Most US business owners can name sales tax

but fewer than half understand use tax, and that gap costs them dearly during audits. Understanding the use tax and sales tax is one of the most overlooked compliance obligations in American business today. These two taxes are closely related, often complementary, and enforced by the same state revenue departments — yet most businesses only comply with one of them.

The IRS and state tax agencies collected

over $500 billion in sales and use taxes across the United States in 2023 alone. Despite that scale, use tax remains the single most under-reported tax on business returns — particularly for ecommerce businesses, cannabis operators, and self-employed individuals who purchase goods and services across state lines.

In this guide, you will learn exactly what sales tax

and use tax are, how they differ, when each applies to your business, the most common mistakes businesses make, and how Tranzesta helps US taxpayers get both taxes right. Let’s start with the definitions.

What Is the Use Tax vs Sales Tax Difference? A Clear Definition

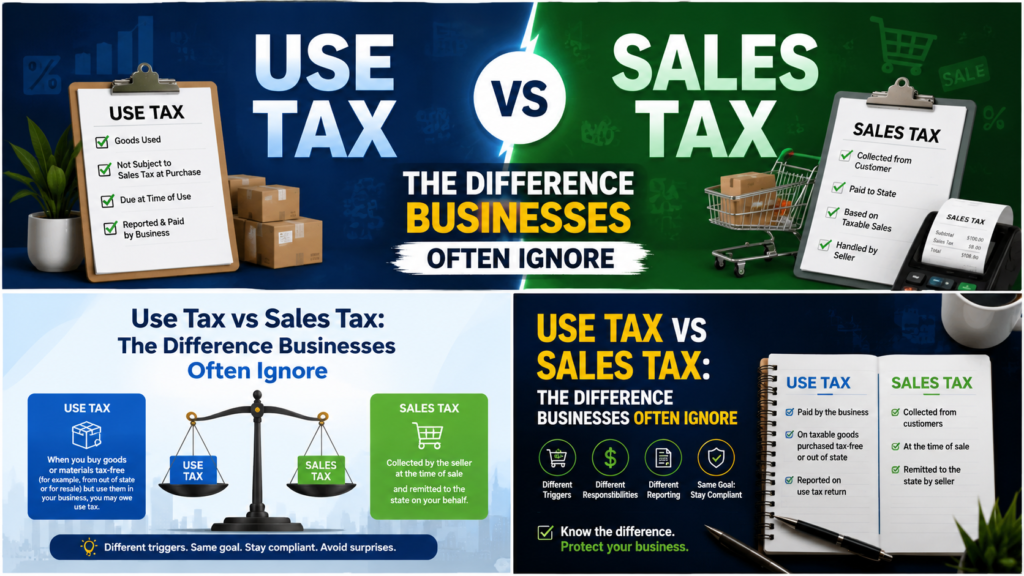

The use tax vs sales tax difference comes down to who collects the tax and under what circumstances. Sales tax is collected by the seller at the point of sale and remitted to the state. Use tax is self-assessed and paid directly by the buyer when they purchase taxable goods or services without paying sales tax at the time of purchase.

In practical terms: when you buy office supplies from a local store in Texas, the store charges you Texas sales tax. However, when you order those same supplies from an out-of-state vendor who does not charge Texas sales tax, you owe Texas use tax on that purchase — and you must report and pay it yourself.

Both taxes exist to ensure that all taxable purchases

made by residents and businesses in a state are ultimately taxed at the same rate, regardless of where the purchase was made. They are, in effect, two sides of the same coin. Most importantly, they apply to the same types of goods and at the same tax rate — the critical difference is simply who is responsible for payment.

What Is Sales Tax?

Sales tax is a state-imposed consumption tax — meaning a tax on spending — charged at the point of sale when a taxable product or service is sold within a state. In the United States, 45 states and Washington D.C. impose a statewide sales tax. The seller collects the tax from the buyer and remits it to the state revenue department, usually on a monthly, quarterly, or annual basis depending on volume.

Sales tax rates vary widely by state. For example,

California’s base rate is 7.25%, while Tennessee’s is 7.0%, and Colorado’s is 2.9% — though local county and city taxes stack on top of each state rate, pushing some total rates above 10%. Sellers must register for a sales tax permit before legally collecting sales tax in any state.

What Is Use Tax?

Use tax is a complementary tax imposed on the storage, use, or consumption of taxable goods or services in a state when sales tax was not collected at the point of purchase. Use tax is not new — it has existed in most US states since the 1930s, originally designed to prevent consumers from crossing state lines to avoid sales tax.

Today, use tax primarily applies to online purchases,

out-of-state vendor purchases, items brought into a state from another state, and goods purchased for resale that are later removed from inventory for personal or business use. The buyer — not the seller — is legally responsible for reporting and remitting use tax directly to the state.

Key Rules and Requirements: How Use Tax and Sales Tax Work in the USA

Both sales tax and use tax are governed at the state level — not the federal level. There is no federal sales tax in the United States. Each of the 45 taxing states sets its own rates, taxable product categories, filing schedules, and enforcement priorities. However, several core rules apply across most jurisdictions.

When Does Use Tax Apply to Your Business?

Use tax applies to your business whenever you purchase taxable goods or services and the seller does not charge sales tax. The most common triggers include:

Purchases from out-of-state vendors without nexus in your state — for example, buying equipment from a vendor in another state that ships to you without charging tax

Online purchases from foreign vendors

or overseas suppliers where no US sales tax is collected Items removed from resale inventory for internal business use — for example, a cannabis dispensary using products from its own inventory for staff events

Goods brought into your state from another state — such as purchasing a vehicle or machinery in a no-sales-tax state like Oregon and bringing it into California

Software or digital subscriptions purchased

from vendors not registered in your state

Office furniture, equipment, or supplies purchased at out-of-state trade shows or conferences

For US taxpayers operating ecommerce businesses, the most common use tax trigger is purchasing inventory, packaging materials, or business equipment from out-of-state suppliers who do not charge your state’s sales tax. Many business owners assume this means the purchase is tax-free. It is not — it simply shifts the payment obligation to you.

How Is Use Tax Reported and Paid?

Most states require businesses to self-report use tax on their regular sales tax return. If you file sales tax returns in California, for example, there is a dedicated line for use tax on purchases made without sales tax. Some states issue a separate use tax return for businesses that have no sales tax filing obligation but still owe use tax on purchases.

Individuals in most states technically owe use tax

on personal online purchases as well, reported annually on their state income tax return. However, business use tax enforcement is far more rigorous than individual enforcement — state auditors routinely cross-reference business purchase records against reported use tax payments.

The IRS provides guidance on state tax obligations

through its State and Local Tax resources (IRS.gov/businesses/small-businesses-self-employed/state-and-local-governments), and each state’s department of revenue publishes specific use tax guidance for businesses. However, each state administers its use tax independently, so the rules genuinely differ.

Which States Are Most Aggressive About Use Tax Enforcement?

California, New York, Texas, and Illinois are widely regarded as the most aggressive use tax enforcement states for businesses. California’s CDTFA (California Department of Tax and Fee Administration) conducts regular desk audits of business purchase records to identify unreported use tax. Texas’s Comptroller of Public Accounts cross-references vendor sales data against business returns. A use tax audit in California can look back three to four years, generating assessments that include 10% penalty plus compounding monthly interest.

Use Tax vs Sales Tax Difference: Expert Tips for Staying Compliant in 2026

Tax enforcement is intensifying in 2026. State revenue departments are investing in data analytics, cross-referencing vendor sales data against business returns, and issuing targeted nexus questionnaires to businesses that appear to have purchasing patterns inconsistent with their reported use tax. Here are the most important strategies to stay ahead.

Request a taxability opinion letter from your state revenue

department for ambiguous product categories. Most states will provide a written ruling on whether a specific product or service is taxable — and that ruling protects you from penalties if their interpretation later changes.

Automate use tax tracking within your accounting software.

Both QuickBooks and Xero allow you to create a dedicated use tax expense category and liability account. When you enter a vendor bill with no sales tax charged, coding it to this category automatically builds your use tax return data without additional manual work.

Train your accounts payable team on use tax triggers.

The person entering vendor invoices is your first line of defense against unreported use tax. A brief internal training session — covering the five most common use tax triggers for your industry — dramatically reduces compliance gaps.

Watch for use tax rule changes in states

where you have significant purchasing activity. Several states updated their digital services use tax rules in 2024 and 2025, and more changes are expected in 2026 as states expand their tax bases to cover cloud software and SaaS tools more broadly.

Consider an annual self-audit of use tax compliance.

Each year, before filing your state tax return, run a complete review of your purchase records against your use tax log. Self-identifying and correcting any gaps before filing protects you against both penalties and the increased scrutiny that comes with audit selection.

Most importantly, remember that both sales tax and use tax

compliance ultimately rest on accurate, well-organized records. Businesses that maintain clean purchase logs and file consistently — even when the amounts are small — face dramatically lower audit risk than those that treat use tax as an afterthought.

Conclusion: Stop Ignoring Use Tax — Your Business Depends on It

The three most important takeaways from this guide are: first, sales tax and use tax are two sides of the same obligation — if sales tax was not collected at purchase, use tax is almost certainly owed; second, use tax applies to every US state where you store, use, or consume taxable goods, regardless of where you bought them; and third, voluntary disclosure is always better than waiting for an audit to force compliance.

Whether you run an e-commerce store,

a cannabis dispensary, a digital content business, or a traditional brick-and-mortar company with out-of-state suppliers, use tax is a real and enforceable obligation in every US state that imposes sales tax. Ignoring it does not make it go away — it only makes the eventual reckoning more expensive.

Ready to get expert help? Email us at hello@tranzesta.com or visit Tranzesta.com to schedule your free tax strategy session today.

FAQs

The main difference between sales tax and use tax is who pays the tax and when. Sales tax is collected by the seller at the point of sale and remitted to the state on the buyer’s behalf. Use tax is self-assessed and paid directly by the buyer when they purchase taxable goods or services without paying sales tax — typically from an out-of-state or foreign vendor. Both taxes apply to the same types of goods and at the same rate; the key difference is the payment responsibility and mechanism.

Yes, you may owe use tax on online purchases when the seller does not collect your state’s sales tax. Before the 2018 South Dakota v. Wayfair ruling, many online retailers with no physical presence in your state did not charge sales tax, creating widespread use tax obligations. Today, most major online retailers collect sales tax in all states where they have nexus. However, purchases from smaller vendors, foreign sellers, or platforms without nexus in your state may still arrive without sales tax — triggering your use tax obligation for those transactions.

If you have never reported use tax, you have several options. Most states allow you to report use tax on your regular sales tax return going forward — simply complete the use tax line on your next filing. For prior years of unreported use tax, a Voluntary Disclosure Agreement (VDA) with your state revenue department is typically the best approach. A VDA caps the lookback period — usually two to three years — and waives penalties in most states. A tax professional like Tranzesta can negotiate a VDA on your behalf and calculate the amounts owed.

For example, if California’s combined sales tax rate for your location is 9.5%, your California use tax on taxable purchases without sales tax is also 9.5%. Local county and city rates that apply to sales tax also apply to use tax in most jurisdictions.

State auditors routinely request three to four years of purchase records during a sales tax audit and then cross-reference them against reported use tax to identify gaps. A use tax audit can result in assessments covering all unpaid tax, penalties of up to 25% of the unpaid amount, and compounding monthly interest from the original due dates. Proactive compliance and clean purchase records are the best defenses.

5

Talk to a real, signing professional

AI precision, human accountability — across the US, UK & UAE.

Book a free consultation