One of the most valuable tax breaks for American business

owners is shrinking — fast. The bonus depreciation rules 2026 allow US businesses to immediately deduct 60% of the cost of qualifying assets in the year they are placed in service. That is still a significant write-off, but it is down from the 100% that was available just a few years ago. If you are not planning around this phase-down right now, you are leaving real money on the table.

In this guide, you will learn exactly how bonus

depreciation works in 2026, what property qualifies, which mistakes to avoid, and how to combine this deduction with Section 179 for maximum tax savings. Whether you are a content creator, a cannabis business owner, or a self-employed entrepreneur, this is one tax rule you cannot afford to ignore.

What Are the Bonus Depreciation Rules 2026?

Bonus depreciation — formally known as the additional first-year depreciation deduction under Internal Revenue Code Section 168(k) — allows businesses to immediately expense a large percentage of the cost of qualifying assets in the year they are purchased and placed in service, rather than depreciating them gradually over years.

For the 2026 tax year, the bonus depreciation rate

is 60%. This is part of a scheduled phase-down that Congress built into the Tax Cuts and Jobs Act (TCJA) of 2017. The TCJA introduced 100% bonus depreciation starting in 2017, but the law set a step-down schedule that reduces the rate by 20 percentage points each year beginning in 2023.

This matters enormously for US taxpayers who make

significant equipment or asset purchases. The difference between deducting 60% now versus spreading a deduction over five or seven years is a substantial cash flow and tax savings advantage. Additionally, unlike Section 179, bonus depreciation can create or increase a net operating loss — which can then be carried forward to offset future income.

The TCJA Phase-Down Schedule

Here is how the bonus depreciation rate has declined and will continue to decline under current law:

Wait — current law as written actually sets 2026 at 20%, not 60%.

However, tax legislation moves fast. As of the time of this writing, there is active congressional discussion about extending or restoring higher bonus depreciation rates, including potential retroactive changes. Always confirm the current rate with a qualified tax advisor before filing. The key point is that the window for high-rate bonus depreciation is narrowing, and acting sooner delivers more value.

Who Can Claim Bonus Depreciation?

Any US business — sole proprietor, partnership, LLC, S-Corp, or C-Corp — can claim bonus depreciation on qualifying property. There is no dollar cap and no business income limitation, which distinguishes it from the Section 179 deduction. However, bonus depreciation applies to new and used property that meets specific IRS criteria, which we cover in the next section.

What Property Qualifies Under the Bonus Depreciation Rules 2026?

Bonus depreciation applies to qualifying property — a specific IRS term meaning property that meets four core requirements.

The Four Requirements for Qualifying Property

According to IRS guidance, bonus depreciation eligible property must meet all of the following:

The property has a MACRS (Modified Accelerated Cost Recovery System) recovery period of 20 years or less. This covers most tangible personal property including machinery, equipment, computers, furniture, and certain vehicles.

The property is depreciable computer software.

The property is qualified film, television, or live theatrical production.

The property has not been previously used by the taxpayer or a predecessor.

The original use requirement was relaxed by the TCJA — used property now qualifies for bonus depreciation as long as the taxpayer has not previously used it. This was a major expansion of the rule.

Industry-Specific Examples

For OnlyFans creators and digital content producers in the United States, qualifying property can include cameras, lighting equipment, audio gear, editing computers, studio furniture, and specialized software. For cannabis businesses, qualifying assets commonly include extraction equipment, packaging machinery, point-of-sale systems, and security infrastructure. Contractors and manufacturers can apply bonus depreciation to heavy machinery, tools, and specialized vehicles meeting weight criteria.

Importantly, real property — land and buildings

— does not qualify for bonus depreciation. However, qualified improvement property (QIP), which covers certain leasehold improvements to the interior of nonresidential buildings, does qualify under current IRS rules.

Common Mistakes to Avoid With Bonus Depreciation in 2026

Even experienced business owners make costly errors when applying bonus depreciation. Avoiding these pitfalls protects your deduction and keeps your return audit-ready.

Mistake 1: Assuming Bonus Depreciation Is Automatic

Bonus depreciation is generally applied automatically, but you can elect out of it on a class-by-class basis. Many business owners do not realize they have a choice, and in some situations — particularly when state tax conformity is a concern — electing out of bonus depreciation for certain asset classes is actually the smarter strategy. Therefore, review this election carefully with a tax professional before filing.

Mistake 2: Ignoring State Tax Conformity Issues

This is one of the most expensive surprises in business taxation. Many US states do not conform to the federal bonus depreciation rules. States like California, for example, have historically decoupled from federal bonus depreciation, meaning your federal deduction does not reduce your California taxable income by the same amount. As a result, business owners in non-conforming states face a higher state tax bill than they expect.

Mistake 3: Confusing Bonus Depreciation with Section 179

Both rules accelerate deductions, but they work differently. Section 179 is capped at $1,220,000 (2026), cannot create a loss, and must be elected. Bonus depreciation has no dollar cap, can create a net operating loss, and applies automatically. Most businesses benefit from using Section 179 first, then layering bonus depreciation on top for remaining eligible property.

Mistake 4: Missing the Placed-In-Service Requirement

Bonus depreciation applies to property placed in service — meaning actively put into business use — during the tax year. Purchasing equipment in late 2026 that is not set up and operational until January 2027 disqualifies it from the 2026 bonus depreciation rate. With rates scheduled to drop, this timing mistake could cost a significant portion of the deduction.

Mistake 5: Forgetting Depreciation Recapture

If you sell or stop using property for business purposes before the end of its recovery period, the IRS requires recapture of accelerated depreciation as ordinary income. This applies to bonus depreciation just as it does to Section 179. Factor recapture risk into any equipment purchase decision, especially for assets you may sell or repurpose within a few years.

How to Apply Bonus Depreciation: A Step-by-Step Guide for 2026

Applying bonus depreciation correctly requires preparation and coordination with your overall tax strategy. Follow these steps to maximize the deduction.

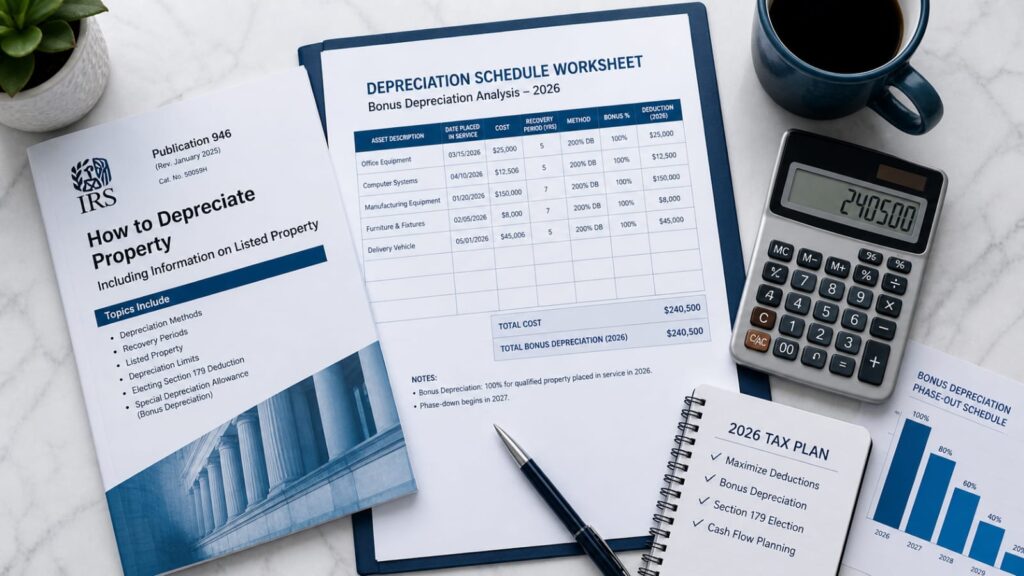

Step 1: Identify All Qualifying Assets Placed in Service in 2026

Start by reviewing every asset your business purchased and placed in service during the 2026 tax year. Separate tangible personal property (equipment, machinery, technology) from real property (buildings, land). Bonus depreciation applies only to the first category and qualifying improvement property.

Step 2: Confirm the MACRS Recovery Period for Each Asset

Look up or confirm the correct MACRS recovery period for each asset class. Five-year property includes computers, automobiles, and certain manufacturing equipment. Seven-year property covers most office furniture and fixtures. Assets with a 20-year or shorter recovery period qualify for bonus depreciation. Your tax advisor can confirm classification for unusual or industry-specific assets.

Step 3: Apply Section 179 First

Before applying bonus depreciation, determine how much Section 179 you want to claim. Section 179 gives you precise control over which assets you expense and in what amounts. After you have applied Section 179 up to your desired limit (capped at $1,220,000 and net income), bonus depreciation applies to the remaining adjusted basis of qualifying property automatically.

Step 4: Calculate Your Bonus Depreciation Deduction

Multiply the remaining depreciable basis of each qualifying asset by the applicable bonus depreciation rate — currently scheduled at 20% for 2026 under existing law (confirm the current rate with your tax advisor, as legislation may have changed this). The resulting amount is your additional first-year deduction for that asset.

Step 5: Evaluate State-Level Impact

Before finalizing your deduction, check whether your state conforms to federal bonus depreciation rules. In non-conforming states, you may need to make a state-specific adjustment or addback on your state return. This step often surprises business owners and significantly affects net tax savings. Review state conformity with a tax professional familiar with your specific state.

Step 6: Complete Form 4562

Both Section 179 and bonus depreciation are reported on IRS Form 4562 — Depreciation and Amortization. Your tax preparer will complete this form as part of your business return. Part II of Form 4562 specifically covers the special depreciation allowance (bonus depreciation). Ensure this form is filed accurately and attached to your return.

Step 7: Document Everything and Plan Forward

Keep complete records of each asset: purchase date, purchase price, invoice, financing agreement if applicable, and date placed in service. Additionally, model your 2027 tax year now. With bonus depreciation dropping further, 2026 may be your last year at a meaningful rate under current law — unless Congress acts. Planning forward is where the biggest savings live.

How Tranzesta Helps US Businesses Navigate Bonus Depreciation Rules in 2026

At Tranzesta, we specialize in helping American business owners understand, plan for, and execute complex tax strategies — including bonus depreciation and Section 179 — in ways that are legally aggressive and fully compliant.

Our clients include OnlyFans and digital content creators

who need clarity on which equipment purchases qualify for immediate deductions. We also serve cannabis businesses, which face the added complexity of IRC Section 280E restrictions alongside depreciation rules. Additionally, we work with self-employed professionals, contractors, and small business owners across the United States who want to make asset-buying decisions with tax strategy built in from the start.

Tranzesta does not take a one-size-fits-all approach.

We analyze your specific income level, asset mix, state of domicile, and multi-year tax position to determine the optimal combination of Section 179 and bonus depreciation for your situation. We also prepare and file Form 4562 accurately, coordinate state conformity adjustments, and build forward-looking depreciation models so you always know what is coming.

Most importantly, we keep your documentation audit-ready. Every deduction we recommend comes with a documentation protocol that protects you if the IRS reviews your return.

Visit Tranzesta.com to learn more about our business tax

and bookkeeping services. You can also explore our content creator tax services at Tranzesta.com to see how we help digital entrepreneurs maximize every available deduction.

Contact our team at hello@tranzesta.com for a free consultation.

Bonus Depreciation Rules 2026: Expert Tips to Maximize Your Deduction

The following strategies go beyond the basics and reflect how experienced tax advisors approach bonus depreciation for high-growth businesses.

Act before year-end on any planned asset purchases. With the rate declining each year under current law, delaying a planned equipment purchase from 2026 to 2027 reduces your bonus depreciation rate. If the purchase makes business sense now, accelerating it into 2026 locks in the higher rate.

Layer Section 179 and bonus depreciation strategically.

Use Section 179 for assets you specifically want to fully expense, especially when your income is high enough to absorb the deduction. Then apply bonus depreciation to the remaining basis on other qualifying assets. The combination often produces a larger total deduction than using either alone.

Track bonus depreciation separately for each asset. Do not lump all assets together. Separate tracking lets you optimize the election-out strategy for specific asset classes in states with non-conformity, potentially saving significant state taxes.

Model a net operating loss scenario. Unlike Section 179, bonus depreciation can push your business into a net operating loss (NOL). An NOL can be carried forward to offset future taxable income. In some situations, creating an NOL intentionally — by timing a large asset purchase — is a legitimate multi-year strategy worth modeling.

Monitor congressional activity. Lawmakers have repeatedly discussed extending or restoring 100% bonus depreciation. If legislation passes retroactively, your 2026 return may be amendable to reflect a higher rate. Stay connected with a tax professional who tracks legislative developments actively.

For official IRS guidance, review IRS Publication 946 – How to Depreciate Property at https://www.irs.gov/publications/p946 (opens in new tab), which is the definitive resource on bonus depreciation and MACRS rules.

Learn more about strategic tax planning for your industry at Tranzesta.com, where our experts break down depreciation strategies specific to content creators, cannabis businesses, and self-employed professionals.

Conclusion

The bonus depreciation rules 2026 still offer a meaningful tax advantage for American business owners — but the window is narrowing. Here are the three most important takeaways:

First, bonus depreciation in 2026 is scheduled at 20% under current law, down from 100% in 2022 — though legislative changes may alter this rate, so always confirm before filing. Second, no dollar cap and no income limitation make bonus depreciation a powerful complement to Section 179, especially for businesses with significant asset purchases or potential net operating losses. Third, state conformity issues, timing requirements, and recapture rules create real complexity — and real risk — for businesses that go it alone.

Planning ahead and working with an expert makes the difference between leaving money on the table and keeping it in your business where it belongs.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

The bonus depreciation rate for 2026 is scheduled at 20% under the Tax Cuts and Jobs Act phase-down schedule, which reduces the rate by 20 percentage points each year starting in 2023 after 100% was available in 2022. However, US lawmakers have discussed restoring or extending higher rates, so the final 2026 rate may change depending on legislation. Business owners should confirm the current applicable rate with a qualified tax professional before filing their 2026 return.

Bonus depreciation can create or increase a net operating loss (NOL) for US taxpayers, which is one of its key advantages over Section 179. Unlike the Section 179 deduction, which cannot exceed net business income, bonus depreciation has no income limitation. A resulting NOL can generally be carried forward indefinitely to offset future taxable income, making bonus depreciation a valuable multi-year tax planning tool for businesses with significant asset purchases.

Section 179 and bonus depreciation are both accelerated depreciation tools, but they differ in important ways. Section 179 is taxpayer-elected, capped at $1,220,000 in 2026, and cannot create a net operating loss. Bonus depreciation applies automatically, has no dollar cap, and can produce a loss. Most US tax advisors recommend applying Section 179 first on selected assets, then using bonus depreciation on remaining qualifying property to maximize the overall deduction in the same tax year.

Yes. Since the Tax Cuts and Jobs Act of 2017, bonus depreciation applies to both new and used property in the United States, provided the taxpayer or any predecessor has not previously used the asset. This was a significant expansion of the original rule, which applied only to new property. As a result, purchasing used equipment — such as second-hand manufacturing machinery, cameras, or computers — can still qualify for the bonus depreciation deduction if all other IRS requirements are met.

Under current law, bonus depreciation is scheduled to drop to 0% after 2026, effectively eliminating the deduction in 2027 unless Congress acts. However, there has been bipartisan support in the United States for extending or restoring 100% bonus depreciation as part of broader tax legislation. Business owners should not assume the deduction disappears permanently — but they also should not count on an extension. The safest approach is to accelerate qualifying asset purchases while a rate still applies and monitor legislative developments closely.