes unreasonably low salaries, so this strategy requires careful, documented implementation.

Maximize the SE Tax Deduction.

Self-employed taxpayers can deduct 50% of SE Tax from gross income as an above-the-line deduction. This deduction is frequently missed in DIY returns, resulting in a higher AGI and a larger total tax bill than necessary. Even a modest SE Tax liability of $10,000 generates a $5,000 deduction.

Set Up Automated EFTPS Deposits.

Automate your FICA deposit schedule through EFTPS at the start of each year. Consistent, on-time deposits eliminate the most common — and most expensive — FICA penalty: the late deposit penalty. Build the deposit dates into your calendar alongside Form 941 deadlines.

Review Worker Classification Annually.

If your business uses both employees and independent contractors, audit your classifications every January. The IRS’s behavioral control, financial control, and relationship-type framework shifts as working arrangements evolve. Catching a misclassification proactively costs far less than an IRS audit.

Track the $200,000 Additional Medicare Threshold Individually.

Build a payroll system that flags each employee’s wages individually once they approach $200,000. The trigger is per-employer — not household income — so multi-employer households may underpay at the individual employer level without knowing.

Reconcile Payroll Monthly, Not Just Quarterly.

Monthly payroll reconciliation catches FICA errors before they compound into quarterly Form 941 discrepancies. Tranzesta’s bookkeeping team helps businesses maintain clean, audit-ready records year-round. Learn more about our Streamlined Filing and compliance services at Tranzesta.com.

Conclusion: FICA Compliance Protects Your Business and Your People

Three takeaways stand above everything else in this guide. First, FICA tax is a shared obligation — employees and employers each contribute, and the self-employed carry both sides. Second, the rates, wage bases, and thresholds update each January, so staying current with IRS guidance is a year-round responsibility, not a one-time task. Third, mistakes — from misclassified workers to missed deposit deadlines — carry real financial penalties that compound quickly and can become personal liability under the Trust Fund Recovery Penalty.

Fortunately, FICA compliance is fully manageable with the right systems, accurate recordkeeping, and expert guidance. Tranzesta works with businesses and self-employed individuals across the United States to ensure payroll taxes are calculated, deposited, and reported accurately — every pay period, every quarter, every year.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

FICA tax is a federal payroll tax that funds Social Security and Medicare. For US businesses, FICA works as a shared obligation: the employer withholds 6.2% for Social Security and 1.45% for Medicare from each employee’s wages, then matches those amounts dollar for dollar out of business funds. Self-employed individuals pay the full 15.3% themselves through the Self-Employment Tax. Employers must deposit FICA taxes electronically through EFTPS and file Form 941 each quarter to report amounts withheld and matched.

FICA tax rates in 2026 are 6.2% for Social Security (each for employee and employer, totaling 12.4%) and 1.45% for Medicare (each, totaling 2.9%). Combined, this is 7.65% per side — or 15.3% total — up to the Social Security wage base. Social Security tax stops once wages reach the annual wage base limit (confirm the 2026 figure at IRS.gov). Medicare applies to all wages. An additional 0.9% Medicare surtax applies to employee wages above $200,000, which the employer does not match.

Yes. Self-employed individuals pay FICA through the Self-Employment Tax, which equals 15.3% of net self-employment income up to the annual Social Security wage base, and 2.9% above it. Because no employer exists to share the load, the self-employed individual covers both sides. However, the IRS allows a deduction of 50% of SE Tax as an above-the-line deduction on Form 1040, which reduces Adjusted Gross Income. Net self-employment income above $400 per year triggers the requirement to file IRS Schedule SE.

Social Security tax funds retirement, disability, and survivor benefits administered by the Social Security Administration. It carries a combined rate of 12.4% (6.2% each for employee and employer) and applies only up to the annual wage base limit. Medicare tax funds hospital insurance under Medicare Part A, carrying a combined rate of 2.9% (1.45% each). Unlike Social Security, Medicare has no wage cap — it applies to every dollar earned. High earners above $200,000 also pay a 0.9% Additional Medicare surtax.

Yes, there are legal strategies to reduce FICA tax exposure for US business owners. Electing S-Corp taxation allows shareholder-employees to pay SE Tax only on a reasonable salary — not on profit distributions — which can significantly lower the total FICA burden. Self-employed individuals should always claim the 50% SE Tax deduction on Form 1040 to reduce AGI. Correctly classifying workers as independent contractors (where IRS criteria are legitimately met) also avoids the employer FICA match. Consult Tranzesta at hello@tranzesta.com to evaluate the right approach for your situation.