Did you know that failing to understand capital gains

tax 2026 short-term long-term rules could cost you thousands of dollars in avoidable taxes? In 2026, the IRS will tax capital gains differently depending on how long you held an asset — and the difference between short-term and long-term rates can be dramatic. Whether you are a self-employed individual, a content creator, a cannabis business owner, or a US expat, knowing which rate applies to your situation is not optional. It is essential.

In this guide, you will learn exactly how capital gains taxes work in 2026, what rates apply to your income level, common mistakes US taxpayers make, and — most importantly — how to legally reduce your tax liability. By the end, you will have a clear roadmap for handling investment gains on your federal tax return.

What Are Capital Gains Taxes? An Overview for US Taxpayers

A capital gain is the profit you earn when you sell an asset — such as stocks, real estate, cryptocurrency, or business property — for more than you originally paid for it. In the United States, the IRS taxes these gains, and how much you pay depends primarily on one thing: how long you held the asset before selling it.

The distinction between short-term and long-term capital gains is one of the most important concepts in US tax law. Understanding it correctly can mean the difference between paying 10% and paying 37% on the same dollar of profit. For self-employed individuals, freelancers, and small business owners in particular, capital gains from selling business assets or investments frequently appear on a tax return without much warning.

Why Capital Gains Tax Matters in 2026

The tax landscape in 2026 is shaped by the expiration provisions of the Tax Cuts and Jobs Act (TCJA), which was originally passed in 2017. Many of the individual income tax provisions from the TCJA were set to expire after 2025, meaning 2026 could bring higher ordinary income tax rates for some taxpayers. As a result, the difference between short-term and long-term capital gains taxation becomes even more significant this year.

Additionally, the Net Investment Income Tax (NIIT), at 3.8%, continues to apply to certain higher earners in addition to standard capital gains rates. US taxpayers with modified adjusted gross income (MAGI) above $200,000 (single) or $250,000 (married filing jointly) should factor this in when planning asset sales.

Who Is Affected by Capital Gains Taxes?

Capital gains taxes affect a wide range of taxpayers in the United States. Content creators who invest their earnings in stocks or real estate, self-employed professionals who sell business assets, cannabis business owners who transfer or sell their licensed operations, and U.S. expats who maintain investment accounts in the U.S. are all subject to these rules.

Even selling a personal home can trigger capital gains tax if profits exceed the IRS exclusion limits: $250,000 for single filers and $500,000 for married couples filing jointly under Section 121 of the Internal Revenue Code.

Capital Gains Tax 2026 Short-Term Long-Term: Rates, Rules, and IRS Brackets

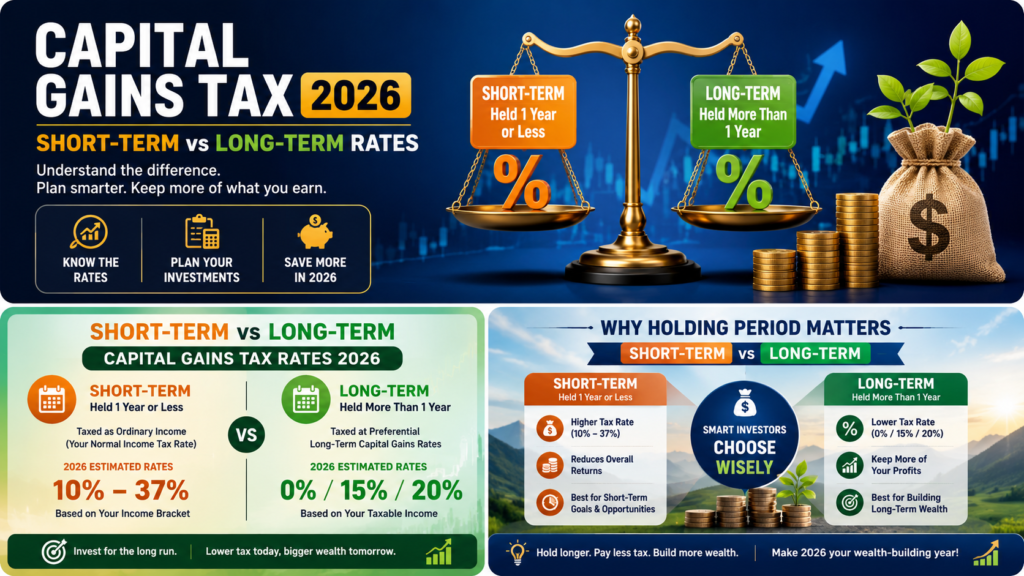

The IRS divides capital gains into two clear categories based on the holding period of the asset sold. Here is how each works in 2026.

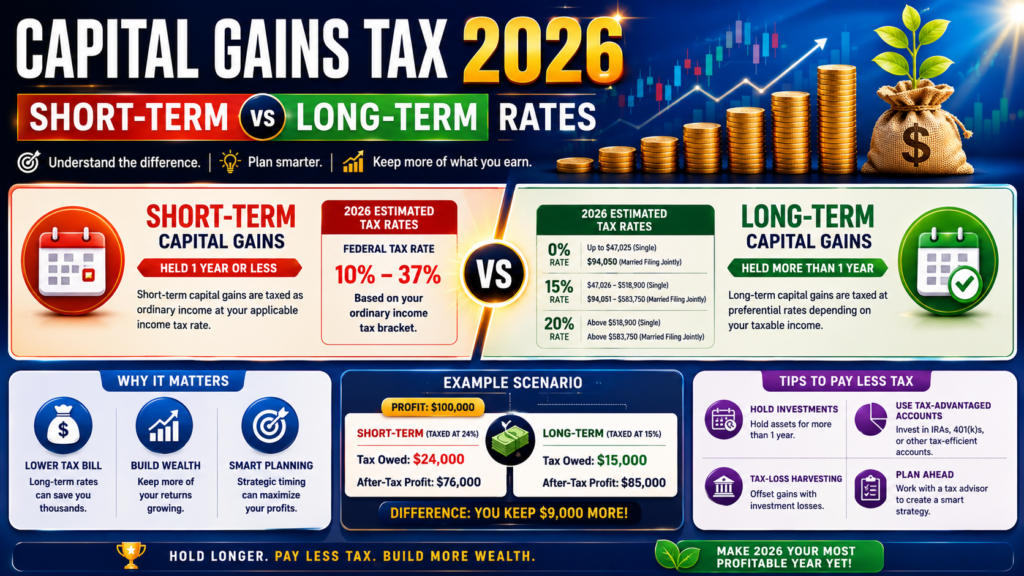

Short-Term Capital Gains Rates in 2026

Short-term capital gains apply when you sell an asset you held for one year or less. The IRS taxes these gains at your ordinary income tax rate — the same rate you pay on wages, freelance income, or business profits. In 2026, with potential TCJA expirations, ordinary income tax rates may revert to pre-2018 levels, which could mean a top marginal rate of 39.6% for the highest earners.

Here are the potential 2026 ordinary income tax brackets for single filers (rates subject to IRS confirmation):

For self-employed content creators and business owners, short-term gains stack on top of ordinary income — pushing you into a higher bracket if you are not careful.

Long-Term Capital Gains Rates in 2026

Long-term capital gains apply when you hold an asset for more than one year before selling. The IRS taxes these gains at preferential rates: 0%, 15%, or 20%, depending on your taxable income. These are the 2026 long-term capital gains rate brackets for single filers:

0% rate: Taxable income up to approximately $47,025

15% rate: Taxable income from $47,026 to $518,900

20% rate: Taxable income above $518,900

For married filing jointly, the thresholds are higher.

The 0% bracket extends to roughly $94,050, and the 20% rate kicks in above approximately $583,750.

Additionally, high-income US taxpayers may owe the Net Investment Income Tax (NIIT) of 3.8% on long-term capital gains if their modified adjusted gross income exceeds $200,000 (single) or $250,000 (married). This means the effective top rate on long-term gains can reach 23.8%.

Special Rates: Collectibles and Section 1202 Stock

Certain asset types face different long-term capital gains rates. Gains from collectibles — such as art, antiques, coins, and precious metals — are taxed at a maximum rate of 28% under IRC Section 1(h)(4). Gains from qualified small business stock (QSBS) under Section 1202 of the Internal Revenue Code may be partially or fully excluded from federal tax for eligible investors, subject to specific holding period and business requirements.

For authoritative rate tables and current year guidance, see the IRS publication on capital gains at

For the most current rates and brackets, visit the IRS capital gains topic page at IRS Topic No. 409 — Capital Gains and Losses (opens in new tab).

Common Capital Gains Tax Mistakes US Taxpayers Make in 2026

Even experienced investors and business owners make costly errors when reporting capital gains. Here are the most frequent mistakes to avoid this tax year.

Mistake 1: Confusing Holding Period Rules

Many taxpayers assume they qualify for long-term rates simply because they have held an asset for around a year. However, the IRS rule is strict: the holding period must be more than 12 months — not 12 months exactly. If you bought stock on January 15, 2025, you must sell it on or after January 16, 2026 to qualify for long-term rates. Selling even one day early triggers the higher short-term rate.

Mistake 2: Forgetting State Capital Gains Taxes

Federal rates are only part of the picture. Most US states impose their own capital gains taxes on top of federal rates. California, for example, taxes capital gains as ordinary income with a top rate of 13.3%. New York adds up to 10.9%. Only a handful of states — including Texas, Florida, and Nevada — have no state income tax. Self-employed individuals and content creators who relocate between states must also consider sourcing rules carefully.

Mistake 3: Ignoring Wash-Sale Rules on Investment Losses

The IRS wash-sale rule under IRC Section 1091 disallows a capital loss deduction if you repurchase the same or substantially identical security within 30 days before or after the sale. Many US taxpayers harvest losses at year-end to offset gains, then immediately rebuy the same stock — inadvertently triggering the wash-sale rule. Cryptocurrency is currently not subject to wash-sale rules, but legislation may change this.

Mistake 4: Not Reporting Crypto, NFT, or Digital Asset Gains

The IRS treats cryptocurrency and digital assets as property. Every sale, trade, or use of crypto to purchase goods triggers a taxable event. US taxpayers who neglect to report these gains face penalties, interest, and potential audit risk. In 2026, expanded reporting requirements under the Infrastructure Investment and Jobs Act apply to crypto brokers, increasing IRS visibility into digital asset transactions.

Mistake 5: Missing the Net Investment Income Tax

Higher-earning taxpayers often overlook the 3.8% Net Investment Income Tax (NIIT) that applies to capital gains. For a single filer earning $250,000 with a $50,000 long-term gain, the effective rate on those gains is not just 15% — it is 18.8% after the NIIT. Ignoring this surcharge leads to underpayment and potential penalties.

How to Calculate and Report Capital Gains Tax in 2026: Step-by-Step

Reporting capital gains correctly on your federal return requires careful tracking and accurate calculations. Tranzesta.com Follow these steps to stay compliant and minimize your liability.

Step 1 — Identify Every Taxable Asset Sale

List all assets you sold during the tax year, including stocks, mutual funds, ETFs, real estate, cryptocurrency, NFTs, business assets, and collectibles. Do not overlook assets sold through brokerage accounts — your broker will issue a Form 1099-B, but it may not capture all gains accurately.

Step 2 — Determine Your Cost Basis

Your cost basis is generally what you originally paid for the asset, plus any commissions or fees. For inherited assets, the basis is typically the fair market value at the date of death (stepped-up basis under IRC Section 1014). For gifted assets, the rules differ. Accurate basis tracking is the foundation of correct capital gains reporting.

Step 3 — Calculate the Holding Period

For each asset sold, calculate the number of days between the acquisition date and the sale date. If the period is 365 days or less, the gain is short-term. If it exceeds 365 days, the gain is long-term. Document this for every transaction — the IRS may request supporting records.

Step 4 — Apply Applicable Rates

Multiply your net short-term gains by your marginal ordinary income tax rate, and multiply net long-term gains by the applicable 0%, 15%, or 20% rate based on your taxable income bracket. Add the 3.8% NIIT if your MAGI exceeds the threshold. For cannabis business owners, note that IRC Section 280E restricts deductions, but capital gains from asset sales are generally still subject to standard capital gains rates.

Step 5 — Complete Schedule D and Form 8949

Report all capital gain and loss transactions on IRS Form 8949, then summarize the totals on Schedule D of your Form 1040. Short-term and long-term transactions are reported separately. Losses offset gains within the same category first, then cross-category netting rules apply. Net capital losses up to $3,000 per year may offset ordinary income, with excess losses carried forward.

Step 6 — Explore Loss Harvesting and Timing Strategies

Consider whether you can defer a sale into the next tax year, accelerate deductible losses before year-end, or shift income-producing assets to a lower-bracket family member. These are legal strategies that US taxpayers use to reduce capital gains liability. Always confirm strategies with a qualified tax professional before executing.

Step 7 — Pay Estimated Taxes If Needed

If you expect to owe more than $1,000 in federal taxes from capital gains, the IRS requires quarterly estimated tax payments. Use IRS Form 1040-ES to calculate and remit payments. Underpayment can result in penalties assessed under IRC Section 6654. Self-employed individuals and content creators with variable income must be especially vigilant about this step.

How Tranzesta Can Help You Navigate Capital Gains Tax in 2026

Managing capital gains tax effectively requires more than reading a rate table. It requires proactive planning, accurate recordkeeping, and the guidance of professionals who understand your specific situation. That is exactly what Tranzesta.com delivers.

Tranzesta is a US-based tax consultation firm with deep expertise in business tax strategy, self-employment taxes, and investment income reporting. Our team works with a diverse range of clients — including content creators, cannabis business operators, self-employed freelancers, and US expats — to develop personalized tax plans that minimize capital gains liability within the bounds of US law.

Our capital gains services include: holding period analysis and timing strategy, cost basis review and reconciliation, Schedule D and Form 8949 preparation, Net Investment Income Tax planning, loss harvesting guidance, and quarterly estimated tax projections. We also integrate capital gains planning with your broader business tax strategy, ensuring that every decision supports your long-term financial goals.

Learn more about our business tax services at Tranzesta.com.

Ready to reduce your capital gains tax bill? Contact our team at hello@tranzesta.com for a free consultation.

Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

Capital Gains Tax 2026 Short-Term Long-Term: Expert Tips to Keep More of Your Money

Smart taxpayers do not just react to capital gains — they plan for them. Here are advanced strategies that Tranzesta recommends for US taxpayers managing investment income in 2026.

Max out tax-advantaged accounts: Gains inside a Roth IRA or 401(k) are not subject to capital gains tax. Prioritizing investments within these accounts shields growth from annual taxation.

Time large asset sales strategically: If you are near year-end and your income is lower than expected, accelerating a sale before December 31 may allow you to use the 0% long-term rate if your taxable income falls below the threshold.

Use the IRS Section 1031 exchange for real estate: A like-kind exchange allows real estate investors to defer capital gains tax indefinitely by rolling proceeds into a new qualifying property. Strict timelines apply — 45 days to identify and 180 days to close.

Donate appreciated assets to charity: Instead of selling a stock with a large embedded gain, consider donating it directly to a qualified charity. You get a deduction for the full fair market value and avoid paying capital gains tax on the appreciation entirely.

Consider Opportunity Zone investments: Investing capital gains into a Qualified Opportunity Fund (QOF) can defer and potentially reduce the original gain while excluding future appreciation in the fund from taxation after a 10-year hold.

Track basis meticulously for crypto: With expanded IRS enforcement in 2026, digital asset transactions must be tracked trade-by-trade. Using specific identification (SPEC ID) for cost basis can produce significantly better tax outcomes than FIFO.

For personalized capital gains planning tailored to content creators and self-employed professionals, visit Tranzesta.com and explore our full suite of tax services.

Conclusion: Take Control of Your Capital Gains Tax in 2026

Understanding capital gains tax in 2026 is not just about knowing the rates — it is about using that knowledge to make better financial decisions throughout the year. Three key takeaways from this guide: first, the difference between short-term and long-term capital gains rates is enormous, often ranging from 10% to 37% versus 0% to 20%. Second, timing, basis tracking, and strategic account placement are the most powerful tools you have. Third, overlooking state taxes, the NIIT, and crypto reporting are the most common and costly mistakes US taxpayers make.

Whether you are investing profits from a content creation business, managing real estate equity, or planning the sale of a cannabis operation, Tranzesta.com has the expertise to help you navigate every dimension of capital gains tax law in the United States.

Ready to get expert help with your capital gains tax strategy? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

. For US taxpayers, choosing the right holding period is one of the most impactful ways to reduce tax liability on investment profits.

For 2026, the long-term capital gains tax rates for US taxpayers are 0%, 15%, and 20%, depending on taxable income. Single filers with taxable income up to approximately $47,025 pay 0%. Those earning between $47,026 and $518,900 pay 15%.

There are several legal strategies US taxpayers use to reduce capital gains tax. Holding assets for more than one year qualifies gains for lower long-term rates. Investing through tax-advantaged accounts like IRAs or 401(k)s shelters gains entirely. Tax-loss harvesting offsets gains with losses. A Section 1031 exchange defers gains on real estate. Donating appreciated assets to charity eliminates the gain and provides a deduction. Each strategy has specific rules, so consulting a qualified tax professional like the team at Tranzesta is essential.

Yes. The IRS treats cryptocurrency as property, not currency, meaning every taxable event — including selling, trading, or using crypto to pay for goods — triggers a capital gain or loss. Long-term gains held over one year qualify for the 0%, 15%, or 20% preferential rates. In 2026, expanded broker reporting requirements make accurate crypto record-keeping more important than ever for US taxpayers.

The Net Investment Income Tax (NIIT) is a 3.8% surtax that applies to investment income — including capital gains — for US taxpayers whose modified adjusted gross income (MAGI) exceeds $200,000 for single filers or $250,000 for married filing jointly. It applies to both short-term and long-term capital gains. This tax frequently surprises self-employed individuals and high-income professionals who do not anticipate it.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation