Most people assume hemp and marijuana are taxed

the same way — they are not. The hemp vs marijuana tax treatment difference is one of the most consequential distinctions in US cannabis law, and getting it wrong can cost your business tens of thousands of dollars in unexpected taxes, penalties, or denied deductions. Hemp became federally legal with the passage of the 2018 Farm Bill. Marijuana remains a Schedule I controlled substance under federal law. That single legal distinction creates an entirely different tax reality for producers, manufacturers, and retailers on both sides of the line.

In this guide, you will learn exactly how the IRS and state tax authorities treat hemp and marijuana differently, which federal tax codes apply to each, the most common mistakes operators make when classifying their products, and a practical action plan to ensure your business is on the right side of both. You will also discover how Tranzesta’s cannabis accounting team helps hemp and marijuana businesses across the United States develop accurate and compliant tax strategies.

What Is the Hemp vs Marijuana Tax Treatment Difference?

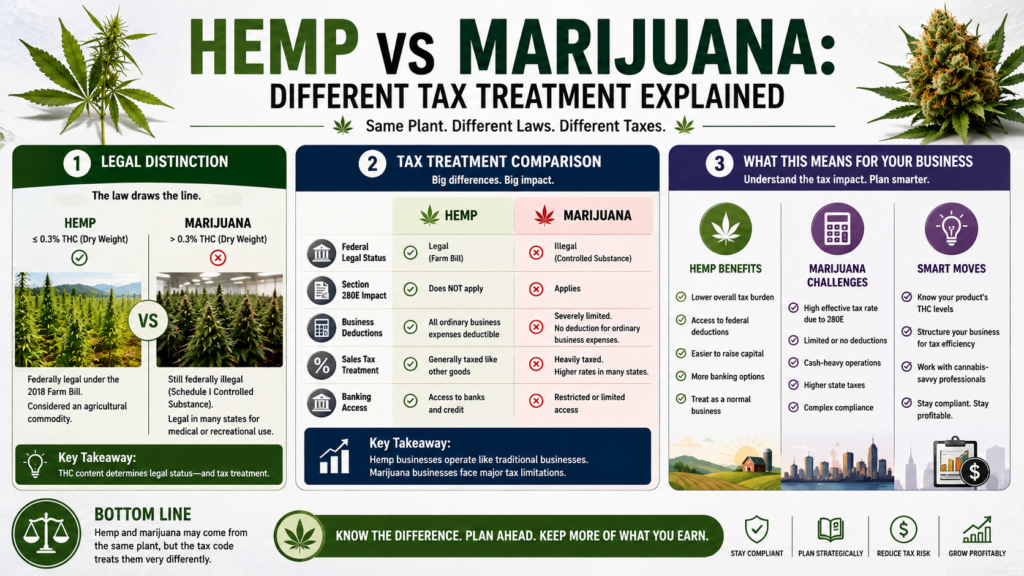

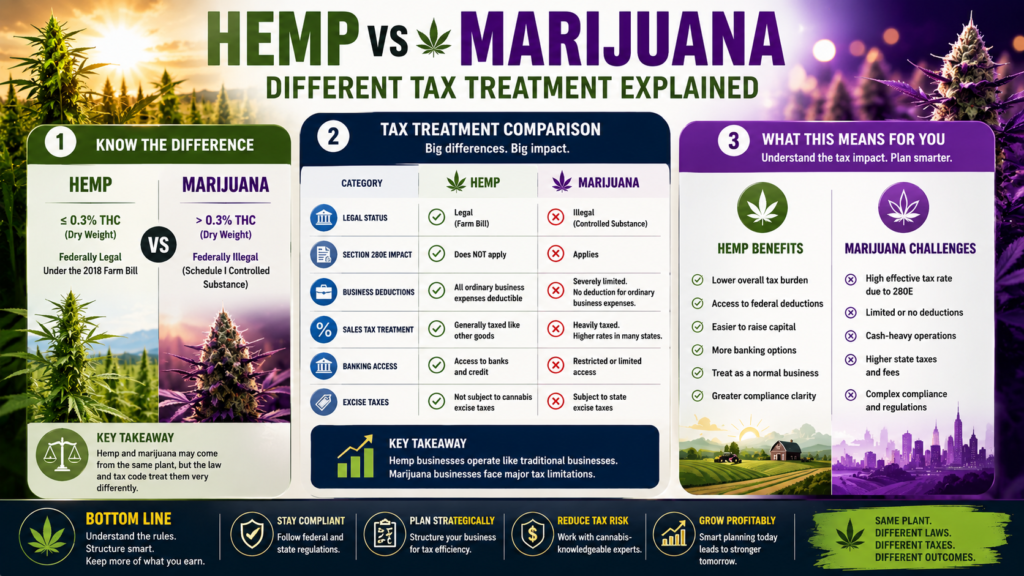

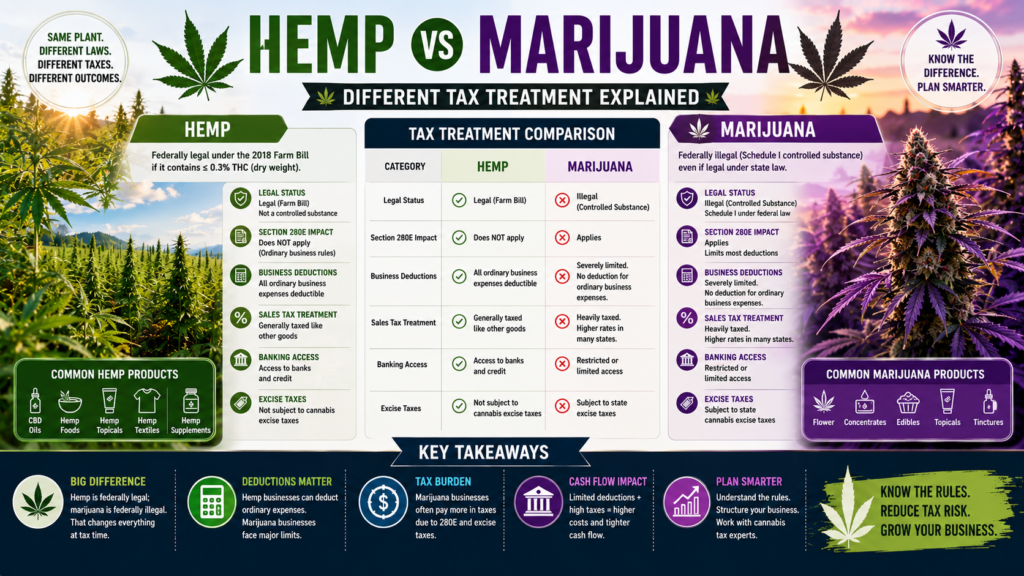

The hemp vs marijuana tax treatment difference refers to the distinct set of federal and state tax rules that apply to each plant based on its legal classification. Hemp and marijuana are both Cannabis sativa plants, but federal law treats them completely differently based on their THC (tetrahydrocannabinol) content. THC is the primary psychoactive compound in cannabis.

Under the Agriculture Improvement Act of 2018 — commonly called the 2018 Farm Bill — hemp is defined as cannabis containing no more than 0.3% THC on a dry-weight basis. Hemp and hemp-derived products, including CBD (cannabidiol), are federally legal agricultural commodities. Marijuana, by contrast, is cannabis containing more than 0.3% THC and remains classified as a Schedule I controlled substance under the Controlled Substances Act. This federal classification triggers IRC Section 280E (Internal Revenue Code Section 280E), which denies standard business deductions to marijuana businesses. Hemp businesses face no such restriction.

Why Does This Distinction Matter to Cannabis Business Owners?

The tax gap between hemp and marijuana operators is substantial. A hemp farmer, CBD manufacturer, or hemp extract retailer can deduct all ordinary business expenses — rent, wages, marketing, insurance, professional fees — just like any other US business. In contrast, a marijuana dispensary, cultivator, or infused product manufacturer operating under a state cannabis license cannot deduct any of those expenses at the federal level. As a result, marijuana businesses often pay an effective federal income tax rate of 60% to 80% of net revenue, compared to the standard 21% corporate rate or personal rate that hemp businesses pay.

Does the 0.3% THC Line Always Determine Classification?

The 0.3% THC threshold is the legal dividing line, but it creates compliance complexity for operators on both sides. A hemp crop that tests above 0.3% THC at harvest is legally reclassified as marijuana under federal law — even if the farmer planted compliant seeds. Similarly, a hemp-derived extract that is concentrated during processing can inadvertently exceed the THC threshold in its final form, potentially reclassifying the product. Therefore, testing, documentation, and product formulation controls are critical for any business that relies on hemp’s favorable tax treatment.

How Does Federal Tax Law Treat Hemp and Marijuana Differently?

Federal tax law creates a stark divide between hemp and marijuana businesses. Understanding each rule is essential to grasping the full hemp vs marijuana tax treatment difference.

Section 280E: The Core Tax Burden on Marijuana Businesses

IRC Section 280E, enacted in 1982, prohibits businesses engaged in trafficking Schedule I or II controlled substances from deducting any expenses except Cost of Goods Sold (COGS). COGS is the direct cost of acquiring or producing inventory — such as seeds, soil inputs, packaging, and direct production labor. All other operating costs — employee wages in non-production roles, rent for retail or office space, utilities, marketing, accounting fees, and management costs — are non-deductible for marijuana businesses at the federal level.

Hemp businesses are entirely exempt from Section 280E.

Because hemp is a federally legal agricultural commodity, hemp operators file taxes like any other US business and deduct all legitimate business expenses under standard IRC rules. The difference in deductible expenses between a hemp business and a marijuana business with identical revenue and costs can easily amount to hundreds of thousands of dollars per year in additional federal tax liability.

Self-Employment and Pass-Through Taxation

For sole proprietors and pass-through entities (LLCs and S corporations), hemp income is subject to standard self-employment tax rules. Net self-employment income is taxed at 15.3% for the first $168,600 (2024 threshold, adjusted annually) plus 2.9% on amounts above that threshold. Marijuana operators with pass-through entities face the same self-employment tax rates, but their taxable income is dramatically higher because 280E prevents them from deducting operating expenses. As a result, a marijuana dispensary owner may owe self-employment tax on gross profit rather than true net profit.

The R&D Tax Credit and Hemp Businesses

Hemp businesses may qualify for the federal Research and Development (R&D) Tax Credit under IRC Section 41 when they conduct qualifying research activities — such as developing new cultivars, improving extraction processes, or creating novel hemp-derived compounds. Marijuana businesses, by contrast, cannot claim the R&D credit because Section 280E disallows it along with all other non-COGS deductions. This creates yet another area where the hemp vs marijuana tax treatment difference produces a significant financial advantage for hemp operators.

Hemp: all business deductions available — rent, wages, marketing, professional fees

Marijuana: only COGS deductible under Section 280E at the federal level

Hemp: eligible for R&D Tax Credit (IRC Section 41)

Marijuana: R&D credit unavailable due to 280E restrictions

Hemp: standard effective federal tax rate (21% corporate or personal rates)

Marijuana: effective federal tax rate often 60–80% of gross profit

How Do State Taxes Treat Hemp and Marijuana Differently?

At the state level, the hemp vs marijuana tax treatment difference is equally significant, though the rules vary widely across US jurisdictions. Most states follow the federal hemp-marijuana distinction but apply their own cannabis excise taxes, sales tax rules, and income tax regulations on top of federal law.

State Cannabis Excise Taxes Apply Only to Marijuana

Every US state that has legalized adult-use or medical marijuana imposes a cannabis-specific excise tax on marijuana sales. These excise taxes do not apply to hemp or hemp-derived products sold outside the state cannabis licensing system. For example, California imposes a 15% cannabis excise tax on all marijuana sales at the retail level. Colorado imposes a 15% retail marijuana sales tax. Washington state imposes a 37% cannabis excise tax — the highest in the USA. None of these rates applies to products in IL channels.

Sales Tax Treatment: Food Exemptions and Hemp CBD Products

Many US states exempt food and dietary supplements from sales tax. Hemp-derived CBD products sold as dietary supplements — capsules, tinctures, and gummies not containing THC above the federal threshold — may qualify for food or supplement exemptions in some jurisdictions. In contrast, marijuana-infused edibles are universally excluded from food tax exemptions in every state that has legalized cannabis. Tranzesta.com Additionally, some states apply their own income tax versions of Section 280E, while others, including California and Colorado, have explicitly decoupled from the federal provision and allow full state-level deductions for marijuana businesses.

Common Mistakes Businesses Make With Hemp and Marijuana Tax Treatment

These errors regularly result in IRS audits, back-tax assessments, and overpayments. Avoiding them is critical for any hemp or marijuana operator in the United States.

Mistake 1: Treating Hemp-Derived CBD Products as Marijuana for Tax Purposes

Some operators — particularly those who produce both hemp and marijuana products — apply cannabis excise tax rates and 280E restrictions to their hemp product lines out of caution or confusion. This is unnecessary and costly. Hemp products sold outside the state cannabis licensing system are not subject to cannabis excise taxes and are not restricted by 280E. Misapplying these means and deducting the empiricale empiricale empirical side of the results, resulting in requiring stakeakeake 2: Claiming Hemp Status for Products That Exceed the 0.3% THC Threshold

The opposite error is equally dangerous. Some operators attempt to classify THC-infused marijuana products as hemp to avoid excise taxes and 280E. State regulatory agencies and the IRS use laboratory testing data and seed-to-sale tracking systems to verify product THC content. Products that test above 0.3% THC are legally marijuana, regardless of how they are labeled or marketed. Misclassifying marijuana products as hemp constitutes tax fraud and exposes operators to civil penalties of up to 75% of the underpayment and potential criminal prosecution.

Mistake 3: Failing to Separate Hemp and Marijuana Operations in Accounting Records

Businesses that operate both hemp and marijuana product lines must maintain completely separate accounting records, bank accounts, and entity structures for each. Commingling revenues and expenses between hemp and marijuana operations creates ambiguity about which 280E restrictions apply, which deductions are available, and which tax rates govern each revenue stream. The IRS may apply the more restrictive marijuana rules to the entire commingled operation if records are not clearly separated.

Mistake 4: Ignoring State Decoupling from Section 280E

Several US states have decoupled their state income tax from Section 280E, allowing marijuana businesses to claim full operating deductions on their state tax returns even though those same deductions are denied at the federal level. California, Colorado, New Mexico, and several other states have taken this position. Marijuana operators who fail to claim these state-level deductions leave significant tax savings on the table every year. Working with a cannabis-specialized firm like Tranzesta ensures you capture every available state deduction.

How to Apply the Hemp vs Marijuana Tax Treatment Difference in Your Business

These steps help hemp and marijuana operators build an accurate, compliant tax structure based on their specific product lines and operations.

Step 1: Confirm the Federal Legal Status of Every Product.

Test every product SKU for THC content and maintain current COA (Certificate of Analysis) records from a DEA-registered or state-approved laboratory. Products at or below 0.3% THC qualify as hemp. Products above 0.3% THC are marijuana. Organize your product catalog into clearly labeled hemp and marijuana categories and update this classification whenever formulas or inputs change.

Step 2: Establish Separate Legal Entities for Hemp and Marijuana Operations.

If you operate both hemp and marijuana product lines, form separate legal entities — typically separate LLCs — for each. Separate entities ensure clean separation of revenues, expenses, and tax obligations. This structure also protects the hemp entity’s favorable tax treatment from being contaminated by the marijuana entity’s 280E restrictions.

Step 3: Set Up Separate Accounting Systems and Bank Accounts.

Maintain independent bookkeeping records, QuickBooks files (or equivalent), and bank accounts for each entity. Every transaction must be coded to the correct entity and expense category. For the marijuana entity, configure your chart of accounts to separate COGS-eligible costs from non-deductible operating expenses in compliance with Section 280E.

Step 4: Determine Which State-Level Deductions

Are Available for Your Marijuana Operation. Research whether each state where your marijuana business operates has decoupled from federal Section 280E. In states that have decoupled — such as California and Colorado — claim full operating deductions on your state returns even though they are denied federally. This requires careful state return preparation that differs from your federal filing.

Step 5: Apply the Correct Sales Tax and Excise Tax Rates for Each Product Line.

Confirm that your POS and accounting systems apply cannabis excise taxes only to marijuana products. Hemp products sold in general retail channels are not subject to cannabis excise taxes. Verify sales tax treatment for each product category and jurisdiction separately, since food and supplement exemptions may apply to certain hemp products.

Step 6: Document Your Classification Decisions in Writing.

For each product, document your THC testing results, the legal basis for your hemp or marijuana classification, and the tax rules you are applying as a result. Update this documentation whenever products change. Written contemporaneous records are your primary defense in an IRS or state audit of your product classifications.

How Tranzesta Helps Hemp and Marijuana Businesses Navigate Tax Differences

Tranzesta is a US-based tax consultation firm specializing in cannabis industry accounting, including the complex hemp vs marijuana tax treatment difference. Tranzesta.com Our team works with hemp farmers, CBD manufacturers, marijuana dispensaries, multi-state operators, and vertically integrated cannabis companies across the United States to build accurate, defensible tax strategies for both plant types.

When you work with Tranzesta, we begin by reviewing your current product catalog, legal entity structure, and existing accounting systems. We identify whether your operations correctly separate hemp and marijuana tax treatments, hemp vs marijuana tax treatment difference

flag any deductions you may be missing on either side, and build a tax position that minimizes your exposure at both the federal and state levels.

Tranzesta’s services for hemp and cannabis businesses include:

280E compliance reviews and COGS maximization, hemp vs. marijuana entity separation and restructuring, state income tax analysis including 280E decoupling, sales and excise tax classification, and full-service bookkeeping for licensed cannabis and hemp businesses in the USA. Learn more about cannabis accounting and tax compliance at Tranzesta.com.

Need help navigating the hemp vs marijuana tax treatment difference?

Contact our cannabis tax team at hello@tranzesta.com for a free consultation.

Visit Tranzesta.com to learn more about our cannabis and hemp accounting services.

Hemp vs Marijuana Tax Treatment Difference: Expert Tips for 2026

Beyond the core rules, experienced cannabis tax professionals apply these advanced strategies to maximize the tax advantages on both sides of the hemp-marijuana line.

Monitor the ling Developments Actively.

The DEA’s ongoing review of marijuana’s Schedule I classification — with a potential move to Schedule III — could eliminate or significantly reduce Section 280E’s reach for marijuana businesses. A Schedule III reclassification would fundamentally close the hemp vs marijuana tax treatment difference at the federal level. Work with a cannabis tax specialist to model how reclassification would affect your tax position and prepare for the transition.

Use Cost Segregation Studies for Both Hemp and Marijuana Facilities.

Hemp businesses can accelerate depreciation on facility improvements and equipment using cost segregation studies — a tax strategy unavailable to marijuana businesses in most cases because 280E prevents depreciation deductions beyond COGS. If you operate both entity types, maximize depreciation on the hemp side of the business.

Explore the QBI Deduction for Hemp Pass-Through Entities.

Hemp businesses structured as pass-through entities (LLCcorporationstc.e (QBI) deduction under IRC Section 199A, which allows eligible business owners to deduct up to 20% of qualified business income. Marijuana businesses generally cannot claim this deduction due to 280E. This is a substantial advantage for hemp operators that is frequently overlooked.

Review Your Hemp Products for R&D Credit Eligibility Annually.

If you develop new hemp cultivars, improve extraction methods, or create novel hemp-based formulations, document the research activity and associated costs throughout the year. The R&D Tax Credit can offset federal income tax dollar-for-dollar — a powerful benefit that hemp operators often miss because they are not aware of their eligibility.

Stay Current on State Hemp Regulation Changes.

State hemp regulations and associated tax rules change frequently as states update their hemp programs in response to federal guidance. Some states have imposed their own THC thresholds more restrictive than the federal 0.3% standard. Working with a cannabis and hemp tax specialist like Tranzesta ensures you catch regulatory changes before they create compliance gaps.

Conclusion: The Hemp vs Marijuana Tax Gap Is Real — and Manageable

The hemp vs marijuana tax treatment difference creates a significant financial divide between two businesses that may be growing nearly identical plants. The three most important takeaways from this guide are: first, hemp businesses enjoy full federal deductibility while marijuana businesses are restricted by Section 280E to deducting only Cost of Goods Sold; second, state-level tax treatment adds another layer of complexity, with cannabis excise taxes applying only to marijuana and some states decoupling from 280E entirely; and third, accurate product classification, separate legal entities, and clean accounting records are essential to protecting the favorable tax treatment on each side.

Both hemp and marijuana tax laws continue in these states states statesee, particularly as federal rescheduling discussions progress and more states refine their cannabis and hemp programs. Proactive planning with a qualified cannabis and hemp tax specialist is the most reliable way to stay compliant and minimize your tax burden on both sides of the line.

Ready to get expert help with hemp and marijuana tax treatment?

Email us at hello@tranzesta.com or visit Tranzesta.com

to schedule your free tax strategy session today.

FAQs

Section 280E of the Internal Revenue Code applies only to businesses Controlled Substances Act by defining it as cannabis with no more than 0.3% THC on a dry-weight basis, hemp businesses are federally legal agricultural operations. They can deduct all ordinary business expenses — including rent, wages, marketing, and professional fees — just like any other US business. Only marijuana businesses, operating under state cannabis licenses, remain subject to 280E.

including the R&D Tax Credit and the Qualified Business Income deduction — that are unavailable to marijuana operators due to 280E. As a result, the effective federal income tax rate for a marijuana business is often two to four times higher than for a hemp business with identical revenue and operating costs.

Hemp-derived CBD products sold in general retail channels such as health food stores, pharmacies, and e-commerce platforms are not subject to cannabis excise taxes in most US states. However, hemp CBD products remain subject to standard sales tax, and food or supplement exemptions vary by state.

and crops that exceed the THC threshold cannot be sold as hemp. From a tax perspective, the loss of the crop may be deductible as a business loss for the hemp operator. However, if a producer knowingly sells a crop that exceeds the threshold as hemp, they face potential criminal charges and significant penalties, as the product legally constitutes an illegal marijuana crop.

revenues and expenses can result in the IRS applying Section 280E restrictions to the entire combined operation. Most cannabis tax specialists, including Tranzesta, recommend forming separate LLCs for each product line to protect the favorable tax treatment of the hemp entity.

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation